Structured notes are hybrid financial instruments that combine a bond with a derivative to offer customized investment outcomes. They balance principal protection and yield potential, but each approach comes with tradeoffs:

- Principal Protection: Safeguards your initial investment (partially or fully) at maturity but limits potential returns. Risks include issuer creditworthiness and inflation reducing real returns.

- Yield Generation: Focuses on higher income through contingent coupons tied to asset performance. However, this exposes you to conditional risks like market declines, capped gains, and issuer default.

Both options have unique risks, including credit risk, limited liquidity, and potential early redemption by the issuer. Your decision should align with your financial goals, risk tolerance, and market outlook.

| Feature | Principal Protection | Yield Generation |

|---|---|---|

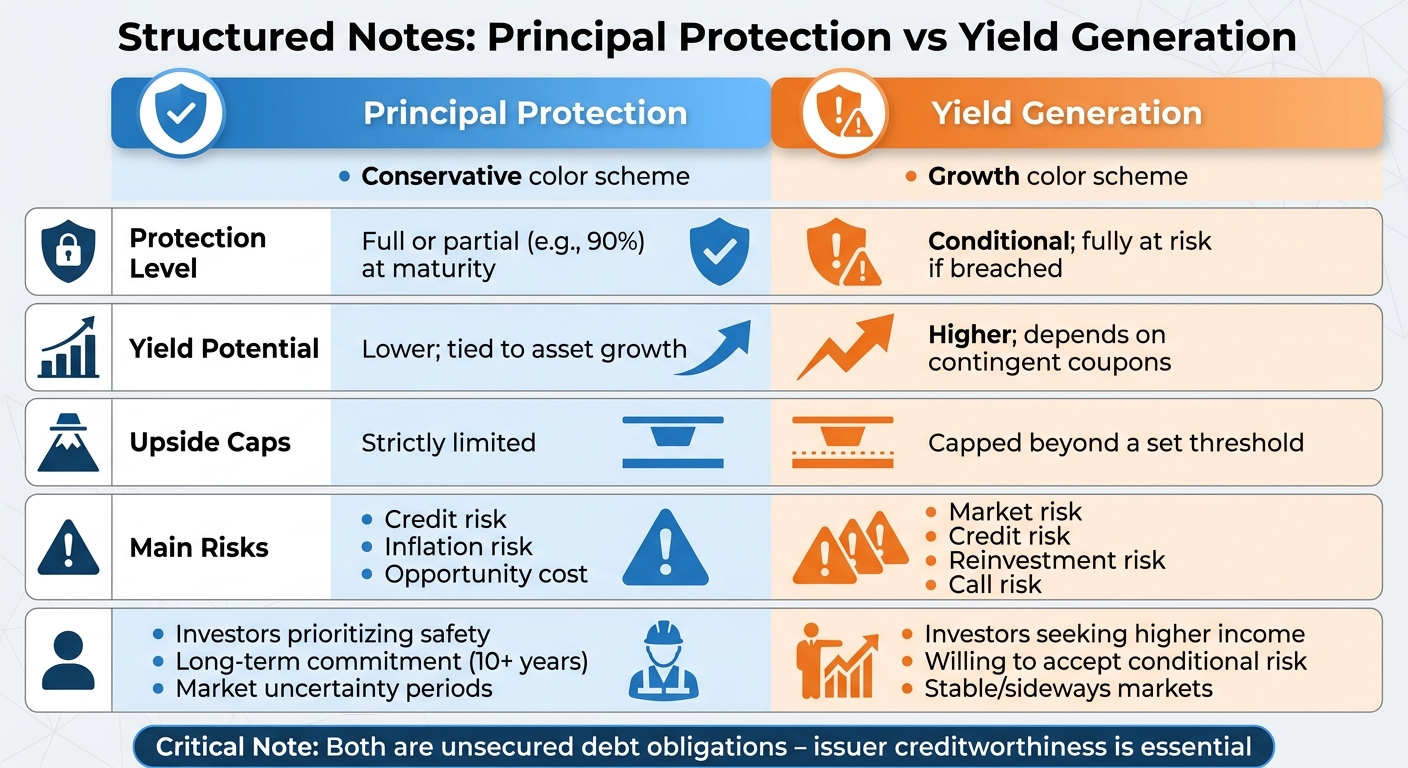

| Protection Level | Full or partial (e.g., 90%) at maturity | Conditional; fully at risk if breached |

| Yield Potential | Lower; tied to asset growth | Higher; depends on contingent coupons |

| Upside Caps | Strictly limited | Capped beyond a set threshold |

| Main Risks | Credit, inflation, opportunity cost | Market, credit, reinvestment, call risk |

Key takeaway: Principal-protected notes are for those prioritizing safety, while yield-focused notes suit investors seeking higher income but willing to accept more risk. Always assess the issuer’s creditworthiness and be prepared to hold until maturity.

Principal Protection vs Yield Generation Structured Notes Comparison

What Are Structured Notes and Are They A Good Investment?

sbb-itb-c5fef17

1. Principal Protection

This section dives into how structured notes safeguard your principal while setting limits on potential returns.

Principal-protected structured notes work by allocating most of the investment into a bond component – typically a zero-coupon bond – to ensure your principal is returned when the note matures. The remainder is used to fund a derivative tied to a reference asset, like an index or stock. The level of protection varies, from full protection (100% of your principal) to partial protection, which can be as low as 10% [3].

Protection Level

The type of protection you choose significantly impacts your risk. With full protection, you’re guaranteed to get 100% of your principal back at maturity, no matter how the reference asset performs – assuming you hold the note to maturity and the issuer remains financially stable. On the other hand, barrier protection (or soft protection) puts your principal at risk if the reference asset drops below a set threshold. Buffer protection (or hard protection) offers a cushion against losses; for instance, with a 10% buffer, your principal only starts to take a hit if losses exceed 10% [3].

| Protection Type | Mechanism | Risk Level |

|---|---|---|

| Full Protection | Guarantees 100% return of principal at maturity regardless of asset performance | Lowest (subject to issuer’s credit risk) |

| Barrier (Soft) | Entire principal is at risk if the reference asset breaches a set threshold | High (if the barrier is triggered) |

| Buffer (Hard) | Losses only impact principal once they exceed a predetermined level | Moderate |

The level of principal protection you select directly affects the note’s potential returns.

Yield Potential and Upside Caps

To fund the cost of principal protection, issuers often limit your upside through capped gains or reduced participation rates. Notes with higher protection levels typically offer lower returns, while those with barrier protection may provide higher potential returns due to the added risk. However, even with full protection, there’s no guarantee of earning a return – your principal will be returned, but if the reference asset doesn’t perform as expected, you might not see any gains.

Additionally, the prospectus often states an initial estimated value for the note that’s lower than its purchase price. This reflects the costs involved in structuring and selling the product. Reviewing the participation rate in the prospectus is crucial – it determines how much of the reference asset’s performance will be credited to your account [3].

While these notes prioritize principal safety, they come with risks that require careful consideration.

Risks

"Any guarantee that your principal will be protected is only as good as the financial strength of the company making that promise." – FINRA [3]

The primary risk with principal-protected notes is credit risk. Since the protection is an unsecured debt obligation, if the issuer defaults, you could lose your entire investment. Another challenge is their limited liquidity – selling these notes before maturity often means accepting a significant discount. Additionally, many notes include autocall features, allowing the issuer to redeem the note early. This could leave you needing to reinvest in less favorable market conditions [3].

2. Yield Generation

Yield-focused structured notes take a different route compared to principal-protected notes. Their goal? To generate income that outpaces traditional bonds. They achieve this by using contingent coupons, which are tied to the performance of an underlying asset, like an equity index or a basket of stocks [1]. But there’s a catch: while these notes aim for higher returns, you trade off full upside participation and take on conditional downside risk to earn that extra income [1].

Protection Level

Unlike fully principal-protected notes, yield-focused products offer conditional protection rather than a guarantee. This protection typically comes in two forms: barriers (soft protection) and buffers (hard protection).

- A barrier safeguards your principal only if the underlying asset doesn’t fall below a set level. If it breaches that level, you lose the protection entirely and are exposed to the full decline. For instance, with a 10% barrier, any loss exceeding that threshold leaves you fully exposed.

- A buffer, however, absorbs losses up to a specific percentage. For example, with a 10% buffer, a 15% drop in the asset means you’re only responsible for the 5% beyond the buffer [3].

Here’s how they compare:

| Protection Type | Risk Profile | Outcome if Asset Drops 50% (with 10% protection) |

|---|---|---|

| Barrier (Soft Protection) | Higher; protection vanishes if the threshold is breached | Investor loses 50% (barrier was breached) |

| Buffer (Hard Protection) | Lower; absorbs losses up to a set percentage | Investor loses 40% (buffer absorbed the first 10%) |

Barriers typically offer higher yields to offset the higher risk of losing protection entirely. Buffers, on the other hand, provide a more stable floor but come with lower yields due to the cost of maintaining that protection. This distinction sets them apart from the fully guaranteed safety of principal-protected notes.

Yield Potential

These notes aim to deliver higher income than traditional fixed-income investments by offering contingent coupons. These coupons are only paid if the underlying asset stays above a certain level – often matching the barrier level. However, this comes with tradeoffs: to fund the enhanced yield and any downside protection, you accept a capped upside and face the risk of earning nothing if market conditions turn unfavorable [1].

"Yield-enhancement notes seek to provide higher income than traditional bonds, often through contingent coupons tied to the performance of an underlying asset." – Russ Zalatimo, Founder, Managing Partner, HUDSONPOINT Capital [1]

Upside Caps

To provide downside protection and higher yields, issuers limit your potential for gains. Even if the underlying asset performs exceptionally well, your return is capped – often at around 10% [1][4]. This ceiling means you won’t benefit from major market rallies beyond that point. For yield-focused investors, this cap represents an opportunity cost, especially during strong bull markets.

Risks

The tradeoffs don’t end with capped upside. Yield-focused notes come with several risks:

- Issuer Credit Risk: These notes are unsecured debt obligations. If the issuing bank defaults, you could lose your entire investment, no matter how well the underlying asset performs [1].

- Liquidity Risk: These investments are designed to be held until maturity. Selling early often means accepting a steep discount, and there’s no guarantee of a secondary market [3].

- Reinvestment Risk: Call provisions can lead to early redemption, forcing you to reinvest at potentially lower rates.

- Path Dependency: In volatile markets, the journey matters as much as the destination. If price thresholds are breached at any point during the term, your outcome can change significantly [1].

"Structured notes are unsecured obligations of the issuing bank. In other words, the investor is exposed not only to the payoff structure but also to the issuer’s creditworthiness." – Russ Zalatimo, Founder, Managing Partner, HUDSONPOINT Capital [1]

Pros and Cons

This section breaks down the key trade-offs between principal protection and yield generation. Your choice will depend on what you’re willing to trade off – security versus potential returns. Each option comes with its own set of benefits and challenges that can shape your investment results.

Principal-protected notes focus on capital preservation, ensuring you receive your initial investment at maturity – provided the issuer remains financially stable. The trade-off? Limited upside potential due to caps or low participation rates. Additionally, fixed returns may struggle to keep up with inflation [3].

On the other hand, yield-focused notes aim to provide higher income via contingent coupons, often surpassing the returns of traditional bonds [1]. But this comes with conditional protection – if a barrier is breached, you could face full downside exposure. There’s also the risk of early calls, which might force you to reinvest at less favorable rates [3].

"Any guarantee that your principal will be protected is only as good as the financial strength of the company making that promise." – FINRA [3]

Here’s a quick comparison of the two approaches:

| Feature | Principal Protection | Yield Generation |

|---|---|---|

| Protection Level | Full (100%) or high partial (e.g., 90%) at maturity [3] | Conditional; principal fully at risk if barrier is breached [3] |

| Yield Potential | Lower; tied to reference asset growth, not fixed coupons [3] | Higher; enhanced income through contingent coupons [1] |

| Upside Caps | Strictly capped or low participation rates (e.g., 70% of index gain) [3] | Capped; appreciation beyond a set limit is forfeited [1] |

| Main Risks | Credit risk, inflation risk, opportunity cost (0% return) [3] | Market risk (downside exposure), credit risk, call risk [3][4] |

Both options are unsecured debt obligations, meaning the issuer’s financial health is critical. Even the best protection features won’t matter if the issuer can’t honor them [3]. Before investing, assess the issuer’s creditworthiness and ensure you’re prepared to hold the note until maturity, as secondary markets may be illiquid or offer steep discounts [3][4].

Conclusion

Deciding between principal protection and yield generation comes down to finding the right fit – aligning the note’s structure with your financial goals, risk tolerance, and view of the market. If safeguarding your initial investment is your top priority and you’re prepared for a long-term commitment (often 10+ years), principal-protected notes could be a solid option, particularly during times of market uncertainty or volatility [3][1]. Keep in mind, though, that this added protection often limits growth potential and may not outpace inflation.

On the other hand, if you’re aiming for higher returns and are willing to accept some level of conditional risk, yield-enhancement notes can offer attractive income opportunities in stable or sideways markets [1]. That said, you need to be comfortable with the chance of losing part or all of your principal if certain thresholds are breached. The best choice will ultimately depend on how well the note’s structure aligns with your financial objectives and the current market environment.

"The effectiveness of any given structured note depends almost entirely on its intent, structure, and context relative to an investor’s portfolio and goals." – Russ Zalatimo, Founder and Managing Partner, Hudsonpoint Capital [1]

Before committing to an investment, it’s critical to assess the issuer’s creditworthiness [3][2]. Confirm the type of protection offered and ensure the note’s maturity aligns with your timeline [3]. Because secondary markets for these notes are often illiquid, be prepared to hold the investment until maturity – or face the possibility of selling at a steep discount [3][4].

FAQs

How do I check the issuer’s credit risk?

When assessing the credit risk of an issuer for structured notes, start by examining credit ratings from agencies such as Moody’s, S&P, or Fitch. These ratings provide insight into the issuer’s financial stability and their ability to meet obligations. Beyond ratings, take a closer look at the issuer’s overall financial health and reputation. Since principal protection hinges on the issuer’s ability to honor commitments, a financially unstable issuer could put your investment at risk.

What happens if I sell a structured note early?

Selling a structured note before it matures comes with liquidity risk and the possibility of losses. While the note might promise principal protection if held until maturity, selling early could lead to poor pricing or penalties. This means you might end up losing part of your investment. Weigh these risks carefully before deciding to sell early.

Barrier vs buffer: which is safer?

In structured notes, a buffer offers a layer of protection against losses by absorbing a portion of the decline in the underlying asset’s value. This means your principal remains protected unless the asset’s drop surpasses a predetermined percentage. On the other hand, a barrier acts as a hard cutoff – once the underlying asset’s value falls below this threshold, it can trigger substantial or even complete loss of principal. Because of this, buffers are generally considered less risky and more appealing to those with a conservative investment approach.