Stablecoins can lose their peg, and when they do, institutional portfolios can suffer massive losses. The March 2023 USDC depeg to $0.87 highlighted how quickly these events can destabilize markets, triggering liquidations and forced sales. With $47 billion in institutional DeFi assets and a $262.3 billion stablecoin market (as of 2026), managing depeg risk is critical.

Here’s how institutions can protect their portfolios:

- Diversify Stablecoin Holdings: Spread assets across fiat-backed (USDC, USDT), crypto-backed (DAI), and real-world asset-backed coins to reduce risk concentration.

- Use Dynamic Rebalancing: Automate adjustments based on market conditions to stay ahead of depegs.

- Leverage Insurance Protocols: Cover against depegs with platforms like Nexus Mutual and InsurAce.

- Deploy Stablecoin Derivatives: Hedge price drops with options and perpetual futures.

- Stress Test Portfolios: Simulate depeg scenarios to prepare for liquidation cascades or collateral issues.

- Monitor Real-Time Data: Use tools like DepegWatch to track liquidity flows, whale activity, and reserve changes.

Key takeaway: A mix of diversification, automation, insurance, and real-time monitoring can minimize losses when stablecoins depeg. Institutions that implemented these strategies saw 89% lower losses during the 2025 downturn. The cost? About 1% of portfolio value annually – a small price for safeguarding capital.

Stablecoin depeg explained. What it means and why it’s dangerous

sbb-itb-c5fef17

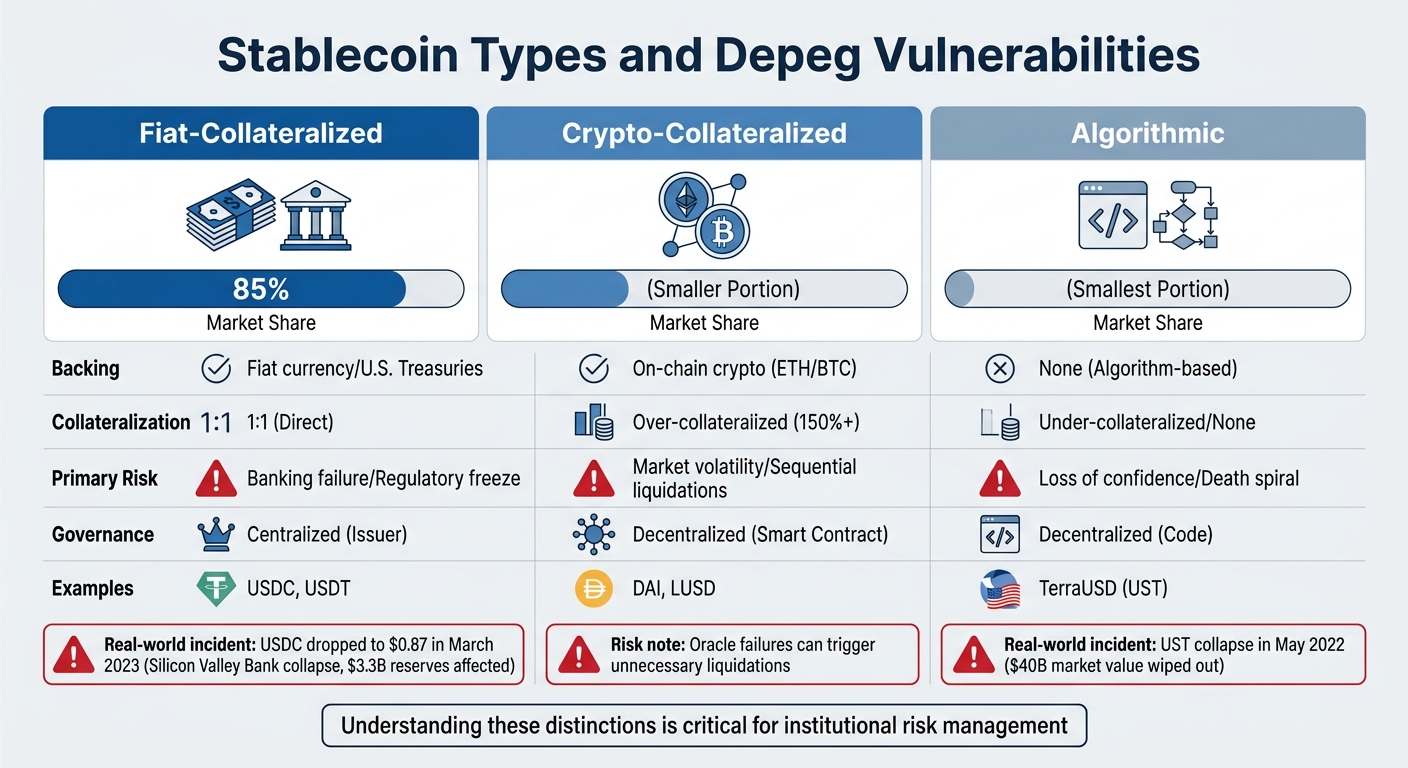

Stablecoin Types and Depeg Vulnerabilities

Stablecoin Types: Collateral Models and Depeg Vulnerabilities Comparison

Grasping the different collateral models of stablecoins is essential for managing risk, especially in institutional settings. Each type comes with its own set of vulnerabilities that can lead to depegging during specific market conditions. This breakdown sets the stage for understanding the hedging strategies discussed later.

Fiat-collateralized stablecoins make up 85% of the market [7]. These are pegged 1:1 to fiat currencies like the U.S. dollar, backed by cash or short-term U.S. Treasuries held by centralized issuers. Examples include USDT and USDC. Their biggest risk comes from counterparty exposure to traditional banks. For instance, when Silicon Valley Bank collapsed in March 2023, USDC dropped to $0.87 because Circle had $3.3 billion of reserves tied up in the bank [2]. Redemption during crises can also be problematic, as users often turn to secondary markets, where prices may deviate significantly [1].

Crypto-collateralized stablecoins, such as DAI, are backed by on-chain assets like ETH or BTC and maintain over 150% collateralization to handle volatility [7]. However, they face risks from sequential liquidations. If the value of the underlying crypto drops sharply, smart contracts automatically liquidate positions to maintain collateral requirements. This process can spiral during a crash. Additionally, if oracles providing price data fail, the system might either liquidate unnecessarily or allow the creation of under-collateralized tokens [2].

Algorithmic stablecoins operate without physical reserves, relying instead on supply adjustments driven by code. These are highly vulnerable to confidence crises, which can lead to a complete collapse. TerraUSD (UST) is a prime example: In May 2022, heavy selling overwhelmed its mint-burn mechanism tied to LUNA, wiping out $40 billion in market value [7].

| Feature | Fiat-Collateralized | Crypto-Collateralized | Algorithmic |

|---|---|---|---|

| Backing | Fiat currency/Treasuries | On-chain crypto (ETH/BTC) | None (Algorithm-based) |

| Collateralization | 1:1 (Direct) | Over-collateralized (150%+) | Under-collateralized/None |

| Primary Risk | Banking failure/Regulatory freeze | Market volatility/Liquidations | Loss of confidence/Death spiral |

| Governance | Centralized (Issuer) | Decentralized (Smart Contract) | Decentralized (Code) |

For institutions, understanding these distinctions is critical for aligning stablecoin choices with effective risk management strategies.

Mapping stablecoin exposure is a must for institutional portfolios. This process helps identify where risks are concentrated – whether from banking system vulnerabilities or sharp market downturns. Such insights are key to shaping the hedging strategies discussed next.

Hedging Strategies for Stablecoin Depeg Risk

To guard against the risks associated with stablecoin depegging, institutions need to implement a mix of strategies. These include diversification, active management, and insurance coverage – all working together to minimize potential losses.

Diversification Across Multiple Stablecoins

Diversifying stablecoin holdings across different types and models is a key way to reduce depeg risk. Relying on a single stablecoin can expose portfolios to vulnerabilities, such as banking failures, liquidation cascades, or algorithmic issues. For this reason, institutions often cap any single stablecoin’s share at 20–25% of their total holdings [10]. For example, during the March 2023 banking crisis, USDC fell to $0.87. Institutions that had diversified into other tokens like USDT and DAI saw much smaller losses overall [3].

Diversification should also include a variety of collateral models. A balanced mix might include fiat-backed options like USDC and USDT, crypto-overcollateralized tokens like DAI and LUSD, and even real-world asset-backed stablecoins like USDY, which can yield 4–6% APR through U.S. Treasury exposure [9]. On top of that, spreading assets across multiple lending and liquidity protocols – such as Aave Arc, Compound Treasury, and Morpho – can reduce the impact of smart contract failures or liquidity issues. For instance, in Q4 2025, a $50 million institutional portfolio diversified across 15 protocols limited its exposure to 5% per protocol. When one protocol suffered an oracle manipulation attack, the portfolio’s insurance coverage paid out $2.3 million, cutting its net loss to just -0.8% instead of a potential 15% [5].

These diversification practices set the stage for active risk management through dynamic rebalancing.

Dynamic Rebalancing Techniques

In volatile markets, static allocations are not enough. Dynamic rebalancing allows institutions to adjust their holdings based on real-time conditions and emerging risks. Automation is critical here – trading bots can reallocate assets immediately when a depeg occurs, avoiding delays [3]. Alerts can be set to monitor deviations: 0.10–0.50% triggers close observation, 0.50–1.50% prompts reducing exposure, and anything above 1.50% demands immediate hedging action [8].

Continuous on-chain monitoring is another essential tool. By tracking liquidity flows, whale movements, and reserve changes in major pools, institutions can stay ahead of potential issues. Tiered monitoring with daily, weekly, and monthly reviews ensures risks are consistently evaluated [8]. Managed vaults, such as those from Sommelier or Yearn, or actively managed funds like Ether.Fi’s Market-Neutral USD Pool, can help automate rebalancing. These tools offer exposure to DeFi yields without requiring in-house trading infrastructure. Pairing these with centralized platform liquidity can further enhance stability during market stress [4].

When even automated rebalancing isn’t enough, decentralized insurance protocols add an extra layer of protection.

Using Decentralized Insurance Protocols

Insurance plays a vital role in shielding portfolios from depeg events. Platforms like Nexus Mutual offer "Depeg Cover", which compensates holders if a stablecoin’s price deviates significantly from its peg (usually $1.00) for a set period – often seven days [11]. As of 2025/2026, this coverage is available for various assets, including Ethena USDe, USDS, Tether USDT0, Resolv USR, and wrapped tokens like WBTC and eBTC.

"The total market cap of stablecoins is over $220 billion. Eliminating the concern around depeg issues should help grow it even further." – Hugh Karp, Founder, Nexus Mutual [11]

Insurance costs depend on the protocol and coverage type. For example:

- Nexus Mutual charges 2–5% annually for smart contract failure coverage.

- InsurAce offers 1.5–4% for smart contract and custodian risk.

- Risk Harbor provides parametric coverage at 0.5–2%.

- Bridge Mutual covers depeg events at 3–7% per year [5].

Allocating around 1% of a portfolio’s value annually for insurance is a common practice. For a $100 million portfolio, this translates to roughly $1 million per year – a reasonable expense to guard against catastrophic depegging events.

When choosing an insurance protocol, ensure it has been audited and has operated on the mainnet for at least six months [6]. Complement insurance with automated threat detection tools like Forta or Hypernative, which provide early warnings of protocol stress or potential depegs. For liquidity providers using automated market makers, pre-programmed exit strategies can further minimize losses. For example, setting a rule to withdraw liquidity if a protocol’s total value locked (TVL) drops by 20% in an hour can mitigate risks [6].

Tools for Risk Mitigation

When it comes to managing depeg risk, institutions need more than broad strategies like diversification or insurance. They require specific tools that allow for real-time risk management. These tools help portfolio managers hedge positions, generate income during volatile periods, and even simulate worst-case scenarios before they occur.

Stablecoin Derivatives

Perpetual futures and options are among the most effective instruments for hedging against price drops below the $1.00 peg. Platforms like GMX, Synthetix, and Lyra enable portfolio managers to take short positions on unstable stablecoins or purchase put options to secure a floor price. For example, if USDC shows signs of stress, a put option can lock in an exit price. Meanwhile, Ethena’s delta-neutral approach combines spot holdings with short perpetuals to capture funding premiums while staying protected against price declines [3][10].

"Speed and precision win in volatile markets" – Tessa Whitman, High-Frequency Trading Specialist [3]

Automated bots can further enhance risk management by executing derivative hedges instantly when a depeg is detected. This avoids delays caused by manual intervention. However, institutions need to keep a close eye on funding rates – high carry costs can diminish the effectiveness of long-term hedges [10].

While derivatives are great for immediate price protection, liquidity strategies offer additional income and risk mitigation.

Liquidity Provision in Stablecoin Pairs

Liquidity strategies can serve a dual purpose: generating income and managing depeg risks. By providing liquidity in stablecoin pairs on decentralized exchanges like Curve Finance or Uniswap v3, institutions earn fee income while also controlling exposure to depegging. Features like concentrated liquidity allow institutions to set tighter ranges around the $1.00 peg, offering more precision than traditional pools. Minor depegs can even turn into a source of revenue, as trading fees offset small price deviations [3][10].

To minimize risks, liquidity providers should establish pre-programmed exit strategies. If a stablecoin’s price moves beyond a set threshold, automated withdrawal rules can help avoid significant impermanent loss and reduce exposure to liquidation cascades [3].

For a more comprehensive approach to risk management, stress testing and simulations are essential.

Stress Testing and Risk Simulations

Monte Carlo simulations and other stress tests allow institutions to model depeg scenarios ahead of time. These tools can uncover hidden risks, such as liquidation cascades triggered by falling collateral values. For instance, during the October 2025 selloff, USDe dropped to $0.65 on Binance. Simulations predicted potential liquidation cascades that could reach $19 billion, far exceeding previous market disruptions [3][12].

Stress tests also aid in fine-tuning protocol parameters like loan-to-value (LTV) ratios and liquidation thresholds. A notable example is Aave’s response during the October 2025 crash. By hard-coding USDe’s price to USDT, Aave prevented wrongful liquidations on its $1.03 billion in USDe deposits. In contrast, Binance’s reliance on a self-referential oracle led to mass liquidations.

"The design of a system’s price oracle is as critical as the inherent peg stability quality of its listed collateral" – LlamaRisk Research [12]

Real-time analytics tools like DepegWatch and Forta further enhance risk management. These tools monitor whale activity, liquidity flows, and reserve changes, giving institutions early warning signs before a full depeg occurs [3].

Case Studies and Practical Applications

These examples show how strategies like diversification and decentralized insurance work in real-world crises.

Case Study: Diversification in an Institutional Portfolio

Take the October 10, 2025 crash as an example. Aave’s oracle design and asset management effectively shielded it from devastating losses. When USDe plummeted to $0.62 on Binance due to an internal oracle failure, Aave’s $1.03 billion in USDe deposits stayed stable. How? Aave pegged USDe’s valuation to USDT instead of relying on volatile spot prices. This approach prevented billions in liquidations, even as Binance experienced a staggering 35% drop [12].

To put this into perspective, Binance’s internal oracle showed a 3,500 basis point deviation (equivalent to a 35% drop), while Chainlink‘s external feed only deviated by 65 basis points. Aave’s strategy – diversifying not just across stablecoins but also among oracle mechanisms and valuation methods – proved invaluable during this period of extreme volatility [12].

Ethena Labs added further proof of the power of diversification during the same event. The protocol managed $894 million in redemptions at full value within just seven hours, thanks to a $1.9 billion stablecoin reserve. By holding liquid reserves across USDT and USDC, Ethena allowed institutional clients to exit positions without relying on disrupted secondary markets [12][13].

Case Study: Using Decentralized Insurance

Structural risk measures go beyond diversification to offer an extra layer of protection. For instance, in February 2025, Bybit experienced a wallet hack. Ethena Labs, however, avoided $30 million in unrealized profit and loss by using off-exchange settlement structures. Their approach involved segregating collateral into bankruptcy-remote trusts managed by vetted custodians. Even though Ethena traded on Bybit, these measures ensured USDe’s collateral remained untouched by the hack [13].

This case underscores an important point: decentralized insurance isn’t just about buying coverage. It’s about reducing risk structurally. By keeping assets off exchanges and in segregated custody, institutions can sidestep insurance claims entirely. For example, during the UST collapse, InsurAce paid out $14 million to covered positions. However, protocols with robust custody arrangements never needed to file claims in the first place [14].

Conclusion

The risk of stablecoin depegging isn’t just a hypothetical – it’s a frequent reality that demands robust strategies to manage. Take the March 2023 USDC drop to $0.87 as a prime example [8]. Even well-established stablecoins can falter under market stress, making it essential for institutional portfolios, often managing hundreds of millions in DeFi assets, to prepare for these disruptions.

Diversification remains the bedrock of managing depeg risks. By spreading exposure across various stablecoin models – like fiat-collateralized options such as USDC and USDT, crypto-overcollateralized solutions like DAI, and even real-world asset-backed alternatives – portfolios gain multiple layers of protection. If one issuer faces a crisis, the others can help absorb the shock and maintain balance.

Adding active hedging to diversification creates a stronger defense against unexpected depegs. Tools like derivatives and automated monitoring systems provide real-time safeguards, turning potential disasters into manageable challenges. Together, these strategies form a comprehensive approach to risk management.

"Risk isn’t the enemy – complacency is. Trade like you’ve seen this movie before." – Jessica, Market Insights Analyst, Phemex [4]

The institutional DeFi market reached $47 billion in Q1 2026, with the total stablecoin market capitalization climbing to $262.3 billion [6][4]. As these markets expand, so does the need for professional-grade risk management. Institutions that adopted systematic frameworks experienced 67% fewer incidents and 89% lower losses during the 2025 downturn [5]. And with implementation costs averaging just 1% of portfolio value annually, the expense is negligible compared to the potential losses from unhedged depeg events.

FAQs

How do I measure my portfolio’s real stablecoin depeg exposure?

To understand your exposure to stablecoin depegging, start by evaluating how much of your portfolio could be impacted if a stablecoin loses its $1 peg. Keep an eye on price fluctuations that deviate from the $1 benchmark and check the underlying mechanism that supports each stablecoin’s value. Calculate the portion of your investments tied to stablecoins that might be affected by significant price instability. Leverage analytics tools to monitor stability metrics in real time, and be ready to tweak your strategy as needed.

What’s the best trigger to rebalance when a stablecoin slips below $1.00?

When the price drops significantly below $1.00, it signals a depeg event – an indicator of instability that requires immediate attention. Such deviations can disrupt portfolio balance and increase risk. To address this, it’s crucial to focus on maintaining stability by keeping a close eye on major price shifts away from the peg.

How much hedge coverage do I actually need for a depeg event?

The amount of hedge coverage you need depends on the stablecoins in your portfolio and their associated risks. Many institutional strategies suggest diversifying across multiple stablecoins and applying structured risk management frameworks. It’s wise to aim for coverage that can absorb major deviations – like 13% or more – based on historical depegging events. Adapting your strategy to address the unique risks of your portfolio is crucial for reducing potential losses.