Decentralized identity (DID) is transforming finance by addressing costly inefficiencies, security risks, and compliance challenges in identity management. Unlike traditional systems that store sensitive data in centralized databases, DID lets individuals control their credentials through digital wallets. This reduces data breaches, accelerates KYC/AML processes, and lowers compliance costs.

Key takeaways:

- KYC/AML Costs: DID reduces verification costs by 70–80%, cutting onboarding times from days to under a minute.

- Data Security: Eliminates single points of failure by distributing data control to users.

- Compliance: Automates AML checks with cryptographic proofs and smart contracts, reducing audit costs by over 90%.

- Cross-Border Payments: Enables seamless credential validation across jurisdictions.

- DeFi Integration: Links compliance credentials to wallets, ensuring secure participation in decentralized finance.

With regulations like eIDAS 2.0 mandating digital identity solutions in Europe by 2026, financial institutions are piloting these systems to improve efficiency and privacy while meeting legal requirements. DID is poised to reshape how banks handle identity verification and regulatory compliance.

Decentralized Identity Benefits in Finance: Cost Savings and Efficiency Gains

How Decentralized Identity Could Revolutionize KYC & Finance

sbb-itb-c5fef17

Problems with Centralized Identity Systems in Finance

Centralized identity systems, originally designed for a paper-based world, are now riddled with inefficiencies, security risks, and regulatory hurdles. As Stablewatch Research aptly notes:

The industry is attempting to build a 21st-century financial system on the back of a 20th-century compliance architecture [6].

KYC/AML Process Inefficiencies

Opening a new bank account or signing up for financial services often means going through the same tedious verification process repeatedly. On average, mobile onboarding in fintech involves 14 screens, 29 clicks, and 16 fields to complete [6]. This inefficiency is driving customers away – by 2025, 70% of financial institutions globally reported losing clients due to slow onboarding processes, up from 48% in 2023 [6].

Despite spending over $25 billion annually on financial crime risk management [5], most of the effort – around 80% – is spent on collecting and processing client information, leaving only 20% for actual risk analysis [5]. These bottlenecks delay transactions by 30–50 days and consume 10–20% of payroll budgets on compliance tasks [5][6]. For stablecoin-native firms, compliance costs can eat up between 5% and 20% of their yearly operational budget [6]. What’s worse, even customers who’ve already been verified are forced to repeat the process [4]. As Javed Khattak, Founder of cheqd, explains:

While current KYC is ‘single-use,’ SSI makes KYC ‘reusable’ [4].

These inefficiencies are just the tip of the iceberg, as centralized systems also face significant challenges with data security and storage.

Data Silos and Security Vulnerabilities

Centralized databases are prime targets for hackers, acting as single points of failure. When breached, they can expose sensitive information for millions. For instance, the Monzo data breach impacted nearly 500,000 customers, highlighting that even digital-first institutions are vulnerable [4]. In 2023 alone, hackers stole $1.1 billion from DeFi protocols [7]. Traditional verification methods, like selfies, are also becoming less reliable due to the rise of AI-powered deepfakes [4][8].

Financial institutions now manage tens of thousands of APIs and federated connections, each a potential entry point for adversarial AI attacks [9]. Centralized systems often create outdated copies of user data, which remain exposed across multiple platforms long after interactions end [9]. It’s no surprise that 100% of surveyed firms in the stablecoin sector listed avoiding data breaches as their top priority [6]. Decentralized identity systems offer a way out, distributing control to users and eliminating centralized data storage.

These vulnerabilities not only threaten privacy but also make regulatory compliance increasingly difficult.

Compliance and Regulatory Difficulties

As regulations grow stricter, centralized systems are struggling to adapt. Over the past decade, financial institutions in major economies have paid a staggering $26 billion in fines for failing to comply with KYC and AML requirements [5]. By 2025, the global cost of financial crime compliance is expected to hit $280 billion annually [6].

Laws like GDPR and CCPA add another layer of risk for centralized databases [1]. Meanwhile, modern financial systems rely on automated tools like smart contracts that demand instant, machine-readable compliance answers. As Stablewatch Research puts it:

A smart contract cannot make a phone call to a compliance officer; it requires a machine-readable yes/no answer to a compliance query [6].

Legacy systems, reliant on manual processes, impose an "Identity Tax" that drives up operational costs [6]. Security experts are raising red flags. Adam Preis, Director of Product & Solution Marketing at Ping Identity, warns:

Security leaders at the largest banks are now sounding the alarm that business-as-usual in these cloud and centralized models cannot be sustained anymore safely and securely [9].

The clash between global digital assets and fragmented identity systems is creating compliance challenges that traditional models simply can’t handle. These issues highlight the growing need for decentralized identity systems that can ensure both security and regulatory compliance.

How Institutions Use Decentralized Identity in Finance

Decentralized identity systems are stepping up to tackle major challenges in the financial sector. By integrating these systems, institutions are cutting costs, speeding up processes, and meeting regulatory requirements – all while safeguarding security and privacy.

Faster KYC and Customer Onboarding

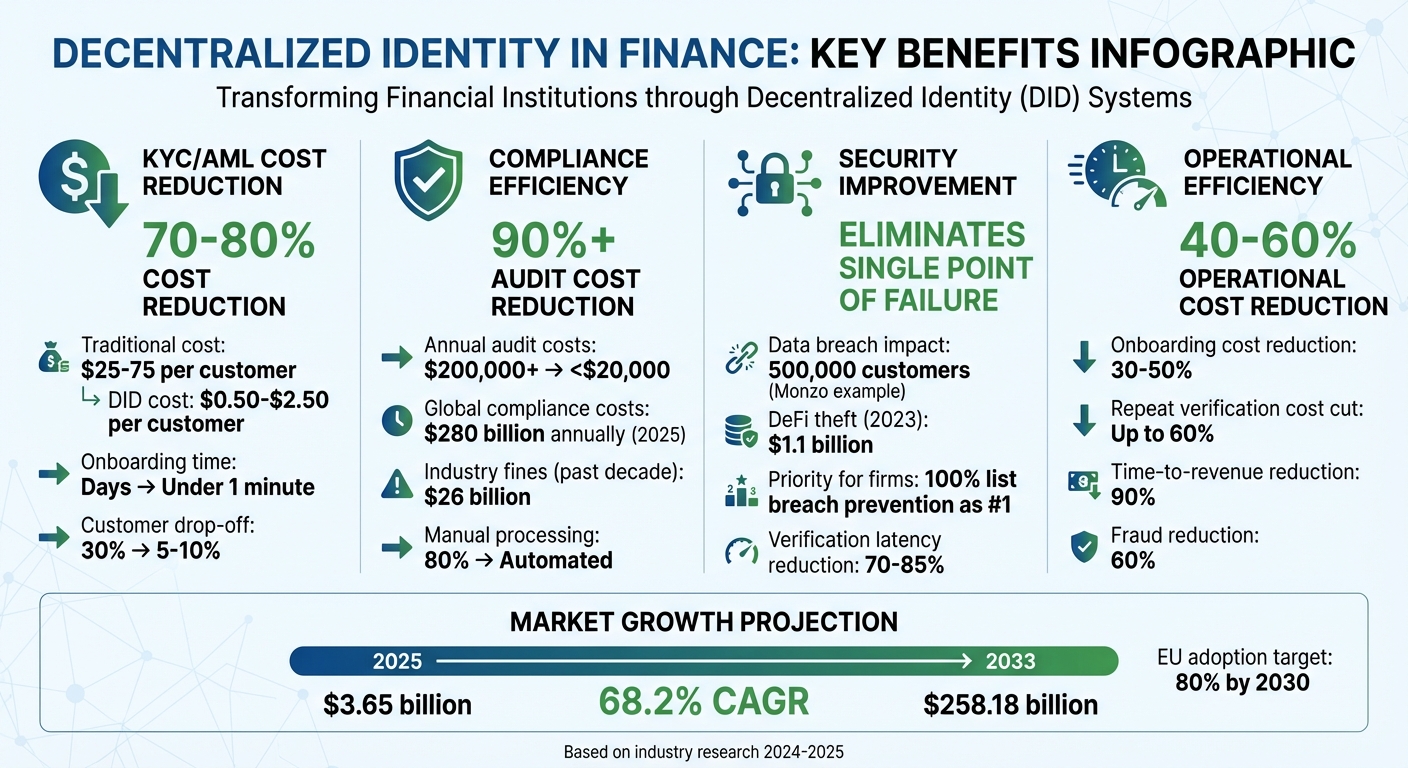

The traditional Know Your Customer (KYC) process is expensive and time-consuming, costing between $25 and $75 per customer and taking around 3–5 days. This lengthy process often leads to frustration, with about 30% of customers abandoning their applications midway[10].

Decentralized identity changes the game. Once a trusted issuer verifies a user’s information, they receive a cryptographically signed credential stored in their digital wallet. This credential can be reused across institutions, eliminating the need for repeated document submissions.

With decentralized identity networks, verification costs drop significantly to just $0.50–$2.50 per customer – a savings of 70% to 80%. Onboarding times shrink from days to under a minute, and customer drop-off rates fall to just 5–10%[10]. Zero-knowledge proofs further enhance privacy by verifying attributes like age or residency without revealing unnecessary personal details, reducing the risks of centralized data storage.

Some financial institutions now act as trusted issuers themselves, charging small fees when other entities verify their customers’ credentials. This not only creates a new revenue stream but also supports automated Anti-Money Laundering (AML) compliance measures[10].

Automated AML Compliance with Smart Contracts

The financial sector spends over $50 billion annually on KYC and AML processes, much of which goes toward outdated, manual systems that are slow and prone to errors[10].

Decentralized identity introduces real-time monitoring through permissioned blockchains, which create immutable audit trails. Smart contracts enforce compliance rules automatically, flagging or blocking transactions involving sanctioned entities. With a shared permissioned ledger, departments or partner institutions can access a customer’s verified AML status – with their consent – ensuring consistency across the board.

Zero-knowledge proofs also play a crucial role here, verifying whether a user appears on sanctions lists without revealing raw personal data. The TRUST (Travel Rule Universal Solution Technology) framework in the crypto space is a great example, allowing secure sharing of sender and receiver data without relying on a central database[10].

These advancements slash annual compliance audit costs from over $200,000 to less than $20,000. Blockchain-based systems also provide tamper-proof logs, simplifying evidence collection for regulators and potentially lowering penalties during audits. This automation naturally strengthens security for cross-border transactions as well.

Cross-Border Payments and Fraud Prevention

Decentralized identity systems are making cross-border payments more efficient. Credentials issued in one country can be programmatically validated against the regulatory requirements of another, reducing the legal complexities for multinational corporations[10].

For example, when a trusted entity in one jurisdiction issues a credential, institutions in other countries can instantly verify it against their local rules. This eliminates redundant paperwork and separate verification steps. By logging every verification event on a permissioned blockchain, institutions create a tamper-proof audit trail, making it harder for fraudsters to exploit stolen or fake credentials.

Institutional DeFi and Asset Tokenization

Decentralized finance (DeFi) has long struggled with compliance due to its reliance on anonymous wallet addresses. Decentralized identity bridges this gap by linking verifiable attributes – such as compliance credentials or membership status – to digital wallets, all while keeping personal identities private.

With verifiable credentials, institutions can create "gated" access to DeFi platforms. Only verified users can participate in governance voting, token sales, or other decentralized applications. Zero-knowledge proofs ensure that participants meet eligibility requirements – like being an accredited investor – without exposing unnecessary personal information.

This approach enables institutions to engage in DeFi while staying compliant with regulations. Asset tokenization platforms also benefit, as they can ensure that all participants are verified and meet compliance standards. This adds a much-needed layer of trust and accountability that traditional DeFi systems often lack.

Technical Framework for Decentralized Identity in Finance

Creating a decentralized identity system for financial institutions requires several interconnected elements. At its core are Decentralized Identifiers (DIDs) – user-controlled, unique identifiers that eliminate reliance on a central authority. These work hand-in-hand with Verifiable Credentials (VCs), which are digitally signed documents that contain claims (like KYC status or licenses) and can be verified cryptographically without needing to contact the original issuer.

This system operates on a "triangle of trust" model, involving three key participants: Issuers, Holders, and Verifiers. Issuers (such as banks or KYC providers) create and sign credentials. Holders store these credentials in secure digital wallets, sharing them when required. Verifiers (like onboarding systems or DeFi platforms) request and validate these proofs during specific user actions. Supporting this ecosystem are registries, which manage DID resolution, public key discovery, and revocation references. These registries can function either on-chain or off-chain, depending on institutional requirements.

In July 2022, the W3C introduced standards for DIDs, emphasizing four key features: decentralized, persistent/portable, verifiable, and resolvable/interoperable [11]. Below, we’ll explore the essential components that form the backbone of decentralized identity in finance.

Core Components of DID Infrastructure

Each element of a decentralized identity system plays a vital role in ensuring secure and streamlined operations. Here’s a closer look at the core components and their roles in financial infrastructure:

| Component | Role in Financial Infrastructure | Key Technical Requirement |

|---|---|---|

| Issuer | Regulated entity (e.g., bank, KYC provider) | VC Schema (e.g., KYC/KYB status, sanctions check) |

| Wallet | User interface for storing and sharing credentials | Secure key management, QR/deep link support |

| Verifier | Validates credentials during onboarding or high-risk actions | Integration with revocation registries |

| Registry | Manages DID resolution and key discovery | Alignment with W3C standards |

Modern systems often integrate Identity and Access Management (IAM) platforms to connect digital wallets with backend systems. This ensures trusted data exchange and keeps credentials up to date. Additionally, standards like SIOPv2 enable legacy applications and Single Sign-On systems to interact with digital wallets without requiring extensive code changes.

Zero-Knowledge Proofs and Privacy Protection

Zero-knowledge proofs (ZKPs) take privacy and efficiency to the next level in verification processes. With ZKPs, financial institutions can verify user information without collecting or storing sensitive data. For example, users can prove they meet specific requirements – like being over 18 or residing in an approved country – without revealing personal details. Institutions receive only a simple yes/no validation, reducing the risk of data breaches and liability.

"Instead of handing over your entire life history, you can prove you meet a bank’s requirements, such as age, country, or verification status, without revealing anything else. No documents are exchanged. No sensitive data sits on a server." – Khaleel Pasha, Engineering Lead [14]

ZKPs also improve efficiency, cutting verification latency by 70–85%, making them ideal for real-time systems like trading engines [12][13]. Different types of ZKPs offer distinct advantages:

- ZK-SNARKs: Compact and efficient but require a trusted setup.

- ZK-STARKs: Quantum-resistant and eliminate the need for a trusted setup, though they generate larger proofs.

- Recursive Proofs: Enable scalability by verifying other proofs, especially in high-frequency environments.

For financial institutions, optimizing latency through techniques like batching and recursion is critical. The overall efficiency of these systems depends heavily on circuit optimization.

Credential Lifecycle and Revocation Management

Managing the lifecycle of verifiable credentials is crucial to maintaining the integrity of a decentralized identity system. Once credentials are issued by regulated entities, holders store them in secure wallets. These credentials are used to generate cryptographic proofs during onboarding or high-risk transactions. Verifiers can then validate these proofs without needing direct communication with the issuer.

Revocation management is another key aspect. Issuers maintain revocation registries or status lists, allowing verifiers to check if a credential has been invalidated. For high-risk credentials like KYC or sanctions checks, expiration dates are often implemented to ensure data stays current and compliant, prompting periodic re-verification.

The decentralized identity market is expected to grow at an annual rate of over 70% between 2024 and 2032 [9]. By 2030, projections suggest that 80% of the EU population will have access to a European Digital Identity (EUDI) Wallet [9]. Financial institutions should begin piloting digital wallet onboarding now to prepare for regulatory requirements like eIDAS 2.0. Employing selective disclosure or ZKPs to verify attributes – such as age or KYC status – without exposing sensitive data can further reduce risks and enhance privacy.

Benefits and Adoption Trends for Institutions

Key Benefits for Financial Institutions

Decentralized identity offers a game-changing way for financial institutions to streamline processes and cut costs. For instance, reusable credentials enable one-time verification that can be used repeatedly, slashing onboarding times from days to mere minutes [9]. This efficiency helps tackle the staggering $275.13 billion annual cost of financial crime compliance and addresses the $47 billion Americans are projected to lose to identity fraud and scams in 2024 [17][15].

By incorporating cryptographic proofs and selective disclosure, these systems significantly reduce the need to store large amounts of Personally Identifiable Information (PII). This not only minimizes identity fraud risks but also lowers regulatory liabilities. On average, organizations face $7 million annually in identity fraud costs, with larger enterprises (those with over 5,000 employees) seeing costs around $13 million [15]. Decentralized systems eliminate the need for centralized databases, which are often targeted by hackers, instead relying on Zero-Knowledge Proofs to confirm details like age or sanctions status without storing raw data [15][3].

| Benefit Category | Institutional Advantage | Impact Metric |

|---|---|---|

| Onboarding | Instant verification via reusable credentials | Reduction from days to minutes [9] |

| Fraud | Cryptographic proof and out-of-band verification | Significant drop in fraud risks [9] |

| Compliance | Automated compliance with smart contracts | Reduced need for manual audits and oversight [15] |

| Data Privacy | Selective disclosure (Zero-Knowledge Proofs) | Lowered PII storage and compliance risks [15][1] |

| Cross-Border | Recognition of digital credentials across borders | Easier expansion into regulated markets [9] |

This shift in digital identity management addresses long-standing challenges for financial institutions. Smart contracts, for example, embed regulatory requirements directly into the system, ensuring compliance without the need for constant manual checks [15]. This approach aligns with regulations like GDPR and CCPA by giving users more control over their data while reducing the compliance burden for institutions [16][17]. These advantages are paving the way for broader industry adoption.

Current Adoption Patterns in Finance

The financial sector is rapidly embracing decentralized identity due to its operational and security benefits. In 2025, the Banking, Financial Services, and Insurance (BFSI) sector made up 19.3% of the decentralized identity market, with the global market valued at $3.65 billion. This market is expected to skyrocket to $258.18 billion by 2033, growing at an annual rate of 68.2% [16][17]. North America currently leads the way, accounting for 32.8% of market revenue, as institutions transition from pilot programs to fully operational systems [16].

Real-world examples highlight this momentum. In January 2025, Identity.com launched a mobile app for decentralized identity management, available on both the Apple App Store and Google Play Store. This app allows users to store verifiable credentials for tasks like age verification and KYC (Know Your Customer) processes, all while maintaining control over their personal data [16][17]. Similarly, Ripple introduced its "Credentials" and "Deep Freeze" features on the XRP Ledger in September 2025. These tools enable institutions to verify KYC status and even freeze accounts to comply with sanctions, effectively turning the ledger into a regulated settlement layer for stablecoin transactions exceeding $1 billion per month [18].

Regulatory developments are also driving adoption. The eIDAS 2.0 regulation, effective May 2024, requires very large online platforms (VLOPs), including financial institutions, to accept the European Digital Identity (EUDI) wallet for customer authentication by mid-2026 [9]. Technical standards for this initiative are set to be finalized by mid-2025, with predictions that 80% of EU citizens will use digital IDs by 2030 [17]. Financial institutions should start integrating their onboarding processes with the EUDI Wallet ecosystem and stay updated on national legislation timelines [2][9].

"By 2026, very large online platforms (VLOPs), including financial institutions offering high-value or regulated services, will be required to accept the EUDI wallet for customer authentication." – Ping Identity [9]

Privacy-preserving technologies are becoming a cornerstone of identity management. By the end of 2025, over 60% of large businesses are expected to adopt at least one Privacy-Enhancing Technology (PET) solution, with Zero-Knowledge Proofs leading the charge for verifying eligibility without exposing sensitive data [17]. Additionally, biometric identity verification accounted for 66.0% of the market share in 2025, showcasing the growing use of AI-driven biometric tools to detect deepfakes and establish "proof of humanity" in digital transactions [16][15][9].

Decentralized Identity in Finance: 2026 Outlook

The Future of Reusable Credentials

The financial services sector is experiencing a major transformation as wallet-based interfaces take over traditional browser sign-ups. By 2026, users will "connect" to financial services instead of creating separate accounts, storing key documents like government IDs, educational records, and credit scores directly in their digital wallets [19]. This shift isn’t just convenient – it’s cost-effective. Organizations leveraging reusable credentials are slashing onboarding expenses by 30–50% and cutting repeat verification costs by up to 60% [20].

The market for decentralized identity is expected to hit $7.4 billion in 2026, a sharp rise from $2.56–$4.89 billion in 2025 [20]. Financial institutions are moving toward a "KYC Verified" credential model. This means verification completed by one bank can be reused seamlessly for onboarding at another financial service, like a DeFi protocol or exchange, in mere seconds [19][20]. Zero-Knowledge Proofs are at the heart of this system, enabling users to confirm criteria – such as "income > $50,000" or "age > 18" – without revealing sensitive personal data [20][21].

Another intriguing development for 2026 centers on AI agent identity. New regulations require autonomous AI agents to have unique Decentralized Identifiers (DIDs) linked to human or corporate supervisors to curb fraud [19][20]. Additionally, modern wallets now generate unique DIDs for each website a user visits through "pairwise IDs", ensuring institutions can’t track user behavior across platforms [19].

These advancements are paving the way for regulatory updates and enterprise integration.

Regulatory Changes and Integration

Regulatory mandates are now reshaping how financial services operate. Under eIDAS 2.0, all EU member states must provide at least one European Digital Identity (EUDI) Wallet by the end of 2026, with mandatory acceptance starting in 2027 [20][23]. The upcoming Anti-Money Laundering Regulation (AMLR), effective July 2027, will harmonize KYC practices across the EU. It will only permit eIDAS-notified digital IDs, the EUDI Wallet, and qualified trust services for identity verification [23].

For financial institutions, the clock is ticking. With technical integration taking 12–18 months, organizations need to act quickly [20]. They must register as relying parties with national authorities to legally accept EUDI Wallet credentials and ensure their Identity and Access Management (IAM) systems comply with ISO/IEC 18013-5 and W3C Verifiable Credentials standards before the 2027 deadline [23]. The European Commission aims for 80% wallet adoption among EU citizens by 2030 [22][9], with decentralized KYC mechanisms projected to cut operational costs by 40–60% [22].

"The EUDI Wallet is the EU encoding privacy-by-design into law: minimum data, held by users, reused without re-collection, and distributed without central repositories." – Edoardo Mustarelli, Fintech/Web3 Strategist, Zyphe [23]

The regulatory framework is aligning with global standards like W3C Verifiable Credentials, Decentralized Identifiers (DIDs), and OpenID for Verifiable Credentials (OpenID4VC) [20][9]. Additionally, the Anti-Money Laundering Authority (AMLA) in Frankfurt is tasked with issuing Regulatory Technical Standards (RTS) throughout 2026–2027, with a key deadline of July 10, 2026, for publishing KYC/AML standards [23].

Enterprise Pilots and Emerging Use Cases

Real-world applications of decentralized identity are picking up pace across Europe. In March 2026, EU member states and wallet providers successfully tested cross-border credential exchange during a live event in Romania, proving the EUDI Wallet’s readiness for international financial use cases [23]. A leading North European bank is actively incorporating decentralized identity into its onboarding and authentication processes. Meanwhile, a major German bank and a London-based multinational are piloting EUDI Wallet integration into their workflows [9].

Beyond KYC, financial institutions are exploring cutting-edge applications. For example, out-of-band verification is being used to combat AI-generated deepfakes and synthetic identities. Banks are rerouting transaction verifications through decentralized wallet channels, requiring local device access and cryptographic proof to ensure security [9]. Some pilots are even embedding payment capabilities directly into digital wallets, enabling secure transactions without needing to manually input card details – drastically reducing merchant fraud [9].

The Zero-Knowledge Proof sector alone reached $28 billion in total value locked in 2025 [20]. By 2026, 80% of Fortune 500 companies are expected to use Microsoft Entra Verified ID for employee credentials [19], signaling a shift from pilot programs to full-scale adoption. Additionally, organizations are testing AI compliance agents paired with decentralized identity, which could reduce manual review costs by up to 85% [23].

These pilot projects highlight a clear trend: the financial sector is moving toward secure, efficient, and regulation-compliant decentralized identity systems.

Conclusion

Decentralized identity marks one of the biggest shifts in banking infrastructure since the adoption of cloud computing [24]. By 2026, it has transitioned from a theoretical idea to a practical system, transforming how banks handle verification, compliance, and customer interactions.

The benefits are hard to ignore. Banks leveraging decentralized identity report major efficiency improvements: onboarding costs drop by up to 40%, verification times are reduced by 70%, fraud decreases by 60%, and time-to-revenue is slashed by 90% [24].

The way data is managed is undergoing a fundamental change. Instead of acting as centralized data holders vulnerable to breaches, banks are becoming trusted issuers of verifiable credentials, which customers control. This evolution – from "owning" data to "verifying" claims – removes the need for repetitive KYC processes, reduces liability, and introduces a privacy-first compliance model using Zero-Knowledge Proofs. This approach not only modernizes data management but also connects traditional banking to the growing world of decentralized finance. As Elena Rodriguez, Chief Innovation Officer at Global Bank Alliance, puts it:

"Decentralized identity is no longer a theoretical concept; it is the foundational infrastructure that allows institutional finance to scale securely in a digital-first economy" [24].

With proven cost savings and stronger compliance frameworks, the focus now shifts to strategic implementation. Regulatory mandates like eIDAS 2.0 are driving adoption, and 85% of Tier-1 banks are already running decentralized identity pilots [24]. The question is no longer if this technology will be adopted but how quickly it can be fully integrated. Decentralized identity serves as a critical trust layer, connecting traditional finance with decentralized finance, enabling regulated capital to move on-chain while maintaining compliance.

Banks that embrace W3C-compliant standards, prioritize privacy through Zero-Knowledge Proofs, and deliver user-friendly experiences are poised to lead the next chapter of institutional finance.

FAQs

What changes in a bank’s risk and liability model when customers hold the identity data?

When banks allow customers to manage their identity data through decentralized systems, they significantly lower their exposure to risks like data breaches and fraud. Since sensitive personal information is no longer stored directly by the bank, verification processes rely on cryptographically secured credentials instead. This approach not only reduces liability but also aligns more effectively with data privacy regulations. Additionally, reusable and verifiable credentials enhance the customer experience while contributing to a stronger and more compliant risk management framework.

How can institutions revoke or update KYC/AML credentials without tracking users across services?

Decentralized identity systems, such as Decentralized Identifiers (DIDs) and verifiable credentials, offer institutions a way to manage KYC/AML credentials more efficiently. These systems empower users to securely control their credentials while sharing only the information that’s absolutely necessary.

When credentials need to be revoked or updated, the process is handled through a decentralized ledger or a revocation registry. User wallets can check these registries in real-time, ensuring that any updates or revocations are immediately recognized. This approach not only maintains user privacy and ensures compliance but also eliminates the need to track individuals across multiple services.

What do U.S. financial institutions need to integrate DIDs and verifiable credentials into existing IAM and compliance systems?

To bring Decentralized Identifiers (DIDs) and verifiable credentials into their operations, U.S. financial institutions need to take a few key steps. First, they should implement digital identity wallets to securely manage credentials and use cryptographic proofs to verify identity claims without revealing sensitive information. Next, their compliance systems must support interoperability standards to enable smooth data exchange across platforms while adhering to regulations like AML/CFT (Anti-Money Laundering and Counter-Terrorism Financing) frameworks. These measures help ensure the integration of decentralized identity solutions is both secure and privacy-conscious.