Token Purchase Agreements (TPAs) are legal documents used in Web3 projects to sell tokens to investors. Unlike SAFTs, which apply before tokens are created, TPAs are used after tokens are minted or ready for launch. Properly structuring a TPA ensures regulatory compliance, protects both parties from risks, and establishes clear terms for token allocation, vesting, and transfer. Key elements include:

- Defining parties and token details: Specify the buyer, seller, token purpose, and allocation.

- Vesting and lock-up schedules: Prevent price crashes and align distribution with long-term goals.

- Regulatory compliance: Use frameworks like Regulation D or Regulation S to avoid legal issues.

- Transfer restrictions: Include anti-dilution clauses, lock-ups, and KYC/AML measures.

- Dispute resolution: Detail arbitration processes and enforce agreements via smart contracts.

A well-drafted TPA balances investor protections with project flexibility, ensuring smooth token sales and long-term stability.

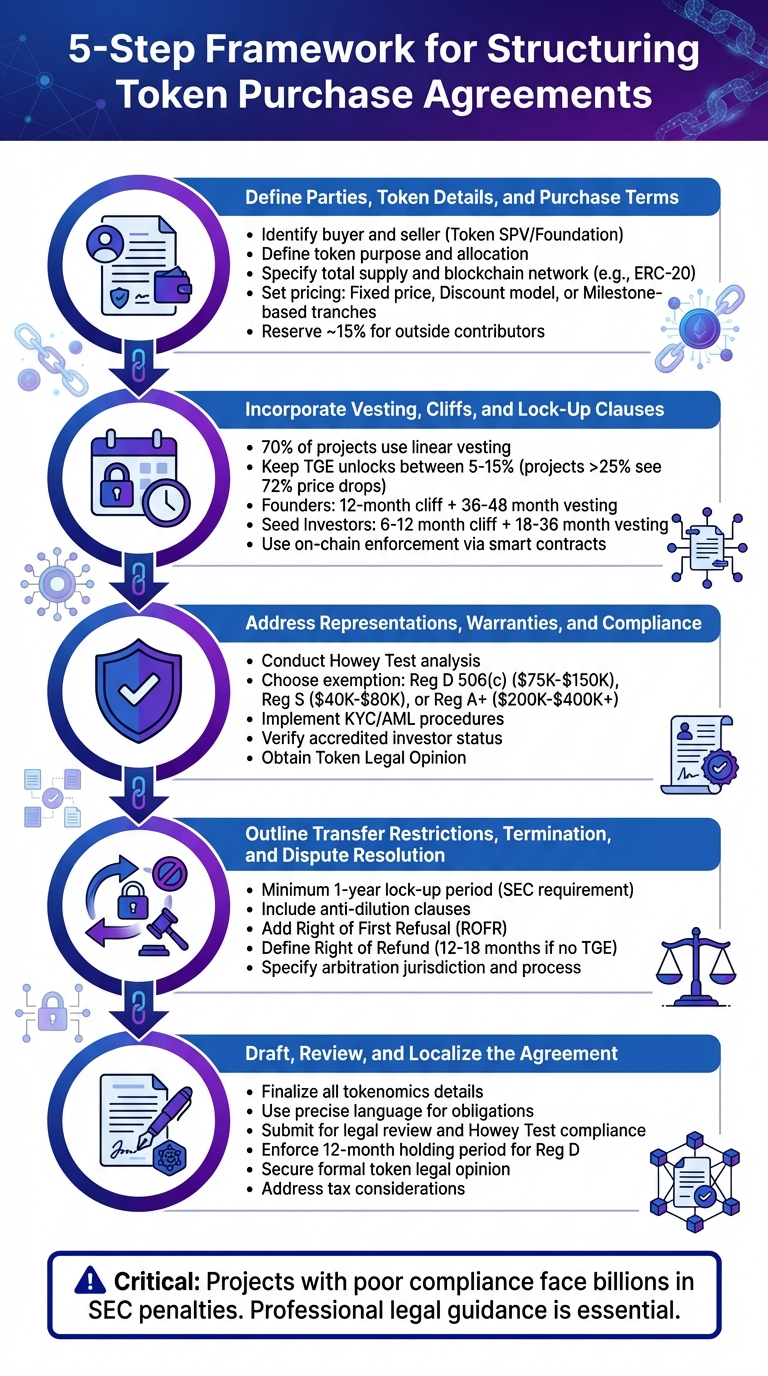

5-Step Framework for Structuring Token Purchase Agreements in Web3

Step 1: Define Parties, Token Details, and Purchase Terms

Identifying the Parties Involved

Start by identifying the buyer and seller in the agreement. Web3 transactions often involve multiple specialized entities, making this step crucial.

The seller is typically a Token SPV (Special Purpose Vehicle) or a Token Foundation – a separate entity set up specifically to issue tokens. This structure helps shield the core development team from regulatory risks. As Pavel Batishchev, Managing Partner at Aurum Law, explains:

"A Web3 project legal structuring begins with forming a legal entity. Without one, the core team may be deemed to operate as a general partnership – exposing each member to unlimited, joint and several liability for all obligations of the project." [4]

The buyer might be an institutional investor (like a VC fund), an accredited individual investor, or a liquidity provider. The agreement should include the full legal name, jurisdiction (e.g., Cayman Islands, BVI, or Switzerland), and registration details for all parties. This level of detail ensures compliance with local VASP (Virtual Asset Service Provider) and tax laws.

Additionally, document any intermediaries involved in conducting KYC/KYB checks to avoid dealings with sanctioned or high-risk parties.

Once the parties are defined, the next step is to outline the token’s characteristics and allocation.

Token Characteristics and Allocation

Clearly define the token’s purpose – whether it’s a utility token, governance tool, or payment mechanism. This classification impacts regulatory treatment and shapes investor expectations.

Include details such as the total token supply and whether the project operates with a hard cap (a fixed fundraising limit) or no cap. Specify the exact number of tokens or percentage of the total supply allocated to the buyer. These allocations are often drawn from designated pools like the investor pool, founder pool, or community pool. For example, the Web3 project MovitOn structured its 2023 token launch with well-defined allocation pools, achieving a 97% KYC success rate while raising $506,000 [5]. Such transparency builds trust and sets clear expectations.

Also, identify the blockchain network and technical standard (e.g., ERC-20) for the tokens. If tokens haven’t been minted yet and you’re using a SAFT (Simple Agreement for Future Tokens), define the "Conversion Event" – the milestone (such as a Network Launch) that will trigger token issuance. Christian Sauer, Founder of soonami, suggests:

"We typically advise reserving around 15% of tokens for outside contributors, with the remainder staying with the core founding team." [7]

Purchase Amount and Pricing

Pricing depends on your project’s stage. If your tokenomics are finalized, detail a fixed purchase price, often referred to as a "pre-sale" price. If tokenomics are still under development, use a discount-based model where the investor gets a predetermined discount on the future token price.

Specify the purchase amount in USD or cryptocurrency, and include wallet addresses for token receipt and delivery to ensure proper auditing. Digital assets lawyer Oldrich Peslar advises:

"In case any third party would receive better terms, the Company shall immediately notify the Purchaser about such a fact, and the Purchaser shall receive such better terms upon a Purchaser’s consent." [3]

To balance risk, consider structuring payments in tranches tied to Key Performance Indicators (KPIs). For example, 50% of the payment could be delivered immediately, with the remaining 50% tied to milestones like a Token Generation Event (TGE) or mainnet launch. This approach protects both the investor and the project, ensuring alignment during development.

| Payment Structure | Conditions | Key Benefit |

|---|---|---|

| Fixed Price | Tokenomics finalized | Clear valuation and allocation |

| Discount Model | Tokenomics in development | Flexibility for early investors |

| Milestone-Based Tranches | Long development timeline | Risk mitigation for both parties |

With these foundational elements – parties, token details, and pricing – clearly defined, the next step focuses on vesting and lock-up clauses.

sbb-itb-c5fef17

Step 2: Incorporate Vesting, Cliffs, and Lock-Up Clauses

Designing Vesting Schedules

Once purchase terms are defined, vesting schedules help ensure token distribution aligns with long-term goals. These schedules determine when and how tokens are released to buyers and team members. Without vesting, early token sales can lead to price crashes and damage community confidence. Projects with poorly designed vesting structures see 40-60% greater price volatility in their first year [8].

The most popular method is linear vesting, where tokens unlock in equal increments over time. About 70% of projects use this approach because it’s straightforward and predictable [8]. For example, a 24-month linear vesting schedule splits token releases equally each month. Uniswap adopted a 4-year linear vesting plan for its team allocation to maintain long-term alignment [9].

Other vesting strategies, like back-weighted and S-curve vesting, can further reduce sell pressure. Back-weighted (exponential) vesting releases fewer tokens early on, with a faster pace toward the end. This structure works well for retaining founders during critical growth stages. Filecoin used a 6-year back-weighted schedule for its team and founders, signaling a strong commitment to its protocol’s development [9]. S-curve (sigmoid) vesting, on the other hand, starts slowly, accelerates in the middle, and tapers off at the end, making it ideal for keeping strategic partners engaged during growth phases [8].

In Web3 projects, around 70% of vesting schedules are now event-triggered rather than based strictly on time from the agreement date [12]. Often, vesting begins at a specific milestone, such as the Token Generation Event (TGE) or mainnet launch. It’s crucial to keep TGE unlocks low – ideally between 5-15% of the total allocation. Projects with TGE unlocks over 25% typically see median first-year price drops of 72%, compared to 38% for those with unlocks under 15% [8].

An emerging option is block-by-block vesting, using tools like Sablier or Superfluid. This method provides continuous, per-block token releases rather than larger, periodic unlocks (e.g., monthly or quarterly). It helps smooth out selling pressure and minimizes volatility tied to major unlock events [9][12][13].

To further secure token distribution, consider adding cliffs and lock-up periods.

Establishing Cliffs and Lock-Up Periods

Cliffs, paired with vesting schedules, delay token availability to strengthen commitment during early stages. A cliff is a waiting period where no tokens vest initially, acting as a "commitment gate" for participants. Industry norms vary by role: 85% of projects implement 12-month cliffs for founders and core team members, while investors typically have 6-12 month cliffs [8].

| Stakeholder Role | Typical Cliff Period | Typical Vesting Duration |

|---|---|---|

| Founders / Core Team | 12 months | 36-48 months |

| Seed Investors | 6-12 months | 18-36 months |

| Advisors | 6 months | 12-24 months |

| Strategic Partners | 6-12 months | 18-36 months |

A 12-month cliff also complies with U.S. Rule 144, which requires a one-year holding period for unregistered securities before resale [14]. This rule protects both the project and investors from potential regulatory issues.

To avoid large-scale sell-offs, stagger cliff dates across different groups. For instance, set the team cliff at 12 months post-TGE, seed investors at 6 months, and strategic partners at 9 months. Research on over 500 unlock events shows that large unlocks exceeding 5% of circulating supply often lead to 8-15% price declines in the 30 days surrounding the event [8].

Include "bad leaver" provisions to reclaim unvested tokens if a team member leaves prematurely or is terminated for misconduct, such as fraud [9][11]. For acquisitions, consider "double-trigger" acceleration, where tokens vest fully only if the company is acquired and the individual is terminated within a specific timeframe [11].

Lastly, enforce vesting schedules on-chain using audited smart contracts like OpenZeppelin‘s VestingWallet. This ensures the schedule is transparent and immutable, giving investors confidence while preventing unilateral changes by founders [8][10][13]. Use simulators to model monthly token unlocks over a 48-month period to confirm your distribution plan won’t create excessive sell pressure [9][13].

Step 3: Address Representations, Warranties, and Compliance Requirements

Representations and Warranties

Once vesting schedules are in place, it’s time to focus on legal guarantees from both sides. These representations and warranties are essential for creating accountability and protecting all parties involved.

For the issuer (your project), there are several critical confirmations to make. First, ensure your company is legally established and authorized to issue tokens. Verify token ownership and transfer rights. Any information shared with investors – whether about your technology, team, or roadmap – needs to be accurate. Additionally, confirm that your project is not facing bankruptcy or any legal issues that could impact the token sale[16][3].

On the purchaser’s side, requirements vary. For U.S.-based transactions under Regulation D, buyers must meet the accredited investor criteria outlined in Rule 501. This typically means having a net worth exceeding $1,000,000 (excluding their primary residence) or an annual income of over $200,000 (or $300,000 for joint income). Purchasers should also agree that they are buying tokens for their own use, not for immediate resale, and acknowledge that these tokens may be classified as securities with restrictions on transfers[16][18].

It’s also wise to include a risk acknowledgment clause. Buyers should confirm their technical and financial expertise to evaluate Web3 investments, which can protect your project against claims of insufficient disclosure later on[16].

Another important step is conducting "bad actor" disqualification checks. Regularly monitor your team and major token holders to ensure compliance with Regulation D exemptions. The SEC may disqualify an offering if key participants have prior securities violations[15].

With these legal assurances in place, the next focus is regulatory compliance.

Compliance with Regulatory Frameworks

Navigating U.S. securities laws is one of the toughest challenges for token sales. Since 2017, the SEC has penalized over 100 token projects for failing to comply with regulations[15]. The difference between a smooth launch and enforcement action often boils down to having a solid compliance plan from the start.

Start with a detailed Howey Test analysis. This test determines whether your token qualifies as an "investment contract" by examining four criteria: investment of money, common enterprise, expectation of profits, and profits reliant on the efforts of others. Many projects fail this test because their networks are not decentralized at the time of the token sale, leaving buyers dependent on the team for any value increase[15][18].

For most Web3 projects, full SEC registration isn’t practical. Instead, structure your token sale under specific exemptions:

- Regulation D (Rule 506(c)): Permits public marketing but restricts sales to verified accredited investors. Legal costs typically range from $75,000 to $150,000.

- Regulation S: Applies to offshore sales to non-U.S. persons and requires strict geofencing to prevent U.S. marketing. Legal costs are usually between $40,000 and $80,000.

- Regulation A+: Functions like a mini-IPO, allowing sales to the general public after SEC qualification. Costs can range from $200,000 to $400,000 or more[18].

| Exemption | Investor Type | Public Marketing | Holding Period | Legal Costs |

|---|---|---|---|---|

| Reg D 506(c) | Verified Accredited only | Yes | 12 months | $75,000–$150,000 |

| Reg S | Non-U.S. persons only | No (in U.S.) | 6–12 months | $40,000–$80,000 |

| Reg A+ Tier 2 | General Public | Yes | None | $200,000–$400,000+ |

Incorporate KYC/AML procedures into your onboarding process. Use trusted third-party services like Jumio or Onfido to screen against sanctions lists from OFAC, the EU, and the UN[15]. Purchasers must pass these checks before receiving tokens, and your agreements should block transfers to non-compliant addresses.

When marketing your tokens, avoid language like "ROI", "investment", or "profits", as these terms can trigger the Howey Test. Instead, emphasize the token’s "utility" and "functionality." For example, in April 2024, Terraform Labs and founder Do Kwon faced a $4.5 billion settlement with the SEC for fraud and unregistered crypto asset securities offerings. Their case underscores why careful phrasing and compliance are critical[18].

"The difference between a successful launch and an SEC enforcement action often comes down to one thing: having a comprehensive compliance strategy from day one." – Sergei, Attorney[15]

Enforce transfer restrictions directly in your token’s smart contract to comply with lock-up periods. For Regulation D offerings, this typically involves a 12-month holding period under Rule 144. By embedding these restrictions into your smart contract, you show regulators your commitment to compliance[18][19].

Finally, secure a formal token legal opinion from experienced counsel. This document confirms your token’s regulatory classification and reassures investors about future risks. In July 2019, Blockstack PBC became the first company to complete an SEC-qualified Regulation A+ token offering, raising $23 million from over 4,000 investors by following a strict compliance approach[18].

Step 4: Outline Transfer Restrictions, Termination, and Dispute Resolution

Transfer Restrictions

To maintain compliance and stability, it’s essential to clearly define how and when tokens can be transferred. Transfer restrictions are a safeguard against regulatory scrutiny and market disruptions.

One effective measure is a minimum one-year lock-up period. This can include a one-year cliff, followed by a gradual release over three years. The SEC has previously blocked token issuances that failed to include such restrictions[20]. As Miles Jennings, General Counsel at a16z crypto, emphasizes:

"Always make token lockups apply for at least one year from token launch." [20]

Another critical element is an anti-dilution clause. This ensures that if the total token supply increases during the lock-up period, investors automatically receive additional tokens to maintain their ownership percentage. Oldrich Peslar, Head of Legal at Rockaway Blockchain Fund, highlights the importance of this:

"There is nothing worse than angry investors who were unfairly diluted." [3]

Additionally, include a Right of First Refusal (ROFR) clause. This gives existing investors the opportunity to participate proportionately in future token sales or funding rounds, preserving their investment stakes. For projects that haven’t achieved sufficient decentralization, enforce geographic restrictions and implement KYC/AML checks for all token transfers to minimize regulatory risks[20][6].

By setting these transfer restrictions, you create a framework that not only protects investors but also ensures compliance with regulatory standards.

Termination Clauses

Termination clauses are essential for defining how agreements can end if circumstances change. These clauses protect both parties and establish clear financial consequences.

A Right of Refund provision is a key feature. This clause allows investors to recoup their funds if the Token Generation Event (TGE) doesn’t occur within a specified timeframe – usually 12 to 18 months from the agreement date[3]. This ensures investors aren’t left in limbo if the project faces delays.

Termination rights should also cover scenarios like failed KYC/AML checks, regulatory changes, or significant shifts in the project’s business strategy. For example, Kima Network’s terms explicitly address this:

"The Seller reserves the right to refuse or cancel any request(s) to purchase or purchases of $KIMA… in connection with an adverse change in the regulatory environment." [21]

When refunds are issued due to delays or cancellations, the agreement should allow for deductions to cover legitimate costs. These might include blockchain network fees, administrative expenses (commonly capped at 5%), and documented marketing costs[21]. However, avoid granting the project unlimited discretion to terminate agreements without cause. This ensures a balance between flexibility for regulatory risks and protection against arbitrary decisions[3].

Finally, include representations that the project is not insolvent or facing bankruptcy. Without this assurance, investors could end up with tokens that have no value[3].

By addressing termination conditions thoroughly, you create a safety net for both investors and the project.

Dispute Resolution Mechanisms

Dispute resolution provisions are essential for handling conflicts efficiently and avoiding costly legal battles.

Consider combining traditional legal systems with blockchain-based solutions. For example, escrow-based enforcement can freeze funds in a smart contract until disputes are resolved[23].

Choosing the right jurisdiction is another critical step. Jurisdictions like Switzerland, Liechtenstein, or the British Virgin Islands provide clearer legal frameworks for digital assets, making arbitration faster and more predictable[6]. Be sure to specify the jurisdiction and governing law in your agreement.

Arbitration is often preferred over litigation for Web3 agreements. It’s faster, more private, and allows the selection of arbitrators with expertise in crypto. Your agreement should detail the arbitration process, including the venue, the number of arbitrators (one or three is typical), and how costs will be shared. For smaller disputes – under $50,000, for instance – require mediation first to encourage negotiation before moving to formal arbitration.

Lastly, integrate dispute triggers directly into your smart contract. Use "if/when…then" logic to automate enforcement. For example:

“If milestone X is unmet by date Y, trigger automatic release of Z% of escrowed funds.”

This type of automation removes ambiguity and ensures that the agreed-upon outcomes are executed smoothly and without manual intervention[22].

Step 5: Draft, Review, and Localize the Agreement

Drafting the Agreement

This step brings together all the prior work into a clear, legally sound agreement that’s ready to be executed. It’s critical to seek professional legal advice to ensure every key term is included in a way that’s enforceable. Missteps here can be costly – just look at the billions in penalties the SEC has imposed on token projects that failed to meet regulatory standards [15].

Before drafting a SAFT or TSA, finalize all tokenomics details, such as the blockchain network, total token supply, and token price or discount [24]. This helps avoid expensive revisions later and ensures all parties know exactly what they’re agreeing to.

The agreement must use precise language to outline obligations. For example, specify the purchase amount in U.S. dollars (e.g., $500,000), the exact number of tokens (or a clear calculation method), and payment timing [16]. Clearly define trigger events like "Network Launch" using measurable benchmarks, such as the mainnet becoming operational, the protocol offering functional utility, and a minimum number of independent validators. Avoid vague terms like "when ready" or "upon completion", as they can lead to disputes or regulatory risks.

Include robust representations and warranties for both sides. Purchasers should confirm they are accredited investors (for U.S. transactions), intend to hold the tokens as an investment (not for immediate resale), and understand the risks involved [16]. On the company’s side, it must affirm its legal status, its authority to issue tokens, and its compliance with applicable laws [16].

Review and Amendments

Once the draft is ready, submit it for legal review to ensure compliance with the Howey Test and applicable registration exemptions. The agreement must clearly specify the exemption it relies on. For U.S. accredited investors, this often involves Regulation D (Rules 506(b) or 506(c)). For offshore transactions, Regulation S is typically used, while public offerings might require Regulation A+ [19]. Each exemption comes with different costs – Regulation D 506(c) filings, for example, range from $75,000 to $150,000, while Regulation A+ (Tier 2) filings can exceed $200,000 to $400,000 [18].

Be cautious with marketing language. It should not emphasize potential investment returns. As Chanté Eliaszadeh from Astraea Law points out:

"The label is irrelevant. Courts apply the Howey Test based on economic realities, not what you call the token." [18]

Ensure that transfer and resale restrictions are explicitly outlined. For tokens sold under Regulation D, a 12-month holding period is mandatory, along with resale limitations to avoid being classified as unregistered securities [15]. Verify that your KYC/AML protocols are still in place, including screening for OFAC sanctions. Additionally, make the agreement contingent on successful security audits of the smart contracts by at least two independent auditors.

After incorporating legal feedback, tailor the agreement to align with U.S. compliance standards.

Localization for Jurisdictional Compliance

To make the agreement enforceable in the United States, adapt its terms to meet local regulatory requirements. Since tokenized interests are generally treated as securities in the U.S., the agreement must align with a valid exemption framework [15].

One common approach involves using a Delaware C-Corp for operational purposes (to attract talent and venture capital) alongside an offshore Token SPV for token issuance. This setup can reduce U.S. securities exposure while maintaining flexibility [15]. For private sales under Regulation D 506(c), include provisions requiring purchasers to confirm they are accredited investors, and actively verify their status [16].

Enforce holding periods using technical lockups. Smart contracts with built-in transfer restrictions, such as ERC-1404 or ERC-3643, can automatically prevent token resales during the required 12-month period [16].

Before finalizing, secure a formal token legal opinion in the U.S. This will help address potential liquidity restrictions and regulatory challenges [1]. As Sergei from Terms.law notes:

"The difference between a successful launch and an SEC enforcement action often comes down to one thing: having a comprehensive compliance strategy from day one." [15]

Lastly, address tax considerations. U.S. issuers need to determine if SAFT proceeds are considered taxable income upon receipt or if they can be deferred until token delivery. The IRS may require immediate income recognition, potentially creating tax liabilities before the project is fully funded [16].

Conclusion and Key Takeaways

Key Insights for Founders and Investors

Crafting a token purchase agreement demands precision, fairness, and compliance. The five-step framework outlined earlier highlights the critical components: defining parties and token economics, incorporating vesting and lock-ups, addressing compliance, outlining transfer restrictions and dispute resolution, and finalizing a legally sound document. These steps collectively create a protective framework for both founders and investors.

Choose the right legal instrument for your project’s stage. For early angel rounds, a SAFE with a Token Side Letter is the right fit. For strategic seed rounds where tokens are not yet created, a SAFT works best. Once tokens are pre-minted, a TSA is suitable for private treasury rounds [1][2]. Aligning your legal approach with your project’s development stage is essential to avoid mismatches that could lead to complications.

Ensure fairness and guard against dilution. Anti-dilution clauses are crucial to maintain investor ownership percentages if the total token supply increases during lock-up periods [3]. Adding Most Favored Nation (MFN) clauses ensures early investors are not disadvantaged compared to later participants. As digital assets lawyer Oldrich Peslar notes:

"It is not good for business to give some investors materially better terms than to others… This issue is covered by the most favoured national clause" [3].

These fairness measures also pave the way for meeting regulatory standards. Implementing strong KYC/AML processes and leveraging on-chain analytics to verify fund sources are essential. Additionally, obtaining a Token Legal Opinion in your jurisdiction provides clarity for investors and helps mitigate risks like exchange delistings [1][17]. To further protect investors, set firm deadlines for the Token Generation Event (TGE) and include a "Right of Refund" clause if those deadlines are missed [3].

The Role of Professional Guidance

Navigating the regulatory complexities of Web3 token sales requires expert legal support. Professionals can help determine whether your token qualifies as a security, identify the best jurisdiction for your Token SPV (such as Switzerland, Liechtenstein, or BVI), and ensure compliance with frameworks like Regulation D/S in the U.S. [1][17]. As Nestor Dubnevych, Co-founder and Head of Web3 Legal at Legal Nodes, explains:

"Token Legal Opinion is a legal guarantee for the investor to a certain extent" [17].

Organizations like Bestla VC specialize in providing the legal and regulatory foundation for Web3 projects. Their expertise spans decentralized infrastructure and the Bitcoin ecosystem, helping founders establish a strong legal framework from the start. This reduces risks of enforcement actions and failed launches.

The stakes of non-compliance are high. Consequences can include being forced to return all raised funds or even facing criminal charges [17]. Collaborating with seasoned advisors who understand both the technical and legal nuances of token sales can mean the difference between a smooth launch and a regulatory disaster.

FAQs

When should I use a TPA instead of a SAFT?

A Token Purchase Agreement (TPA) works best for straightforward token sales, especially when the tokens are categorized as utility tokens. This approach can help navigate around the complexities of securities laws.

On the flip side, a Simple Agreement for Future Tokens (SAFT) is more appropriate for pre-sale fundraising. It’s typically used when tokens are treated as securities and are sold to accredited investors before the tokens are fully developed or decentralized.

In short, go with a TPA for utility token sales and simpler compliance. Opt for a SAFT when dealing with securities-related fundraising.

What vesting and lock-up terms prevent a token price crash?

Cliff periods and vesting schedules play a key role in maintaining token price stability. Cliff periods delay token unlocks – commonly 6–12 months for teams and 3–6 months for investors – helping to prevent sudden sell-offs right after a token launch. Meanwhile, linear vesting schedules ensure tokens are released gradually and predictably over time, reducing the risk of market volatility. For some projects, non-linear vesting schedules tied to specific milestones can align token distribution with the project’s progress, further supporting a stable market environment.

How do I structure a U.S.-compliant token sale under Reg D or Reg S?

To set up a token sale that complies with U.S. regulations under Reg D or Reg S, it’s essential to grasp the legal specifics of each exemption. Reg D focuses on accredited investors within the U.S. and mandates filing Form D with the SEC. On the other hand, Reg S permits sales to non-U.S. individuals outside the country without requiring SEC registration. Make sure to create detailed legal documents and work closely with seasoned legal experts to align with U.S. securities laws.