Feeder and master funds are two key components of a commonly used investment structure in Web3 venture capital. Feeder funds collect capital from different investor groups, while the master fund consolidates these investments into a single portfolio to manage trading and asset allocation. This setup simplifies operations for fund managers and provides tax advantages for investors.

Key Takeaways:

- Feeder Funds: Act as entry points for investors and cater to specific tax and jurisdictional needs. They pool contributions into the master fund but do not directly manage investments.

- Master Fund: The central hub for portfolio management and trading. It holds all assets and executes a unified investment strategy for the combined capital from feeder funds.

- Benefits: Centralized management reduces costs, simplifies compliance, and improves efficiency. Offshore feeder funds help non-U.S. investors and U.S. tax-exempt entities avoid certain tax burdens.

Quick Comparison:

| Feature | Feeder Fund | Master Fund |

|---|---|---|

| Role | Aggregates capital from investors | Manages portfolio and executes trades |

| Asset Holding | Owns shares in the master fund | Holds the actual investments |

| Investor Type | Targets specific groups | Combines all feeder contributions |

| Tax Considerations | Adjusted for investor jurisdiction | Generally tax-neutral |

| Control | Passive; relies on master fund decisions | Full control over investment strategy |

This structure is ideal for funds with diverse investor bases, combining U.S. taxable individuals, non-U.S. investors, and U.S. tax-exempt entities. However, for simpler setups or illiquid strategies, alternative structures may be more suitable. Understanding these dynamics is crucial for aligning investment goals with the right fund structure.

Master-Feeder Fund Structure: Capital Flow and Key Differences

How Master-Feeder Fund Structures Work

Basic Structure

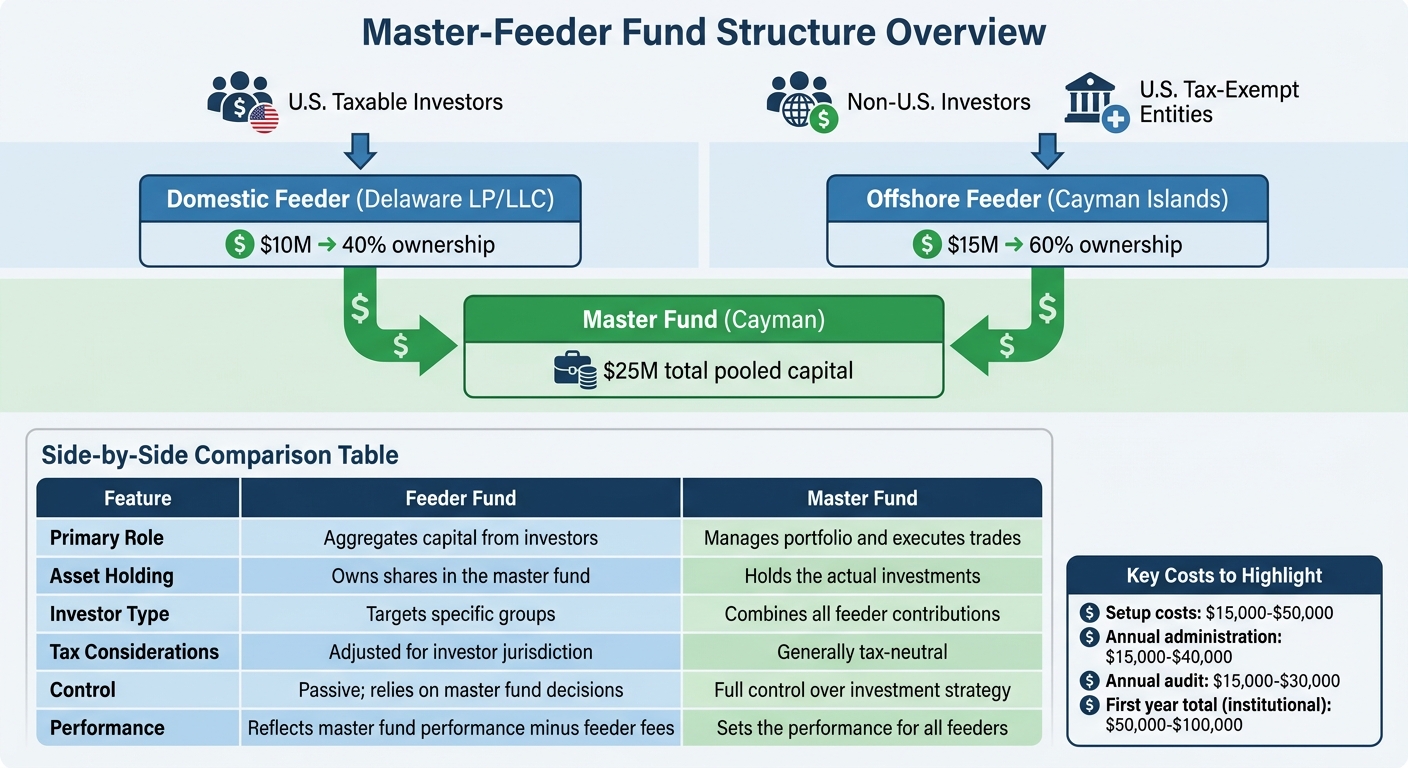

A master-feeder structure involves two or three distinct legal entities. At the top are the feeder funds – typically, one domestic feeder (often organized as a Delaware LP or LLC) and one offshore feeder (commonly structured as a Cayman Islands exempted company). At the bottom is the master fund, which can be set up as a Cayman company or a partnership. The domestic feeder is designed for U.S. taxable investors, while the offshore feeder caters to non-U.S. investors and U.S. tax-exempt entities, such as pension funds and endowments. Each feeder operates as a separate legal entity but does not make independent investment decisions.

"The master fund is the central investment vehicle that executes the primary investment strategy. It receives capital from one or more feeder funds and directly invests in a portfolio of securities." – MyFinanceProcess [4]

The master fund holds all the portfolio assets – whether these are digital tokens, venture equity, or traditional securities – and manages relationships with brokers, custodians, and clearing houses. By centralizing these activities, fund managers only need to negotiate counterparty agreements once, avoiding the complexity of separate agreements for each investor group. This setup ensures a streamlined process for managing investments. Let’s dive into how capital flows through this system.

How Capital Flows Through the System

Capital flows seamlessly from investors to the master fund through the feeders. Investors commit funds to a feeder, which then channels all capital into the master fund in exchange for proportional ownership. For example, if a domestic feeder contributes $10 million and an offshore feeder contributes $15 million, the domestic feeder owns 40% of the master fund, while the offshore feeder owns 60%. The master fund pools this capital to execute a single, unified trading strategy.

This centralized system not only simplifies trading but also eases regulatory compliance. Profits and losses flow back through the same channels. The master fund allocates income, gains, and expenses to each feeder based on its ownership percentage, and the feeders, in turn, distribute returns to their respective investors. For instance, if the master fund achieves a 20% return, both feeders reflect that return proportionately in their distributions.

Regulatory Requirements

Master-feeder structures must navigate a variety of regulatory frameworks. The master fund typically avoids registration as a regulated investment company by relying on exemptions under the Investment Company Act of 1940, such as Section 3(c)(7) or Section 3(c)(1). Section 3(c)(7) requires all investors to qualify as "Qualified Purchasers", while Section 3(c)(1) limits the fund to no more than 100 beneficial owners [7].

Compliance with ERISA becomes a key concern when U.S. retirement plans invest through a feeder fund. If retirement plan investments make up 25% or more of a feeder fund’s total capital, the fund must implement specific measures to meet Department of Labor regulations [8]. Additionally, the master fund typically makes a "check-the-box" election for U.S. tax purposes, allowing it to be treated as a partnership. This step avoids an extra layer of corporate taxation on gains. Setting up a master-feeder structure generally costs between $15,000 and $50,000 [8].

sbb-itb-c5fef17

Benefits of Master-Feeder Structures

Single Portfolio Management

By managing a single portfolio at the master fund level, fund managers eliminate the need to replicate trades across different investor groups. This means investment decisions are made once and applied to the entire pool of capital, cutting down on redundant tasks like rebalancing trades [8].

"The master-feeder model solves this by creating separate entry points… the general partner runs one portfolio and one strategy regardless of how many feeders sit above it." – PipelineRoad [5]

This centralized approach also simplifies risk oversight. Fund administrators manage the portfolio-level records at the master fund, while keeping separate investor-level records and tax reporting (such as K-1s) for each feeder [5]. These efficiencies not only streamline operations but also reduce costs.

Cost Savings from Scale

Pooling capital through a master-feeder structure creates economies of scale, which help reduce costs for individual investors. Larger trade volumes allow fund managers to negotiate better rates for brokerage and transaction fees [8]. Simply put, combining assets is less expensive than managing multiple smaller funds.

"By joining together, the fund managers can take advantage of economies of scale, lowering trading costs and simplifying management." – Fund Launch Team [8]

Administrative costs also shrink. Centralized accounting, tax preparation, and auditing are handled at the master fund level, avoiding duplicate expenses across multiple entities. For context, annual fund administration typically costs between $15,000 and $40,000, while audit fees range from $15,000 to $30,000 [9]. These savings align with the operational efficiencies achieved through centralized trade execution.

Easier Trade Execution

Master-feeder structures streamline relationships with brokers, custodians, and clearing houses. Instead of negotiating separate agreements for each investor group, fund managers work under a single legal agreement at the master fund level [8].

"A single legal agreement with counterparties at the master fund level reduces legal and administrative burdens." – Fund Launch Team [8]

For globally operating Web3 funds, this setup integrates seamlessly with International Central Securities Depositories (ICSDs) like Euroclear and Clearstream. These platforms support straight-through processing for subscriptions and redemptions, cutting down on paperwork and enabling electronic, multi-currency settlements [3]. Additionally, the larger asset pool improves access to leverage and simplifies the execution of complex strategies, including derivatives and hedging [3].

Hedge Fund Master-Feeder Structures – How Do They Work?

Feeder Funds vs Master Funds: Main Differences

Building on the structure and benefits discussed earlier, let’s dive into how feeder and master funds differ in their roles and operations.

What Feeder Funds Do

Feeder funds act as the entry point for investors, channeling their capital into the master fund. They don’t hold any direct assets themselves – just an ownership stake in the master fund. Each feeder fund is tailored to meet the needs of specific investor groups, such as U.S. taxable individuals, U.S. tax-exempt entities, or non-U.S. investors.

This setup allows fund managers to navigate varying tax and regulatory requirements without disrupting the overall investment strategy. For example, a Cayman Islands-based offshore feeder can help non-U.S. investors avoid U.S. tax filing obligations while enabling U.S. tax-exempt entities to avoid Unrelated Business Taxable Income (UBTI). However, feeder funds do come with their own administrative fees, which can affect their net performance when compared to the master fund.

"A feeder fund’s primary function is to provide a way for smaller investors to access the master fund’s investment opportunities."

- Anne Wiegand, Writer, CGAA

What Master Funds Do

The master fund is where the core action happens – portfolio management, trading, and asset holding all take place here. It makes centralized investment decisions and distributes returns to the feeder funds based on their share of the capital.

"The master fund functions as the central hub where all portfolio management and trading activities occur. It is the sole repository for the pooled assets."

- LegalClarity Team

The master fund holds the actual investments – whether they’re equities, derivatives, or tokens. It also handles negotiations with brokers, custodians, and clearing houses. This centralized approach simplifies operations by maintaining a single set of legal agreements, instead of duplicating them across multiple investor groups.

Side-by-Side Comparison

Here’s a quick breakdown of the main differences between feeder and master funds:

| Feature | Feeder Fund | Master Fund |

|---|---|---|

| Primary Role | Aggregates capital and interfaces with investors | Manages the portfolio and executes trades |

| Asset Holding | Owns shares/units in the master fund | Holds the actual investments |

| Investor Type | Targets specific investor groups | Combines capital from all feeder funds |

| Tax Status | Adjusted for investor jurisdiction (e.g., LLC, LP, Corp) | Generally tax-neutral (e.g., partnership) |

| Control | Passive; relies on master fund decisions | Full control over investment strategy |

| Performance | Reflects master fund performance minus feeder fees | Sets the performance for all feeders |

These distinctions are crucial for choosing the right fund structure to complement your Web3 investment goals. By understanding how feeder and master funds operate, investors can better align their strategies with the appropriate framework.

Selecting the Right Fund Structure for Web3 Investments

When to Use Master-Feeder Structures

Master-feeder structures are well-suited for liquid Web3 strategies, particularly those involving frequent trading of tokens or digital assets. By centralizing trades, this setup minimizes duplication and reduces transaction costs through economies of scale.

This structure is especially useful when raising capital from a diverse investor base. For example, if your limited partners (LPs) include non-U.S. investors, U.S. tax-exempt entities (like pension funds or university endowments), and U.S. taxable individuals, separate feeders can address their unique needs. As PipelineRoad explains:

"The master-feeder model solves this by creating separate entry points… allowing the manager to run a single investment strategy while accommodating diverse LP needs" [5].

However, for illiquid Web3 venture capital strategies – such as early-stage token projects or SAFTs (Simple Agreements for Future Tokens) – a parallel fund structure may be a better fit. This approach allows for direct asset ownership, avoiding the complexities of a master-feeder setup [5].

These distinctions pave the way for institutional-specific considerations, which we’ll explore next.

What Institutional Investors Should Consider

For institutional investors, tax efficiency is a top priority. U.S. tax-exempt entities, such as pension plans and endowments, typically invest through offshore feeder funds – commonly based in the Cayman Islands – to avoid generating Unrelated Business Taxable Income (UBTI) [7][5].

Regulatory compliance is another key concern. Many institutional funds operate under Section 3(c)(7), which permits up to 2,000 beneficial owners, as long as all are "Qualified Purchasers." This means individuals must have at least $5 million in investments, while institutions need $25 million or more [7][9]. If your fund is likely to exceed 100 LPs, structuring under Section 3(c)(7) from the outset is crucial. As VC Beast notes:

"If you ever plan to have 100+ LPs, you need to structure as 3(c)(7) from the start. You can’t convert later without restructuring the fund" [9].

Institutional investors should also plan for setup and operational costs, which typically range from $50,000 to $100,000 in the first year. These expenses cover legal fees, fund administration, audits, and tax preparation [9][8]. Ensuring the fund size justifies these costs is essential.

A case from 2018 highlights the importance of legal separation. The Grand Court of the Cayman Islands ruled against the Asia Dragon feeder fund in its dispute with the Ardon Maroon Asia Master Fund because it failed to provide formal written notice of redemption before both were liquidated. This serves as a reminder to maintain clear, formal communication between feeder and master entities [1][10].

Careful tax and regulatory planning is essential to ensure master-feeder structures align with the operational goals of Web3 investments.

What Individual Investors Should Consider

While institutional investors focus on tax and regulatory strategies, individual investors face a different set of challenges.

Individual investors typically access master-feeder structures through feeder funds. These funds pool capital to meet the master fund’s thresholds, which often range from $1 million to $10 million. Feeder fund minimums are usually between $50,000 and $100,000 [2][8].

Before investing, confirm your eligibility. Most feeder funds require "Accredited Investor" status, while some master funds demand "Qualified Purchaser" status, which generally requires $5 million or more in investments [9]. This distinction determines which funds are accessible to you.

Another key consideration is fee layering. The master fund usually charges a standard management fee – around 2% of committed capital during the investment period, which later drops to 1%-1.5% of invested capital [9]. Feeder funds, however, often add their own administrative fees for services like audits and fund administration [5]. Always review offering documents to fully understand the fee structure.

For non-U.S. investors, using an offshore feeder fund can help avoid U.S. tax filing obligations [7]. However, be aware that offshore feeders may face a 30% withholding tax on U.S. dividends, which can affect returns if the fund holds U.S. equities [1].

These considerations highlight the importance of evaluating fees, eligibility, and tax implications before committing to a master-feeder structure.

Conclusion

Feeder and master funds work together as parts of a cohesive investment system. Feeder funds act as gateways tailored to specific investor groups, while the master fund functions as the central platform for portfolio management and trading. This setup plays a crucial role in structuring investments in the Web3 space.

When deciding on a fund structure, it’s important to consider the makeup of your investor base. The right structure depends on both your investors’ profiles and regulatory requirements. For instance, U.S. taxable investors often use domestic Delaware LP feeders, while non-U.S. and tax-exempt investors typically require offshore feeders to avoid UBTI and U.S. tax filing obligations [6]. As VC Beast cautions:

"Choosing the wrong fund structure costs you money, limits your LPs, and creates legal headaches that last for years" [6].

For Web3 fund managers, timing is everything when it comes to implementing a master-feeder structure. If your investor pool includes a mix of U.S. taxable, tax-exempt, and international investors, this structure becomes essential. On the other hand, if you’re raising funds solely from U.S. taxable individuals, a simpler Delaware LP structure may be more cost-effective, potentially saving $15,000–$25,000 in upfront expenses [6].

Both individual and institutional investors must align their choices with their unique goals. Individual investors should confirm eligibility and fee structures, while institutional investors should focus on tax efficiency and compliance. Strategically integrating feeder and master funds can enhance operational efficiency and minimize costs. Ultimately, the best structure is one that aligns seamlessly with your investment strategy, investor base, and operational objectives in the Web3 ecosystem.

FAQs

Do I need a feeder fund to invest in a master fund?

Feeder funds are not mandatory for investing in a master fund. While they are commonly used to pool capital from specific groups of investors and then allocate it to a master fund, institutional investors can often invest directly in the master fund. Feeder funds primarily exist to address differences in regulatory, tax, or reporting requirements among investors and to streamline operations for cost efficiency. However, they serve as a convenience rather than a necessity for accessing master funds.

How do I know if I’m an Accredited Investor or a Qualified Purchaser?

To qualify as an Accredited Investor, individuals need to meet certain financial benchmarks. This includes having a net worth exceeding $1 million (excluding the value of their primary residence) or an annual income of more than $200,000 – or $300,000 when combined with a spouse – over the past two years.

On the other hand, a Qualified Purchaser is someone with at least $5 million in investments. Understanding where you stand is crucial, as it determines your access to specific investment opportunities and the level of investor protections you may receive.

What additional fees can a feeder fund charge beyond the master fund?

Feeder funds often tack on extra charges in addition to the fees already imposed by the master fund. These can include management fees, performance fees, and administrative fees. The exact amount of these additional costs depends on the specific structure and objectives of the feeder fund.