Reverse convertibles are short-term investment products designed for high-net-worth individuals (HNWIs) seeking higher income in exchange for accepting potential risks. These structured notes offer fixed, often high coupon payments and are tied to the performance of a stock, index, or basket of equities. Here’s how they work:

- Fixed Income: Investors receive regular coupon payments, regardless of the underlying asset’s performance, provided the issuer remains solvent.

- Risk-Reward Trade-Off: If the underlying asset stays above a predefined barrier, investors get their full principal back. If it breaches the barrier, they may receive depreciated shares instead of cash.

- Short-Term Commitments: Typical maturities range from 3 months to 2 years, making them suitable for tactical, short-term strategies.

- Issuer Credit Risk: Returns depend on the financial health of the issuing institution.

While reverse convertibles can generate higher income than traditional bonds, they expose investors to equity-like downside risks and capped upside potential. They perform best in stable or slightly rising markets but can lead to losses if the underlying asset performs poorly. Careful consideration of the issuer’s creditworthiness, market conditions, and the specific terms of the product is essential for successful use in a portfolio.

How Reverse Convertibles Work

Structure and Components

A reverse convertible combines a short-term debt instrument with a fixed, above-market coupon and an embedded put option tied to a reference asset [5]. Essentially, when you invest in one, you’re agreeing to "write" a put option on a reference asset – this could be a single stock, a stock index like the S&P 500, or even a basket of equities. This put option is what allows the issuer to offer higher income compared to traditional bonds [5].

One key feature is the knock-in level, a barrier typically set 20% to 30% below the initial price of the reference asset. This level determines your final payout. If the asset’s price stays above this level during the investment period, you get back your full principal in cash, along with all the coupon payments. On the other hand, if the asset breaches the knock-in level and ends below its starting price at maturity, the issuer will deliver a predetermined number of shares instead of cash, which could result in a loss of principal.

Reverse convertibles are generally issued at $1,000 per security and have maturities ranging from three months to two years [5]. As FINRA explains:

"In exchange for higher coupon payments during the life of the note, you effectively ‘write,’ or give, the issuer a put option on the reference asset" [5].

This setup highlights the balance of risk and reward inherent in reverse convertibles. The dual structure – combining fixed income with exposure to market risk – defines how payouts work and explains the appeal of their higher coupon payments.

Income Generation Through Coupon Payments

The standout feature of reverse convertibles is their coupon payments. These fixed, periodic payments – usually distributed monthly or quarterly – are made regardless of how the reference asset performs, as long as the issuer remains solvent [5].

The coupon rate is closely tied to the volatility of the reference asset. Higher volatility increases the value of the embedded put option, which the issuer compensates for by offering a higher coupon rate [5]. For instance, reverse convertibles linked to volatile tech stocks often promise double-digit yields, while those tied to more stable blue-chip indices may offer lower, but still above-average, returns.

To illustrate, a 15% annual coupon suggests a higher level of downside risk compared to an 8% coupon. This reflects the market’s assessment of the likelihood that the barrier could be breached, potentially leaving you with depreciated shares instead of cash.

It’s important to note that these coupon payments are an unsecured debt obligation of the issuing financial institution – not the company behind the reference asset [3]. Therefore, the issuer’s creditworthiness is critical. Your income stream hinges entirely on their ability to fulfill these obligations, so evaluating their financial health should be a top priority.

sbb-itb-c5fef17

Risk and Reward Analysis

Primary Risk Factors

While coupons can enhance income, they come with a set of risks that need careful consideration.

High coupons often indicate higher risk, which can lead to capital erosion. If the underlying asset falls below the knock-in barrier, you may end up receiving shares at a loss[1]. This is a built-in trade-off of reverse convertibles, balancing higher income potential with the possibility of losing capital.

Another key issue is issuer credit risk. Your returns depend entirely on the financial institution’s ability to meet its obligations. If the issuer faces financial trouble, both your income and principal could be at stake[1].

Liquidity is also a concern. Reverse convertibles typically have limited trading options in secondary markets. If you need to exit early, you might have to sell at a significant discount[1].

Additional risks include call provisions, which allow the issuer to redeem the product early when interest rates drop, and complex tax implications. Returns often combine ordinary income with potential capital gains, making tax reporting more challenging[1].

Evaluating Trade-Offs

Understanding these risks helps clarify the trade-offs involved in reverse convertibles.

Reverse convertibles essentially trade the chance for significant upside in exchange for higher-than-average income, while exposing you to downside risk. The coupon rate itself acts as a risk indicator – higher rates usually mean a greater chance of the knock-in barrier being breached.

Even if the underlying asset performs well, your returns are capped at the coupon rate. In contrast, if the asset falls, losses can hit hard. As summarized by My-Structured-Products.com:

"Reverse convertibles typically produce multiple small gains… for longer periods of time, which are often erased by one large loss" [7].

A study analyzing 3,000 scenarios from 2006 to 2019 found that reverse convertibles offered excess returns over high-yield bonds of less than 7%[6]. However, high-yield bonds outperformed reverse convertibles in many stress scenarios, particularly during the 2008 financial crisis[6]. This difference arises because bonds may recover some value in the event of a default, whereas reverse convertibles are more exposed to declines in the underlying equity – even if the issuer does not default[6].

This strategy only works if you’re confident the underlying asset will stay above the barrier level. Before investing, carefully consider whether you’re prepared to own the reference stock at a potentially lower price if the barrier is breached[1].

Reverse Convertibles Explained | Structured Products Series (Episode 6)

Using Reverse Convertibles in HNWI Portfolios

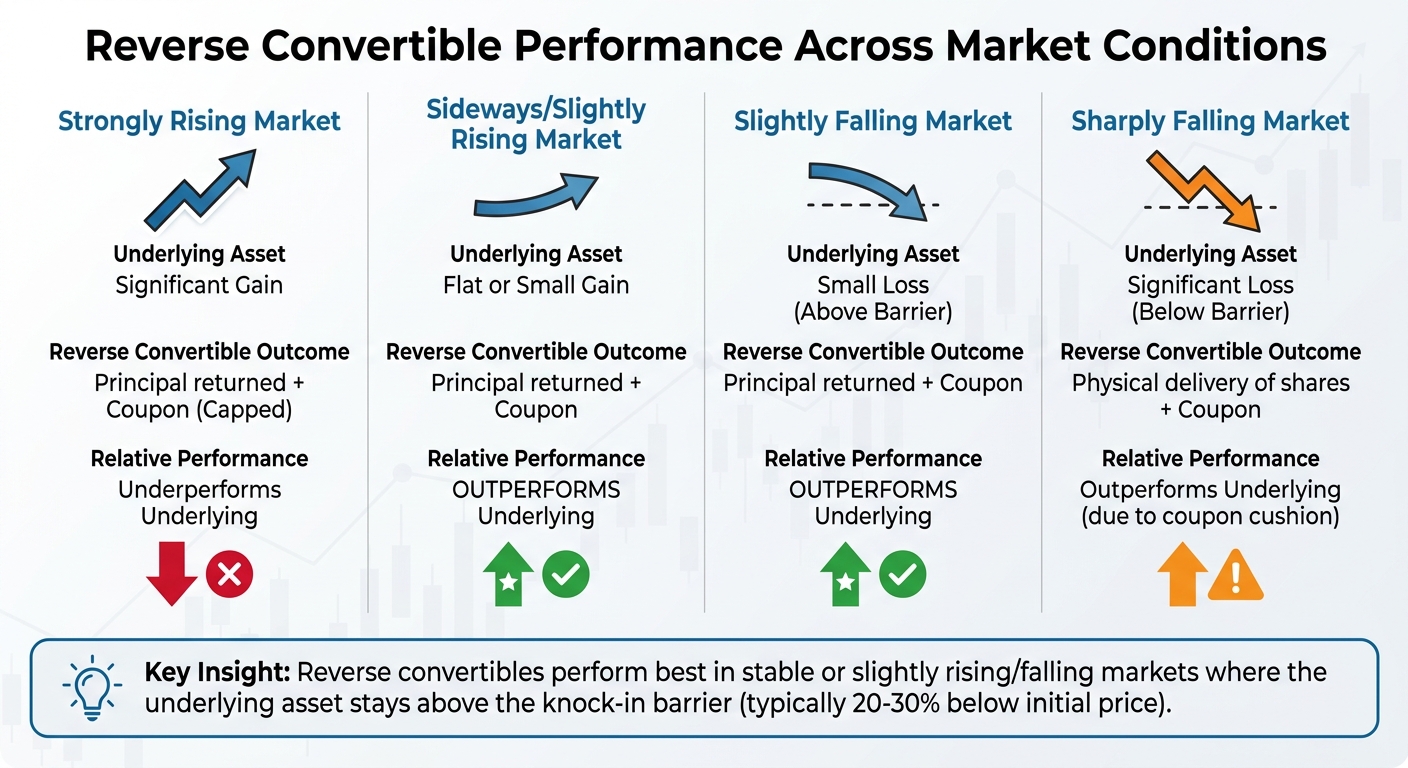

Reverse Convertibles Performance Across Different Market Conditions

Reverse convertibles can be tailored to align with the specific income and risk preferences of high-net-worth investors, offering flexibility through their design features.

Performance Across Market Conditions

The performance of reverse convertibles varies depending on market conditions, making it crucial to assess their suitability for a portfolio. These instruments tend to perform well in sideways or modestly rising markets, where the underlying asset remains relatively stable. In such scenarios, investors collect the full coupon while preserving their principal, often delivering better returns than direct equity investments in flat or slightly rising markets[2].

In sharply rising markets, investors still receive their principal and coupon, but gains are capped, limiting upside participation[2]. On the other hand, in declining markets, the coupon acts as a buffer. If the asset declines but stays above the barrier level, investors retain their principal and receive the full coupon. However, if the asset breaches the barrier, principal loss occurs, though the coupon helps soften the impact[2][7].

| Market Condition | Underlying Asset Performance | Reverse Convertible Outcome | Relative Performance |

|---|---|---|---|

| Strongly Rising | Significant Gain | Principal returned + Coupon (Capped) | Underperforms Underlying |

| Sideways / Slightly Rising | Flat or Small Gain | Principal returned + Coupon | Outperforms Underlying |

| Slightly Falling | Small Loss (Above Barrier) | Principal returned + Coupon | Outperforms Underlying |

| Sharply Falling | Significant Loss (Below Barrier) | Physical delivery of shares + Coupon | Outperforms Underlying (due to coupon cushion) |

Understanding these outcomes helps determine when reverse convertibles can add value to a portfolio.

Design Features: Barriers and Autocalls

The structural features of reverse convertibles allow for customization to meet the specific needs of high-net-worth investors. These features influence both risk and income potential.

Barrier levels are a key design element, determining the point at which principal is at risk. For instance, an 80% knock-in barrier ensures the principal is preserved as long as the asset does not fall below that level[1]. Investors with a more conservative approach may select lower strike levels – below the current market price – to increase the safety margin, though this typically results in a lower coupon yield[7].

Autocallable features provide early redemption opportunities when the underlying asset reaches a predetermined level on specific observation dates. For example, an S&P 500 inverse autocallable issued in early 2025 (SRP ID 50114080) offered a 32% annual coupon with a 100% autocall trigger. It redeemed after just three months when the index fell slightly, delivering an 8% return while the S&P 500 declined by approximately 3%[8]. Similarly, a EuroStoxx 50 inverse autocall (SRP ID 51607755) offered a 6.6% yield with a 135% barrier and a 94% autocall level, safeguarding principal unless the index rose more than 35%[8].

Another useful feature is memory, which ensures missed coupon payments are recovered when conditions improve. For instance, an S&P 500 contingent income note (SRP ID 50698105) provided a 7.85% annual coupon as long as the index remained above 80% of its initial level. Its memory feature allowed for the recovery of previously missed payments, making it particularly beneficial during periods of temporary volatility, assuming eventual recovery[8].

These design elements enhance the adaptability of reverse convertibles, making them a versatile tool for high-net-worth portfolios.

Portfolio Allocation Guidelines

Alignment with Bestla VC Strategies

Reverse convertibles fit well with Bestla VC’s focus on generating yield and tactical income. These instruments combine a debt component with a short put option, allowing returns to stem from embedded option premiums rather than traditional interest payments. Their relatively short-term nature makes them appealing for high-net-worth investors looking to take advantage of favorable market conditions.

However, issuer credit risk is a key consideration, as reverse convertibles are unsecured debt obligations. As highlighted in the Risk and Reward Analysis section, conducting thorough credit evaluations of the issuing financial institution is critical. Beyond this, portfolio-specific allocation factors must be assessed to effectively integrate reverse convertibles into an investment strategy.

Allocation Considerations

To maximize portfolio performance and achieve income-generation goals, allocation decisions must align with broader market conditions, risk tolerance, and diversification principles.

Market Outlook:

Reverse convertibles are most effective when the prices of the underlying assets are expected to remain stable or rise modestly. They tend to underperform in strong bull markets, where gains are capped, and in steep downturns, where losses can mirror those of the underlying equity. In 2018, these instruments accounted for nearly 50% of the structured-product market, with sales reaching approximately $20 billion [6].

Risk Tolerance:

Understanding the risks associated with reverse convertibles is crucial. Despite being referred to as "notes", they expose investors to the same downside risks as the underlying equity, with the coupon serving as the only buffer. As FINRA explains:

"In general, the higher the expected volatility of the reference asset, the higher the fixed coupon or interest payment." [5]

This means higher coupon rates often indicate a greater chance of barrier breaches, where investors may receive depreciated shares instead of cash at maturity. Investors must be comfortable with this potential outcome.

Diversification:

Diversifying reference assets is essential to avoid concentration risk. Selecting underlying stocks, indices, or commodities with low correlation to the broader portfolio can help manage this. Special caution is needed with "worst-of" structures, which base payouts on the poorest-performing asset in a basket, increasing the likelihood of barrier breaches. Typically, knock-in levels are set 20% to 30% below the initial reference price [5], providing some protection based on historical asset volatility.

Investment Timeline:

Reverse convertibles are designed for short-term income generation, with maturities ranging from three months to two years [4]. They are better suited for tactical, short-term strategies rather than long-term holdings. Additionally, they are not ideal for capital that might be needed quickly, as selling in the secondary market before maturity can result in losses, even if the underlying asset’s value remains stable. Tax planning is also an important consideration, as returns typically involve a mix of ordinary income (from the debt component) and capital gains (from the put option component or share tax basis).

Conclusion

Reverse convertibles offer high-net-worth investors a way to achieve higher income, especially when traditional fixed-income yields are falling short [5]. With coupons that often surpass those of standard bonds from the same issuer, these instruments can provide compelling short-term returns – provided the underlying assets remain steady or see modest gains. Additionally, knock-in barriers, typically set 20%-30% below the initial price, provide a layer of downside protection that direct equity ownership does not [5].

However, these benefits come with notable risks. The capped upside limits the potential for capital gains to the fixed coupon, while the downside can be severe if the knock-in barrier is breached. As MSCI analysts Gyorgy Kocsis and István Varga-Haszonits pointed out:

"Reverse convertibles’ limited upside potential is overshadowed by a disproportionately large downside risk, which penalized returns when market conditions became unfavorable" [6].

For Bestla VC’s income-focused strategies, reverse convertibles can serve as a useful tool to complement broader portfolio objectives. Their short maturities, ranging from three months to two years, fit well within tactical, risk-managed approaches. That said, these instruments work best as income enhancers rather than core holdings, and they suit investors who are comfortable with equity-like downside in exchange for higher-than-average coupons.

To use reverse convertibles effectively, strategic positioning and detailed due diligence are critical. Evaluating factors like barrier terms, issuer creditworthiness, and tax considerations is essential for successful implementation. Their popularity among sophisticated investors highlights their appeal [6], but the $1.4 million in FINRA fines for unsuitable sales [4] emphasizes the importance of proper suitability assessments and continuous monitoring within any high-net-worth portfolio strategy.

FAQs

What happens if the barrier is breached?

If the barrier is crossed, you might end up receiving shares of the underlying stock instead of getting your principal back. This can lead to a loss if the stock’s value has fallen below the barrier level. This risk is built into the structure of reverse convertibles, making it crucial to evaluate how this could affect your portfolio before deciding to invest.

How do I assess the issuer’s credit risk?

When assessing the credit risk of reverse convertibles, it’s crucial to examine the issuer’s credit ratings, financial stability, and overall reputation. Typically, these issuers are major banks with investment-grade ratings, which suggest a lower level of risk.

Since reverse convertibles are debt obligations, the issuer’s ability to meet its financial commitments plays a direct role in determining the default risk. Keep an eye on any updates to their credit ratings or signs of financial instability – these could signal changes in the level of risk associated with the investment.

Are reverse convertible coupons taxed as ordinary income?

Yes, reverse convertible coupons are generally taxed as interest income, which falls under the category of ordinary income. It’s always a good idea to consult a tax professional to get advice tailored to your specific financial situation.