Family offices looking to invest in Tier 1 hedge funds face high barriers like exclusivity, steep financial requirements, and rigorous vetting processes. These funds are known for their size, consistent performance, and advanced strategies, but gaining access requires more than just capital. Here’s what you need to know:

- Key Requirements: AUM of $500M+ is often necessary, along with institutional-level governance, formal investment committees, and accreditation as a qualified purchaser.

- Investment Strategies: Popular approaches include long/short equity, global macro, and quantitative strategies for diversification and wealth preservation.

- Access Routes: Options include managed funds, co-investments, direct allocations, and Separately Managed Accounts (SMAs), each offering different levels of control, transparency, and fees.

- Relationship Building: Personal networks, placement agents, and early commitments (anchor LP strategy) are critical for accessing oversubscribed funds.

- Governance: Strong internal processes, documented decision-making, and thorough due diligence are essential to meet Tier 1 standards.

Why Some Family Offices Quietly Outperform Institutions

sbb-itb-c5fef17

Preparing Your Family Office for Tier 1 Investments

Gaining access to Tier 1 hedge funds requires more than just capital – it demands a robust, institutional-level setup. For most family offices, the threshold for a formal structure begins at $100 million in investable assets. This "rule of $100 million" reflects the level at which in-house investment teams become financially viable, especially when allocations to alternative asset classes exceed this amount. Typically, this means a total AUM of $500 million or more is necessary to meet operational demands and qualify for Tier 1 investments [1][6].

AUM Requirements and Financial Qualifications

Tier 1 hedge funds set the bar high. While family offices generally manage $30 million or more [2], the North American average AUM is closer to $1.5 billion [6]. Most family offices allocate between $1 million and $5 million per fund, with only 13% committing over $10 million [6]. Beyond financial capacity, investors must meet regulatory standards as "accredited investors" or "qualified purchasers" [1].

Liquidity planning is crucial. Hedge fund investments make up roughly 4% to 6% of family office portfolios [6], balancing their appeal for uncorrelated returns against limitations like lock-up periods and redemption gates. For offices with under $500 million AUM, outsourcing to external advisors or multi-family office structures often makes more sense than building costly internal teams [6]. Another challenge: 40% of family offices cite cybersecurity as a significant capability gap during due diligence [6].

Governance and Decision-Making Frameworks

Tier 1 funds expect institutional-grade governance, yet only 56% of family offices have formal investment committees, and just 44% document their investment processes [6]. This lack of structure can be a major obstacle. To meet these expectations, successful offices establish clear decision-making roles:

- Calendar Owner: Manages the investment funnel and timelines.

- Internal Sponsor: Advocates for specific investments.

- Capital Approver: Holds final authority, whether it’s a principal or a committee [8].

"An effective way to attract and retain senior investment professionals within a family office is to align compensation with performance through thoughtfully structured participation."

- Peter G. Naismith, McDermott Will & Schulte [7]

Single-family offices can leverage their agility, often resolving decisions in days compared to the 2–4 months typical for institutions. However, this speed requires standardized playbooks that outline key terms like fee structures, side letter precedents, and non-negotiable conditions. Starting legal reviews early – once near-final documents are available – helps avoid missing critical windows, such as most-favored-nations clauses [7]. With a strong governance framework in place, family offices can better align their investment approach with the demands of Tier 1 hedge funds.

Matching Investment Goals with Hedge Fund Strategies

The first step in alignment is defining specific investment parameters, including asset class, geography, sector focus, and vehicle type [8]. Family offices targeting Tier 1 funds often lean toward long/short equity, global macro, and quantitative strategies, which are known for tail-risk hedging and delivering uncorrelated returns [6]. The key question to evaluate: Does the fund’s strategy align with your goals for alpha generation and preserving multi-generational wealth?

Fee structures also deserve close attention. Negotiate performance hurdles – thresholds funds must meet before incentive fees apply [3]. Ensure that general partners have meaningful personal stakes, often expected to exceed 5%, particularly for emerging managers [6]. Request detailed reporting, such as monthly sector and regional exposure updates, along with notice rights for any changes in strategy or valuation policies [3]. This diligent alignment process not only satisfies Tier 1 fund requirements but also helps protect and grow wealth for future generations.

How to Secure Tier 1 Hedge Fund Allocations

Once your family office has established solid structures and governance, the next step is gaining access to Tier 1 hedge funds. These funds don’t openly advertise openings, so securing a spot requires careful planning, relationship-building, and choosing the right strategy. While institutional readiness is essential, the real challenge lies in navigating the competitive and exclusive world of Tier 1 fund allocations.

Accessing Tier 1 Funds Through Managed Vehicles

Separately Managed Accounts (SMAs) present an alternative to traditional commingled funds or direct investing. Unlike blind-pool funds, SMAs offer significant advantages like position-level transparency, customized fee structures, and the ability to control trade timing and liquidations [14]. However, they come with steep minimum investment requirements, typically between $10 million and $50 million [14].

SMAs also allow family offices to negotiate favorable fees – often lower than the standard "2-and-20" structure – and to request detailed exposure reports. These reports help monitor and manage risk across a diversified portfolio [16]. For family offices seeking transparency and liquidity without the hassle of building an in-house team, SMAs strike a good balance. Beyond managed vehicles, direct investments and co-investment opportunities are other popular routes to consider.

Direct Allocations and Co-Investment Deals

The anchor LP strategy is a key way for family offices to gain access to Tier 1 funds. By committing $5 million to $15 million early in a fund’s lifecycle – typically accounting for 10–20% of the fund – family offices can negotiate better governance visibility and secure co-investment rights [11][13].

"Co-investment rights are the easiest concession. They cost you nothing and family offices value them enormously."

- Cura placement professional [11]

Co-investments serve as a middle ground between passive fund allocations and fully direct investments. They’re hugely popular, with about 83% of family office direct deals taking place as co-investments or club deals [11]. These arrangements allow family offices to select deals that align with their risk preferences, often with reduced or no fees on the co-investment portion [10][13].

Smaller, specialist funds – those managing less than $150 million – are increasingly attractive to family offices following this strategy. These funds often outperform larger platforms, with some delivering an excess internal rate of return (IRR) of 250–350 basis points. Micro-VC funds under $200 million, for example, have achieved a 2.8x TVPI in the upper quartile, compared to 2.1x for larger funds [13]. However, co-investments come with their own risks, such as portfolio concentration, and demand thorough operational due diligence.

To prepare for co-investments, it’s essential to create a 90-day readiness plan. This plan should outline your investment criteria, approval processes, and a standardized approach to reviewing term sheets [10].

"Co-investing is a capacity decision before it is an investment decision."

This preparation ensures your family office has the resources to handle the complexities of deal-specific diligence, legal structuring, and ongoing valuation tracking. When internal capabilities hit their limits, external advisors and placement agents can provide the expertise needed to access Tier 1 funds.

Working with Placement Agents and Advisors

External advisors can complement your internal team, opening doors to exclusive, off-market opportunities. Currently, 52% of family offices collaborate with external partners to manage their assets [4]. This trend reflects the growing demand for institutional-level expertise without the overhead of building a full in-house team. Advisors can assist with everything from complex due diligence to leveraging proprietary networks for access to top-tier managers [14][15].

These consultants often act as an extension of your team, handling legal and accounting aspects of due diligence, negotiating deal terms, and optimizing tax structures. Their ability to provide warm introductions to Tier 1 managers is particularly valuable, as 70% of new manager LPs are sourced through personal networks rather than cold outreach [2].

The push for professionalism in family offices is undeniable. By 2030, family offices are projected to manage $5.4 trillion in assets, with 66% of professionals expecting them to adopt more institutional practices [4]. Specialized advisors can help meet the operational and compliance standards demanded by Tier 1 funds [2][4].

"The differentiator is no longer access alone. It is the ability to integrate sourcing, underwriting, portfolio construction and governance into a coherent framework."

- Joe Samuel, Connection Capital [12]

Evaluating and Monitoring Tier 1 Hedge Fund Investments

Comparison of Tier 1 Hedge Fund Investment Structures for Family Offices

Getting into a Tier 1 hedge fund is just the beginning. The real challenge lies in keeping a close eye on performance, managing risks, and ensuring the fund stays aligned with your family office’s goals. Without a clear system for evaluation, even the most promising investments can veer off track or bring unexpected risks.

Performance Metrics and Risk Analysis

To effectively evaluate performance, you need the right metrics. Use Time-Weighted Returns (TWR) to compare managers, while Internal Rate of Return (IRR or XIRR) gives a clearer picture of your actual investment experience, including cash flow timing [17]. But raw returns alone don’t tell the full story. Dive deeper by assessing risk-adjusted performance through Sharpe ratios, rolling volatility, and return dispersion. Look at maximum drawdown and recovery periods to see how well the fund protects wealth during tough markets [6][17].

Family offices often aim for returns between 8% and 12%, so it’s crucial to monitor whether a manager consistently hits these targets without excessive volatility [6]. Pay close attention to DPI (Distributed to Paid-In) over paper valuations. As Stephen Frangione, Managing Director at Praxis Rock Advisors, explains:

"DPI is the primary quantitative metric, and family offices are particularly skeptical of paper returns because many principals have personal experience with investments that looked attractive on paper but never generated cash."

- Stephen Frangione [9]

Keep an eye on exposure and concentration across sectors, geographies, and themes to identify crowding risks or style drift [3][17]. Also, review liquidity terms like notice periods, lock-ups, and gates. Investor-level gates are generally preferable to fund-level ones [3][17]. Lastly, evaluate the general partner’s (GP) alignment by checking their personal capital commitment. While the industry average is 3.6%, research indicates optimal alignment occurs when GPs commit between 11.5% and 13% [6].

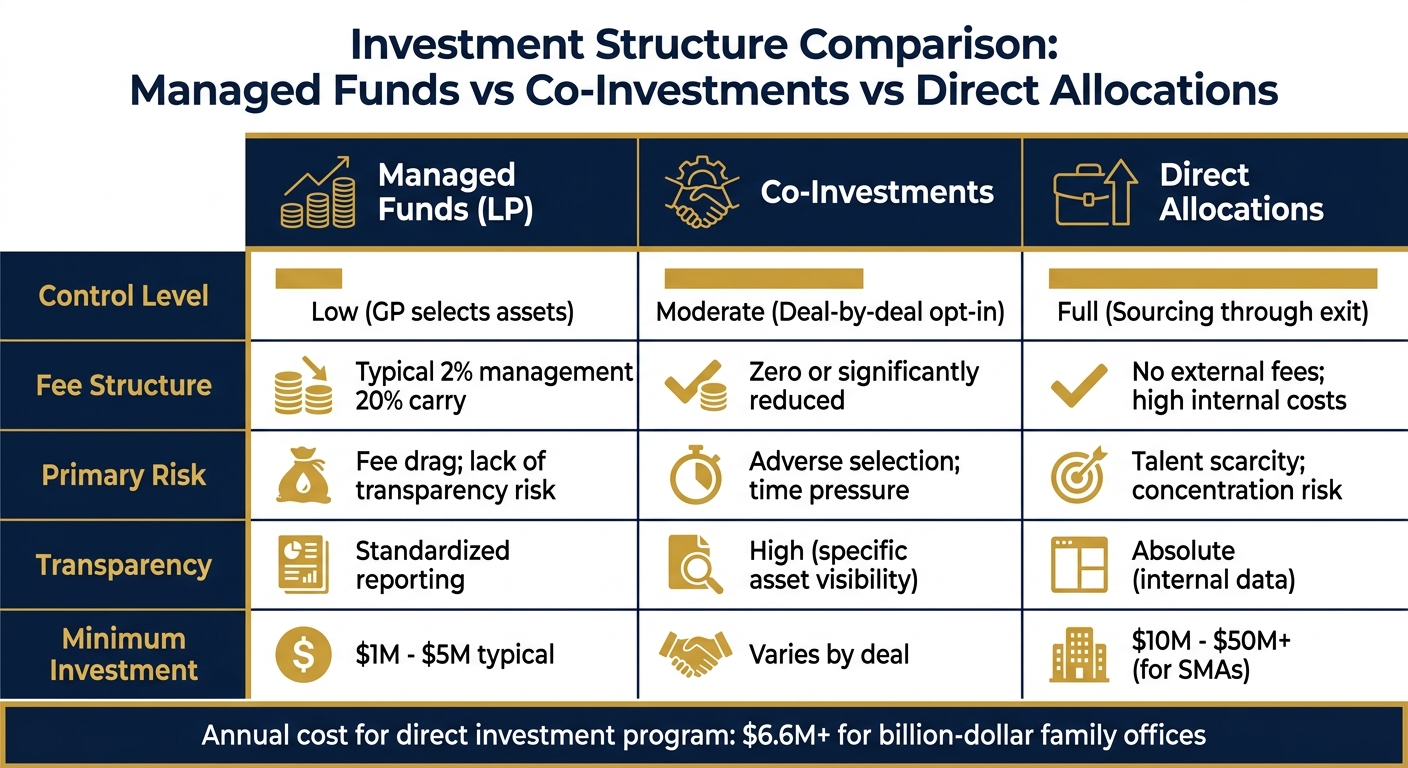

Comparing Investment Structures

The way you access hedge funds – whether through managed funds, co-investments, or direct allocations – comes with trade-offs. Here’s a breakdown:

| Feature | Managed Funds (LP) | Co-Investments | Direct Allocations |

|---|---|---|---|

| Control | Low (GP selects assets) | Moderate (Deal-by-deal opt-in) | Full (Sourcing through exit) |

| Fees | Typical 2% mgmt / 20% carry | Zero or significantly reduced | No external fees; high internal costs |

| Primary Risk | Fee drag; lack of transparency risk | Adverse selection; time pressure | Talent scarcity; concentration risk |

| Transparency | Standardized reporting | High (specific asset visibility) | Absolute (internal data) |

Managed funds are straightforward but offer limited control. Co-investments reduce fees and provide greater transparency, though they come with risks like adverse selection and tight timelines. Direct allocations give maximum control and visibility but can be costly. Running a direct investment program can cost over $6.6 million annually for billion-dollar family offices [18].

Manager Monitoring and Performance Reporting

Effective monitoring requires a structured approach. A three-tier review system works well: monthly checks on liquidity and exposure, quarterly reviews of private markets and performance, and annual deep dives into strategy [19]. Donald Campbell, Partner at Capstone Family Office, highlights the role of modern tools:

"What used to take hours or days is now done in minutes."

- Donald Campbell [17]

Secure side letter rights to get immediate updates on key events like personnel changes, litigation, regulatory issues, or trading halts [3]. As Peter G. Naismith of McDermott Will & Emery explains:

"A side letter is a contract that is meant to be monitored and implemented. If the investor cannot track whether the sponsor is performing its obligations, then it is of little use."

- Peter G. Naismith [7]

Be vigilant about side pockets – these segregate illiquid or hard-to-value assets. Ensure management fees for these assets are based on the lower of cost or fair value, and that incentive fees only apply upon realization [3]. Also, track high-water marks to avoid paying unearned fees [3]. To stay on course, maintain a standardized decision memo for every investment. This should document the original thesis, risks, and valuation approach to avoid drifting from your strategy over time [19].

Conclusion

Summary of Access Strategies

Gaining access to Tier 1 hedge fund allocations requires a well-rounded strategy. Family offices need to focus on internal readiness by establishing institutional-level governance, formalizing investment committees, and ensuring they meet the financial benchmarks expected by top-tier managers. Today, around 34% of family offices allocate over 40% of their portfolios to alternative assets, making the move from informal decision-making to structured processes increasingly critical [5][9].

The paths to access vary depending on resources and desired control. Managed funds offer diversification with less oversight, while direct investments and co-investments provide more transparency and cost efficiency but require faster decision-making and deeper due diligence. Separately Managed Accounts allow for tailored solutions but typically require commitments ranging from $10 million to $50 million [14]. Another approach involves anchoring smaller, specialized managers with commitments of $5 million to $15 million in funds under $150 million, potentially delivering 250–350 basis points of additional IRR while securing favorable terms and priority co-investment opportunities [13].

Intermediaries and relationships are also key. Placement agents, advisors, and introductions through shared co-investors tend to outperform cold outreach. Building authentic, long-term relationships is crucial for gaining access to these coveted opportunities.

These insights lead to actionable steps for family offices looking to optimize their strategies.

Final Recommendations for Family Offices

To effectively implement these strategies, ensure every investment aligns with your long-term goals. Develop a clear "reason now" thesis for each allocation to maintain a sharp focus [8].

Adopt a balanced approach. Combine managed funds for core exposure, co-investments for cost savings, and selective direct investments for greater control. Use the advantage of permanent capital to strengthen your negotiating position, as family offices now contribute nearly 30% of the capital for emerging managers [20].

Continuously improve internal processes, rely on trusted networks, and evaluate performance rigorously. Look for managers with significant personal capital commitments – ideally 3% to 5% of the fund – and prioritize realized distributions over unrealized gains when assessing returns [3][9]. Ultimately, success lies in integrating sourcing, underwriting, portfolio construction, and governance into a cohesive strategy to secure top allocations and preserve wealth across generations.

FAQs

How can a smaller family office get Tier 1 hedge fund access without $500M+ AUM?

Smaller family offices can find ways to connect with Tier 1 hedge funds by focusing on building meaningful relationships and aligning with the fund’s objectives. Trust is a cornerstone here – showing a long-term commitment and even presenting co-investment opportunities can make a big difference.

Another approach is to engage through intermediaries, join specialized networks, or attend industry events specifically designed for family offices. These platforms offer a chance to network and demonstrate value beyond just financial capital. For instance, emphasizing shared themes or offering unique insights can help smaller family offices stand out, even if they don’t meet the usual AUM requirements.

What’s the best way to get into an oversubscribed hedge fund without an existing network?

Accessing an oversubscribed hedge fund without an established network can feel like a challenge, but there are ways to navigate this.

One option is exploring funds of funds or separately managed accounts. These vehicles often provide diversified exposure to some of the most sought-after hedge funds, making them a practical entry point.

Another approach is to focus on building credibility. Conduct thorough due diligence and demonstrate a clear understanding of the fund’s strategy. Aligning your interests with the fund’s goals can make you a more appealing candidate.

You might also consider partnering with family offices or positioning yourself as an anchor investor with emerging managers. These partnerships can open doors and create opportunities to gain access to top-tier funds.

How should we choose between a fund allocation, an SMA, and a co-investment?

When weighing your options between a fund allocation, a Separately Managed Account (SMA), or a co-investment, it’s important to align your choice with your goals, liquidity requirements, and desired level of control.

- Fund Allocations: These offer broad diversification and professional management, making them a convenient choice for many investors. However, they often come with limited control and potential liquidity restrictions.

- Separately Managed Accounts (SMAs): With SMAs, you gain greater transparency and the ability to customize your portfolio. Plus, you directly own the assets, giving you more say in your investments.

- Co-Investments: This route can deliver higher potential returns and hands-on control. On the flip side, it demands thorough due diligence and significant operational resources.

Your decision should ultimately reflect your strategic goals and your capacity to manage the associated responsibilities.