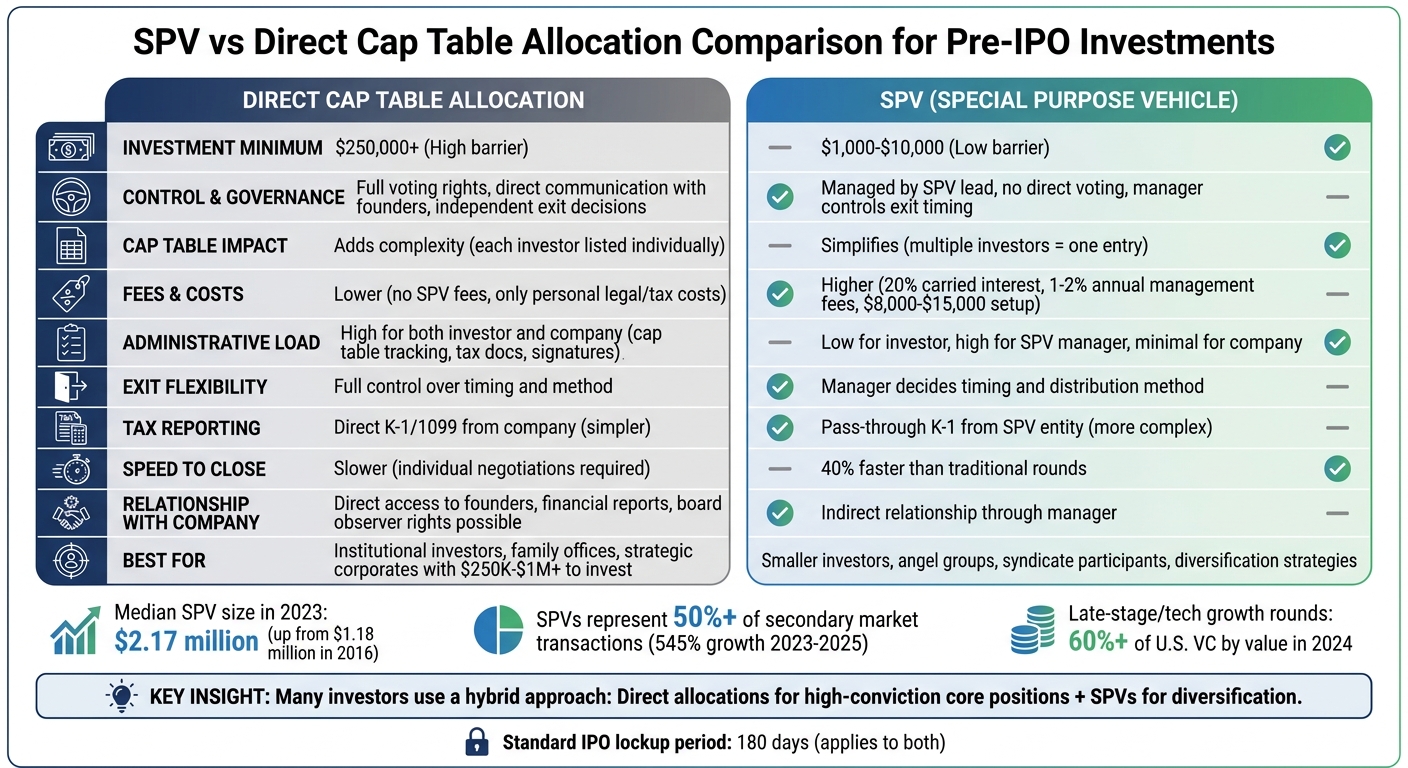

When investing in pre-IPO companies, you have two main options: Direct Cap Table Allocations or Special Purpose Vehicles (SPVs). Each method offers unique benefits and challenges depending on your investment goals, capital size, and desired level of control.

- Direct Cap Table Allocations: You hold shares directly in your name, giving you full voting rights, direct communication with the company, and control over exit timing. However, this requires larger investments (typically $250,000+) and involves more administrative effort.

- SPVs: These pool funds from multiple investors into a single entity, simplifying the cap table for companies. They allow smaller investments (as low as $1,000), faster deal closures, and reduced administrative burdens for investors. But, you give up direct control and face additional fees like carried interest and management costs.

Quick Comparison

| Factor | Direct Cap Table Allocation | SPV |

|---|---|---|

| Investment Minimum | High ($250,000+) | Low ($1,000–$10,000) |

| Control | Direct voting and exit control | Managed by SPV lead |

| Cap Table Impact | Adds complexity for companies | Simplifies cap table |

| Fees | Lower (no SPV fees) | Higher (management and carry fees) |

| Administrative Load | High for investor and company | Low for investor, high for SPV lead |

| Exit Flexibility | Full control over timing | Manager decides timing |

Your choice depends on factors like your available capital, need for direct governance, and how much administrative work you’re willing to handle. Many investors use a mix of both approaches to balance control, diversification, and efficiency.

SPV vs Direct Cap Table Allocation: Complete Comparison Guide for Pre-IPO Investors

What is an SPV? (And Why Your Startup Needs One for Fundraising) 🚀

sbb-itb-c5fef17

What Are Direct Cap Table Allocations?

A direct cap table allocation means you personally hold shares in a company, with your name appearing on the company’s official capitalization table. This involves signing key investment documents, like a Series Preferred Stock Purchase Agreement, directly with the founders. You can hold these shares either personally or through your primary legal entity [7][9]. This setup is important to understand as it lays the groundwork for comparing direct allocations to SPVs (Special Purpose Vehicles) later on.

When you own shares directly, you have full control over your voting rights and decisions, such as selling shares or participating in follow-on funding rounds. You’ll also receive financial reports, operational updates, and possibly even board observer rights directly from the company [7]. As Monty explains:

“Direct investment means you own shares directly, with no additional legal entity between you and the company. This directness simplifies everything from understanding your position to managing tax reporting to executing exit transactions.” [7]

For companies, managing direct investors involves keeping track of details like share types, quantities, prices, and ownership percentages. As the number of shareholders grows, companies often move from basic spreadsheets to specialized tools like Carta or Pulley to handle this complexity [12]. This administrative burden increases with each new investor, as individual signatures are required for every corporate amendment or legal document [3][12]. With that in mind, let’s explore the benefits and challenges of direct cap table allocations.

Benefits of Direct Cap Table Allocations

One major advantage of direct ownership is the control it provides. You can independently decide when to sell your shares on secondary markets or participate in tender offers [7].

Another benefit is cost efficiency. By investing directly, you avoid the fees associated with SPVs, such as formation costs, annual management fees (typically 1.5% to 2%), and carried interest on profits [4][7]. While you’ll still have personal legal and tax reporting expenses, skipping the SPV structure reduces overall costs.

Tax reporting is also simpler with direct allocations. You’ll receive tax documents directly from the company, making the process more straightforward compared to dealing with pass-through entities like LLCs [7]. This simplicity appeals to seasoned investors who make large, high-conviction investments - often $1 million or more [7].

Lastly, direct ownership can strengthen relationships with founders and management. Being on the cap table directly often provides deeper insights into the company’s operations and future plans [7].

Drawbacks of Direct Cap Table Allocations

Despite the benefits, direct allocations come with notable challenges. A key hurdle is the high minimum investment requirement. Many private companies set entry thresholds at $250,000, $500,000, or even $1 million. While some founders lower the minimum to $25,000 to avoid too much fragmentation, this still excludes many smaller investors [2][7].

Another issue is cap table bloat. A large number of individual investors can complicate governance and due diligence, which may deter future IPO underwriters or buyers. To avoid this, companies often limit the number of direct entries on their cap table [2][3][6][9].

Managing direct investments also requires significant administrative effort. Tracking individual cap tables, managing tax filings, and coordinating legal documents demand resources that smaller investors or firms may not have [7]. Companies themselves often need dedicated staff or professional systems to handle these complexities.

Finally, direct allocations can expose investors to concentration risk. With larger investments - often $500,000 to $1 million per company - you face a higher risk if one company underperforms. Achieving proper diversification under this model requires a substantial overall capital base.

These factors highlight the trade-offs of direct allocations, setting the stage for a comparison with SPV strategies in pre-IPO investments.

What Are Special Purpose Vehicles (SPVs)?

A Special Purpose Vehicle (SPV) is a legal entity - commonly set up as a Delaware LLC or Limited Partnership - created for the sole purpose of making a single investment in a specific company during a particular funding round [2][11]. Instead of each investor appearing individually on the company’s capitalization table, they pool their funds into the SPV. The SPV then invests the combined capital into the company, appearing as just one entry on the cap table [2][9].

This setup simplifies things for the company. Instead of managing 20 or 30 individual investors, the company deals with a single SPV entity. As Alon Kapen, a corporate lawyer at Farrell Fritz, P.C., puts it:

“The company deals with one investor; the complexity lives inside the SPV, not inside the startup.” [11]

SPVs streamline the investment process by consolidating multiple investors into one entity, reducing the administrative load for startups. A Syndicate Lead or General Partner oversees the SPV, handling due diligence, negotiations, paperwork, and ongoing management. Meanwhile, individual investors, known as Limited Partners (LPs), contribute funds but remain passive participants - they don’t directly interact with the company or sign documents [2][3].

SPVs also act as “legal islands,” keeping liabilities separate from the underlying company [3]. In 2023, the median SPV managed $2.17 million in assets, a notable increase from $1.18 million in 2016. This growth highlights their increasing role in venture capital [2].

Benefits of SPVs

SPVs offer several advantages, particularly for startups and investors:

-

Simplified cap tables: By consolidating multiple investors into one entity, SPVs make cap tables less complicated. This streamlined structure is especially attractive to late-stage institutional investors and potential acquirers [3][8]. Timothy Carter, Chief Revenue Officer at Marketer, explains:

“By funneling multiple checks into a single SPV, you replace a choir of voices with one clear soprano.” [3]

-

Centralized management: The Syndicate Lead handles all governance tasks, such as signing documents, voting, and corporate consents, on behalf of the group. This eliminates the need to track down individual investors for approvals, saving time and reducing administrative headaches [3][9]. In fact, SPV-backed seed rounds can close up to 40% faster than traditional direct investment approaches in fast-paced tech markets [2].

-

Lower investment barriers: While direct allocations often require minimum investments of $25,000 to $100,000, SPVs may allow contributions as low as $1,000. This opens the door for smaller investors to participate in high-potential pre-IPO deals that might otherwise be out of reach [2][14].

-

Cost efficiency: Platforms like AngelList, Carta, and Allocations have drastically reduced SPV formation expenses - by as much as 80–90% compared to traditional legal fees a decade ago [10]. Today, setup fees range from $8,000 to $15,000, and standard legal agreements make the process quicker and more predictable [2][10].

Drawbacks of SPVs

While SPVs offer clear benefits, they also come with some limitations:

- Indirect ownership: Investors don’t hold shares directly in the company. Instead, they own a stake in the SPV, which holds the shares. This structure means no direct voting rights, limited access to company updates, and no ability to independently sell the investment [14]. All decisions are made by the Syndicate Lead on behalf of the group.

- Additional fees: SPVs often charge a 20% carried interest on profits and annual management fees of 1–2% of committed capital [2][10]. Some platforms also add one-time administrative fees of 2.5% to 4% [2]. These layers of fees can significantly cut into returns, especially if the investment performs well.

- Complexity in secondary markets: In high-demand secondary markets, like SpaceX, shares may pass through multiple SPVs, each adding fees and obscuring ownership. For example, in March 2026, investors like Tejpaul Bhatia, former CEO of Axiom Space, purchased SpaceX shares through layered SPVs because direct shares were unavailable.

- Reliance on the Syndicate Lead: The Syndicate Lead has control over all key decisions, including exits, follow-on investments, and secondary sales. If the lead makes poor choices or becomes unresponsive, passive investors have limited options for recourse.

SPVs are a powerful tool for simplifying investments and expanding access, but they require careful consideration of these trade-offs.

How SPVs and Direct Allocations Differ

Grasping the differences between SPVs (Special Purpose Vehicles) and direct allocations is essential for institutional investors fine-tuning their pre-IPO strategies. At the core, the distinction lies in ownership: direct allocations provide individual share ownership, while SPVs offer ownership in a separate legal entity. This impacts governance, tax considerations, and exit strategies, shaping how investors engage with their investments.

When it comes to governance and control, the two structures are worlds apart. Direct shareholders receive proxy statements and annual reports directly from the company. They have voting rights on corporate matters and can independently decide their course of action during liquidity events like IPOs or tender offers. On the other hand, SPV investors depend on the manager to handle voting rights, share company updates, and decide on exit strategies. As Allocations explains:

“From the company’s perspective, the SPV is one investor among several, indistinguishable in the cap table from a direct institutional investor.” [9]

Administrative responsibilities also vary significantly. Direct investors must manage cap tables, transfer agents, and tax documentation on their own. SPVs, however, streamline these processes. The SPV manager consolidates administrative tasks and provides summarized reports to investors, though this comes at the cost of reduced direct control.

SPVs vs. Direct Allocations

| Factor | Direct Cap Table Allocation | Special Purpose Vehicle (SPV) |

|---|---|---|

| Cap Table Complexity | High; each investor is listed individually. | Low; multiple investors are grouped under one entity. |

| Investor Minimums | High (typically $250,000+). | Low (typically $1,000–$10,000). |

| Governance | Direct; investors vote and receive updates directly. | Indirect; the manager handles voting and communication. |

| Liability | Direct shareholder liability. | Limited; structured to isolate risk. |

| Admin Overhead | High for the company (e.g., managing numerous K-1s). | High for the manager; minimal for the company. |

| Tax Reporting | Direct K-1/1099 from the company. | Pass-through K-1 issued by the SPV. |

| Exit Control | Investors control their own exit timing. | Manager determines exit timing and method. |

| Speed to Close | Slower; requires individual negotiations. | Faster; up to 40% quicker than traditional rounds [2]. |

In the next section, we’ll dive into scenarios where each structure aligns with specific investment objectives.

When to Use Direct Cap Table Allocations

Direct cap table allocations work best for investors who meet high minimum investment thresholds and want a direct say in the companies they back. This approach is particularly suited for institutional investors, family offices, and strategic corporates making investments ranging from $250,000 to over $1 million. At this level, the cost of SPV (special purpose vehicle) management fees often becomes hard to justify, making direct ownership a more practical choice [7].

One of the biggest advantages of direct allocations is the enhanced governance and communication it allows. Lead venture capital firms, sovereign wealth funds, and strategic corporate investors often choose this route to negotiate primary deal terms, secure board seats, and establish direct lines of communication with the founders [9]. GoMonty highlights this benefit:

“Direct shareholders build direct relationships with company management and fellow investors. These relationships can create opportunities for follow-on investment, access to founder networks, and deeper understanding of the company’s evolution.” [7]

Another significant perk is the ability to maintain full control over exit timing. For example, this proved advantageous when Stripe reached a $91.5 billion valuation through a tender offer [4]. These factors make direct cap table allocations a compelling option for certain strategic scenarios.

Direct Allocation Use Cases

Direct cap table allocations shine in situations where investor size and governance influence are priorities. Lead institutional investors writing checks of $1 million or more often use this structure to negotiate terms such as valuation, share classes, and board representation. A couple of noteworthy examples include:

- OpenAI, which raised $6.6 billion in October 2024 at a $157 billion valuation, relied on direct allocations for lead venture firms committing $200 million or more.

- Databricks, which secured $10 billion in funding at a $62 billion valuation, attracted institutional investors contributing between $25 million and $75 million [9].

Family offices also lean toward direct investments when making larger commitments or when simplicity and control are top priorities. Matthew Wilson, Managing Director at Allied Venture Partners, explains:

“For very small rounds, single-lead investors, or when simplicity is paramount, direct investment may be more appropriate than introducing the SPV structure and associated costs.” [2]

Even large-check angel investors - those who can meet minimum direct investment thresholds, usually between $25,000 and $1 million - benefit from this approach. Direct allocations simplify tax reporting, as documents come straight from the company rather than through an intermediary [2][7][14].

When to Use SPVs

SPVs (Special Purpose Vehicles) are ideal for pooling smaller investments, helping investors access deals that would otherwise be out of reach due to high minimum thresholds. This approach is particularly useful for venture capital firms syndicating investments across their networks, angel groups combining their resources, and institutional investors joining oversubscribed rounds without having to meet steep minimums independently. By pooling funds, SPVs not only simplify meeting these thresholds but also help maintain a clean cap table.

One of the standout advantages of SPVs is their ability to streamline cap table management. This is especially crucial for late-stage deals, where founders often prefer dealing with a single, consolidated investor. Alon Kapen, Partner at Farrell Fritz, P.C., highlights this benefit:

“One SPV is much easier to deal with than twenty individual angels, particularly when it comes time to raise the next round” [11].

This simplicity becomes even more important in late-stage investments, where institutional investors closely examine cap table structure before committing funds.

SPVs also make it easier for investors to participate in high-demand rounds by pooling resources to meet high minimum investment requirements. For instance, companies like OpenAI or Databricks may set minimum check sizes between $250,000 and $1 million. Smaller institutional investors can use SPVs to combine their funds and meet these thresholds. In fact, late-stage and technology growth rounds made up over 60% of the total U.S. venture capital deployed by value in 2024, with many of these deals relying on SPV structures to manage investor participation [9].

Another advantage of SPVs is their ability to help investors exercise pro-rata rights. By sharing the costs of follow-on rounds with co-investors through an SPV, investors can maintain their ownership percentages without heavily depleting their main fund’s reserves [3][9].

SPV Use Cases

SPVs aren’t just about pooling funds or managing large check sizes - they offer flexibility for a variety of strategic goals. One common use is syndicating smaller check sizes. For example, platforms like Allied Venture Partners allow angel investors to participate in premium deals with as little as $1,000. This opens up opportunities that might otherwise be out of reach for many investors [2]. The growing popularity of SPVs is evident, with the median SPV on platforms like Carta managing $2.17 million in assets in 2023, compared to $1.18 million in 2016 [2].

Another key benefit is facilitating carried interest. Syndicate leads can earn 15–20% of profits on a deal-by-deal basis, creating strong incentives for sourcing and managing investments [2]. As Forbes aptly put it:

“SPVs went from an edge case to a core strategy” [11].

Emerging approaches, such as tokenizing LP interests and using layered SPVs, are also gaining traction. These strategies make it easier to transfer interests and access exclusive deals, though they require careful attention to regulatory considerations [7][15][16]. Additionally, automated platforms can fund SPVs in as little as 2–3 weeks, enabling rounds to close up to 40% faster than traditional direct investments [2]. In oversubscribed rounds, this speed can be the deciding factor in securing allocations.

Cost, Tax, and Administrative Factors

The financial and administrative challenges of SPVs compared to direct allocations can vary greatly. Understanding these differences is key for investors deciding which structure suits their needs.

Cost Breakdown

The cost of forming SPVs has dropped significantly in recent years. Michael Kaufman, Founder & Editor-in-Chief at VC Beast, highlights this shift:

“The total cost of forming an SPV has dropped dramatically: platforms like AngelList charge $8,000-15,000 per SPV (down from $25,000-50,000 in legal fees a decade ago).” [10]

Direct investments, while avoiding SPV formation fees, can rack up legal and administrative costs when managing multiple investors. For companies handling dozens of individual investors, these expenses can quickly escalate due to the need for collecting signatures, amending documents, and maintaining constant communication. Timothy Carter, Chief Revenue Officer at Marketer, explains:

“Each avoided legal hour roughly equals a few thousand dollars… those savings extend your runway and let you focus on product sprints instead of line-item audits.” [17]

SPVs simplify this process by consolidating interactions into a single administrative workflow [9]. However, they do come with their own fees - typically $1,000–$5,000 in annual administration costs and a management fee of about 2% of committed capital. For larger investors pledging $2 million or more, direct investment may be more appealing, as it avoids SPV fees and the standard 15–20% carried interest [7].

While costs are a major consideration, tax and compliance requirements also play a critical role in differentiating these structures.

Tax and Compliance Requirements

Tax reporting and compliance obligations create additional distinctions between SPVs and direct allocations. SPVs, as pass-through entities, require participants to file annual Schedule K-1 forms and necessitate Form 1065 filings with the IRS [13]. In contrast, direct allocations offer simpler tax reporting, as investors receive documentation directly from the company.

SPVs also come with regulatory obligations. Managers must file SEC Form D and state-level Blue Sky filings for investors in various states [13]. Brian Hall, Managing Partner at Traverse Legal, cautions:

“Without the right legal and tax infrastructure, the benefits [of SPVs] collapse under regulatory burden or administrative complexity.” [13]

Institutional investors often require SPVs to set up Delaware or offshore “blocker” corporations to protect against Unrelated Business Taxable Income (UBTI), which can arise from debt-financed returns. In contrast, direct investments shift these compliance tasks to the target company’s legal team, potentially introducing their own set of administrative hurdles [9].

Liquidity and Exit Planning

When it comes to exit strategies, SPVs and direct allocations take very different paths. These differences affect how investors access the secondary market and handle post-IPO distributions, making it essential to carefully consider your exit plan when deciding on an investment structure.

SPVs and Secondary Market Liquidity

SPVs have become a dominant force in the secondary market, now accounting for over 50% of transactions - a staggering 545% growth between 2023 and 2025 [20][19]. This boom highlights the efficiency of SPVs in transferring membership interests via specialized platforms, giving investors a way to exit before an IPO.

The pace of these transactions has also ramped up significantly. Alexandre Covello, Founder of Venture Secondaries, describes the shift:

“It used to take 2-3 months to raise an SPV for secondaries. Now? You need to be capital-ready in 1-2 weeks or you’re out.” [19]

This rapid timeline underscores the need for upfront exit planning. Institutional interest is a big driver here - 72% of family offices were investing in secondaries by 2025, up from 60% in 2023 [19]. For high-demand assets, like leading AI companies, SPVs can even trade at 30% premiums over the latest funding round price [19].

When an IPO finally happens, SPV managers handle the heavy lifting. They can either distribute shares “in-kind” to investors’ brokerage accounts or sell them after the lockup period and distribute the cash proceeds. This centralized process avoids the risk of a “fire sale”, where individual investors might flood the market with shares all at once. However, investors give up control over the timing and method of the exit. Jack Berger, Investor at Augment, cautions:

“Because of lockups and manager discretion, IPOs do not always mean instant liquidity for LPs.” [5]

The standard 180-day IPO lockup period applies to both SPVs and direct allocations, but SPV distributions are further delayed until the vehicle itself is allowed to sell or transfer shares [5].

While SPVs simplify the exit process, direct allocations bring their own set of complexities and benefits.

Direct Allocations and Exit Execution

Direct investors have the advantage of controlling their exit timing, as they can independently sell shares on secondary markets [7]. But this freedom comes with hurdles. Companies often enforce Right of First Refusal (ROFR) and transfer approval processes, which can slow or even block sales [20]. Each transaction requires company consent, creating delays that SPVs typically avoid.

These challenges become even more pronounced during acquisitions or IPOs. For example, a cap table with twenty individual seed investors requires signatures from every one of them, whereas an SPV consolidates that into a single line item needing just one signature. Timothy Carter, Chief Revenue Officer at Marketer, points out:

“A cap table showing twenty individuals from the seed round spooks them; a cap table showing one SPV for that same block of equity looks tidy and predictable.” [3]

Direct investors are also responsible for managing cost basis, tax reporting, and brokerage accounts when exiting. They receive documentation directly from the company, which simplifies tax reporting compared to SPVs but shifts the administrative load entirely onto the individual [5].

From the company’s perspective, dealing with hundreds of shareholders during a distribution can be a logistical nightmare. Matthew Wilson, Managing Director at Allied Venture Partners, explains the efficiency of SPVs:

“Distributing proceeds through a single SPV is far more efficient than managing distributions to hundreds of individual shareholders.” [2]

The choice boils down to priorities: direct allocations offer autonomy and control for individual investors, while SPVs streamline the process and provide easier access to secondary markets, though at the expense of personal decision-making. Deciding which path to take depends on whether you prioritize independence or prefer a more hands-off, manager-led approach.

Guidance for Institutional Investors

When deciding between SPVs and direct allocations, institutional investors should align their choice with their strategic goals, investment mandates, and operational capacity. Each structure offers distinct advantages depending on the fund’s priorities and constraints.

Start by reviewing your fund’s concentration limits and mandate restrictions. For funds with strict caps on single-asset exposure, SPVs act as sidecars, keeping these investments separate from the main fund and preventing policy breaches [18]. This setup is particularly useful for follow-on rounds or high-conviction opportunities. On the other hand, if you’re considering a core position of $1 million or more, the typical SPV management fees (averaging 1.9% annually in 2023) might be harder to justify [25,26]. In such cases, direct allocations can be more cost-effective and foster stronger relationships with company founders.

Governance and information rights also play a crucial role. Direct shareholders gain access to financial statements, board observer rights, and proxy materials directly from the company [7]. SPV investors, however, receive these rights indirectly through the SPV manager, creating a layer of separation. For pension funds governed by ERISA or other fiduciary standards, SPVs with clear voting provisions, audited financials, and robust reporting can ensure compliance [9]. To further enhance investor protection, verify that your SPV manager is FINRA-registered [7]. Once governance and fee considerations are addressed, operational capacity becomes the next key factor.

Managing direct investments requires significant operational resources. Your team will need to handle cap table monitoring, tax documentation, coordination with transfer agents, and information flow management [7]. If these resources are unavailable, SPVs can simplify the process by consolidating administrative tasks under a single manager. However, this convenience comes at the cost of reduced control, as SPV investors depend on the manager for liquidity events like secondary sales or tender offers, which could face delays [7].

A balanced approach often involves a hybrid strategy. Use direct allocations for high-conviction, core positions where maintaining direct relationships with founders and voting control outweighs the administrative effort. Meanwhile, SPVs can be used for broader diversification. For instance, instead of allocating $500,000 to two direct investments, you could spread the same amount across ten SPVs at $100,000 each, reducing concentration risk [7]. This hybrid approach combines the strengths of both structures, allowing for a more flexible and diversified portfolio.

The next section will bring together these insights to offer final recommendations for structuring pre-IPO allocations.

Conclusion

Choosing between SPVs and direct cap table allocations comes down to your investment goals, operational capacity, and portfolio strategy. Direct allocations provide full control, direct relationships with founders, and simpler tax reporting. However, they typically require larger investments - often ranging from $250,000 to $1 million or more [7]. On the other hand, SPVs simplify entry by pooling multiple investors into a single line item, with minimum investments often as low as $1,000 to $5,000 [1][2]. These differences impact not just the financial commitment but also the cost, speed, and administrative workload involved.

SPVs are particularly useful for maintaining cleaner cap tables and avoiding the SEC’s 2,000-holder registration threshold [20]. They also offer efficiency - SPV-backed seed rounds can close up to 40% faster, which can be a critical advantage in competitive deals [2].

Administrative demands are another key consideration. If your team isn’t equipped to handle tasks like cap table monitoring, tax documentation, and coordination with transfer agents, SPVs can offload these responsibilities to a single manager [7]. However, this convenience comes with trade-offs, such as relying on the manager for updates, voting decisions, and exit timing - something not every investor is comfortable with.

Both structures have their own advantages and challenges, and a hybrid approach may offer the best of both worlds. As Monty [7] explains:

“The goal isn’t choosing between direct investment and SPVs - it’s using both thoughtfully to construct portfolios that reflect your specific objectives, resources, and risk tolerances.”

For instance, you might use direct allocations for high-conviction investments where close relationships with founders and direct voting rights are critical. Meanwhile, SPVs can help you diversify across more opportunities. For example, instead of investing $1,000,000 in two $500,000 direct positions, you could spread it across ten $100,000 SPV positions for broader exposure.

FAQs

How do I choose between an SPV and a direct allocation?

Choosing between an SPV and a direct allocation comes down to your investment strategy, the complexity of the deal, and how you plan to manage operations.

SPVs (Special Purpose Vehicles) are a great choice when you want to streamline cap table management. By grouping multiple investors into a single entity, SPVs can cut down on legal and administrative work, making them especially useful for larger or syndicated investments.

On the other hand, direct allocations are better suited for smaller, straightforward deals where maintaining direct relationships with individual investors is a priority. They provide more control and are often favored when simplicity outweighs the need for consolidation.

When deciding, think about the number of investors involved, the size of the deal, and how it aligns with your broader investment goals.

What fees should I expect in an SPV deal?

When setting up an SPV, formation and setup costs usually fall between $5,000 and $25,000. This range typically includes expenses like legal fees, administrative charges, and filing costs. Beyond the initial setup, there are also ongoing administrative and compliance fees to consider. The exact costs will depend on how complex the SPV is and the specific services needed to manage it.

What are the biggest risks of relying on an SPV manager?

Relying on an SPV manager comes with several risks that investors should carefully consider. These include mismanagement of funds, conflicts of interest, and lack of transparency.

When funds are poorly managed or when the manager’s incentives don’t align with investors’ goals, it can result in financial losses or even legal complications. Conflicts of interest can also surface if the manager focuses more on maximizing fees rather than delivering strong performance. On top of that, inadequate reporting can leave investors in the dark, making it difficult to monitor the status and performance of their investments.