When it comes to SAFT (Simple Agreement for Future Tokens) vesting, taxes can get complicated fast. Each time tokens vest, it’s a taxable event, and ignoring IRS rules can lead to significant penalties. Here’s what you need to know upfront:

- Taxable Events: Every vesting milestone is taxed as ordinary income based on the token’s fair market value (FMV).

- 83(b) Election: Filing this election within 30 days of the grant date can reduce taxes by locking in the token’s value at the grant date.

- Tax Withholding: Taxes must be paid in USD, requiring strategies like "sell-to-cover" or "net settlement."

- Documentation: Keep detailed records of token valuations, vesting schedules, and tax filings to avoid audit risks.

Failing to comply with these rules can lead to steep tax bills or penalties. Let’s break down the key steps to stay compliant and avoid costly mistakes.

SAFT Vesting and Tax Implications

When you receive tokens through a SAFT (Simple Agreement for Future Tokens), the IRS treats them as property rather than currency, as outlined in IRS Notice 2014‑21 [3][4]. Each time tokens vest, it creates a taxable event. The taxable amount is calculated based on the fair market value of the tokens at the time of vesting, and this income is taxed at ordinary income rates, which can go as high as 37% [3][4][8].

Unlike traditional equity, where taxes are deferred until a sale, SAFT-related taxes are due as tokens vest. This can lead to unexpectedly high tax bills, especially if the token value increases between the grant and vesting dates. Below, we’ll explore the key tax triggers and strategies to manage these liabilities.

Tax Triggers for SAFT Vesting

The main tax trigger occurs at each vesting milestone. For instance, if your SAFT agreement includes monthly vesting over three years, each month’s unlock is treated as taxable income [3]. To determine the taxable amount, you must calculate the tokens’ fair market value at each vesting event using appropriate valuation methods [3][4]. Even if the tokens aren’t immediately sellable, their value must still be reported as ordinary income [4].

A second tax trigger arises when you sell or dispose of the tokens. At this point, capital gains tax applies to any increase in value from the vesting date to the sale date [8][4]. If you hold the tokens for over a year after they vest, you may qualify for lower long-term capital gains tax rates of 15% or 20%, compared to the higher ordinary income rates [8].

83(b) Election Filing

The 83(b) election offers a way to shift the taxable event from each vesting date to the grant date. You have 30 calendar days from the grant date to file this election with the IRS – no extensions or exceptions are allowed [8][9][11]. By making this election, you pay ordinary income tax based on the tokens’ fair market value at the time of the grant [8][12].

"The 83(b) election allows you to pay taxes on your tokens when they’re granted, not when they vest. That one decision can dramatically lower your total tax bill." – Toku [14]

For early-stage projects where token values are minimal at the time of grant, this strategy can lead to significant tax savings. Any future appreciation is then taxed at the lower long-term capital gains rates, potentially saving as much as 17 to 30 percentage points in taxes [11][12]. However, if the tokens are forfeited or lose value, the taxes paid upfront under the 83(b) election are non-refundable [11][13][14].

Starting in July 2025, the IRS will accept online 83(b) filings through Form 15620. Alternatively, you can file by paper using USPS Certified Mail with Return Receipt Requested to ensure proof of timely delivery [12][14].

sbb-itb-c5fef17

Pre-Vesting Compliance Checklist

Taking care of these steps before vesting can help you avoid unexpected tax surprises. Proper preparation ensures smoother tax withholding and makes audit processes much easier down the line. Think of it as laying the groundwork for accurate tax calculations and hassle-free vesting.

Review SAFT Agreement Terms

Start by reviewing your SAFT agreement carefully. This document outlines key details that directly influence your tax responsibilities. Pay close attention to the trigger event – such as "Network Launch" or "Functional Utility" – as it marks the beginning of your 30-day window for filing the 83(b) election. Also, double-check the vesting schedule, since each unlock could result in taxable events.

Another critical detail is the forfeiture clause. Ensure the agreement includes language for repurchase at the original price, which is an IRS requirement for making an 83(b) election. Additionally, confirm whether your agreement is categorized as a Restricted Token Award (RTA) – which qualifies for the 83(b) election – or a Restricted Token Unit (RTU), which doesn’t, as it only represents a promise of future token delivery.

Finally, verify the valuation of your tokens to proceed with the next steps.

Conduct 409A Valuation

A 409A valuation is essential for determining the fair market value of your tokens. This valuation is critical for filing the 83(b) election and for defending against potential audits. Make sure the appraisal is conducted by a qualified professional and is updated annually, or whenever significant events occur, like a funding round or a major revenue change (e.g., a 25% increase).

Once the valuation is complete, the next step is to educate token recipients about their tax options.

Provide Tax Election Guidance to Recipients

Recipients, whether they’re team members or advisors, need clear guidance on filing the 83(b) election. They must file this election within 30 days of the grant date using Form 15620. This can be done online or via USPS Certified Mail. Advise them to prepare funds for the upfront tax payment, submit a signed copy of the election to HR or payroll, and include another copy with their tax return.

"The 83(b) election represents a powerful tax planning strategy for founders and employees receiving vesting tokens. When used appropriately, it can result in substantial tax savings and simplified compliance." – Mo Yang, Founder and Managing Partner, Convoy Finance [8]

Highlight the potential savings: for a standard grant, making the 83(b) election can save over $46,000 in taxes. In cases of rapid growth, the savings can exceed $2.1 million [12]. Sharing these figures can help recipients understand the financial benefits and importance of acting promptly.

Vesting Event Tax Withholding Checklist

When your tokens vest, each vesting event triggers a taxable obligation. The tax owed is determined by the fair market value (FMV) of the tokens at the time they vest [3][4].

Calculate Taxable Income at Vesting

To start, calculate the FMV of your tokens at the exact moment they vest. For liquid tokens traded on exchanges, use the spot price at the time of transfer or a 24-hour volume-weighted average price (VWAP) to account for price fluctuations [3][4]. For illiquid tokens not listed on exchanges, you’ll need a qualified appraisal or a 409A-style valuation based on market comparables [3][4].

Once you have the FMV, multiply it by the number of vested tokens to determine your taxable income. This amount typically falls into the 32% to 37% federal tax bracket [15]. Don’t forget to include state taxes, as states like California, Maryland, and New York have their own supplemental income withholding rates. Keep a detailed log of each vesting event, noting the date, token quantity, and FMV source (e.g., exchange screenshot or appraisal report) [3][15].

After calculating the taxable income, you’ll need to choose a method to handle the associated tax liabilities.

Apply Tax Withholding Methods

Taxes must be paid in USD. The federal supplemental withholding rate is 22% for amounts under $1 million and 37% for amounts over $1 million [16]. Select a withholding method that ensures compliance with IRS rules while generating the required USD for tax payments:

- Net Settlement: Your employer withholds a portion of the tokens to cover taxes and pays the tax liability on your behalf. This avoids selling tokens on the market but requires your employer to have sufficient fiat liquidity [4][15].

- Sell-to-Cover: A portion of your vested tokens is sold on the market to generate cash for taxes. This method ensures liquidity but may affect token prices if market liquidity is low [4][15].

- Cash-to-Cover: Taxes are deducted from your cash salary, or you provide fiat funds directly. While simple for payroll teams, this can create a cash flow challenge if your salary is low compared to the token value [4][15].

"The fair market value of virtual currency paid as wages, measured in U.S. dollars at the date of receipt, is subject to Federal income tax withholding." – IRS Virtual Currency FAQ [16]

Document Ownership and Control

Once taxes are paid, make sure your token ownership records are accurate and complete to avoid issues during audits. Clearly document beneficial ownership and ensure the timing of control transfer is well-defined, as this determines when taxes are triggered. Use smart contracts or escrow arrangements to specify when you gain control of tokens [2][1].

Maintain detailed logs for each unlock event, including timestamps, wallet addresses, token amounts, and reference smart contracts [2][1]. For compliance, link wallet addresses to verified identities through KYC (Know Your Customer) procedures. If tokens operate across multiple networks, consolidate cross-chain transactions into a single cap table for streamlined reporting [2][1]. Finally, document your valuation methodology, especially for illiquid tokens, in case your FMV calculations are challenged [4].

Post-Vesting Compliance and Audit Preparation

Once tokens vest and taxes are paid, the work doesn’t stop there. Staying on top of compliance and being prepared for audits is crucial to avoid regulatory headaches. The IRS can review up to three years of tax returns – or even six years if they suspect significant underreporting [18]. Keeping your records well-organized can cut the length of an IRS audit by 40% to 60% [18].

Maintain Documentation

Creating a central hub for all SAFT vesting records is a smart move. This should include 409A valuation reports that detail the methodology used – whether it’s the Market, Income, or Asset Approach – and the exact FMV (Fair Market Value) for each vesting event [3][17]. Also, keep copies of all relevant tax forms, like Form W-2 for employees, Form 1099-MISC or 1099-DA for contractors, and any 83(b) election filings [17][2][4].

Don’t forget about on-chain records. Save transaction hashes, wallet addresses, and timestamped unlock logs [2][1]. For each vesting event, take snapshots of exchange data (like VWAP or closing prices) [3]. You’ll also need KYC/AML documentation and "Know Your Transaction" (KYT) reports to confirm wallet ownership and compliance [10][2]. If you’re working across multiple blockchain networks, consolidate all cross-chain activity into a single cap table for easier reporting [2][1].

Having these records isn’t just about audits – it’s also essential for accurate revenue tracking.

Monitor Revenue Recognition Rules

Proper documentation is critical for adhering to IRS revenue recognition rules. Under IRS Notice 2014-21, tokens are treated as property, so general tax rules for property transactions apply [6][3]. For example, staking rewards, airdrops, and hard forks are considered ordinary income as soon as you have "dominion and control" over the tokens [7][6]. After vesting, the FMV becomes your cost basis, with any later price changes treated as capital gains or losses [6][3].

If your company raised funds through SAFTs, be aware that these proceeds might be taxable income, depending on whether the agreement is classified as a pre-sale of services or digital goods rather than a capital contribution [19]. Document key events like new funding rounds or token generation events, as these could trigger revaluations [17]. Employees who fail to comply with 409A rules face serious consequences, including immediate taxation, a 20% federal tax penalty, and steep interest charges. In some cases, the total tax hit can exceed 60% of the deferred amount, especially when state penalties (like California’s 5% surcharge) are added [17].

Review Section 409A Compliance

Just like pre-vesting tax preparations, regular reviews of Section 409A compliance are essential to avoid unexpected penalties. Section 409A governs deferred compensation, and SAFT vesting schedules can sometimes fall under its scope if tokens are treated as deferred compensation. Double-check that your SAFT terms don’t unintentionally create a deferral arrangement that violates these rules. Make sure every valuation report is backed by board approvals, and establish clear policies for identifying "material events" that require revaluations [17].

To stay ahead, perform monthly reconciliations of financial accounts to catch any untracked deposits that could lead to unexpected taxes [18]. If you’re ever audited, don’t engage directly with the IRS – let a CPA or tax attorney handle communication and documentation [18]. With approximately one-third of the global crypto workforce based in the United States, compliance is non-negotiable under the IRS’s watchful eye [4].

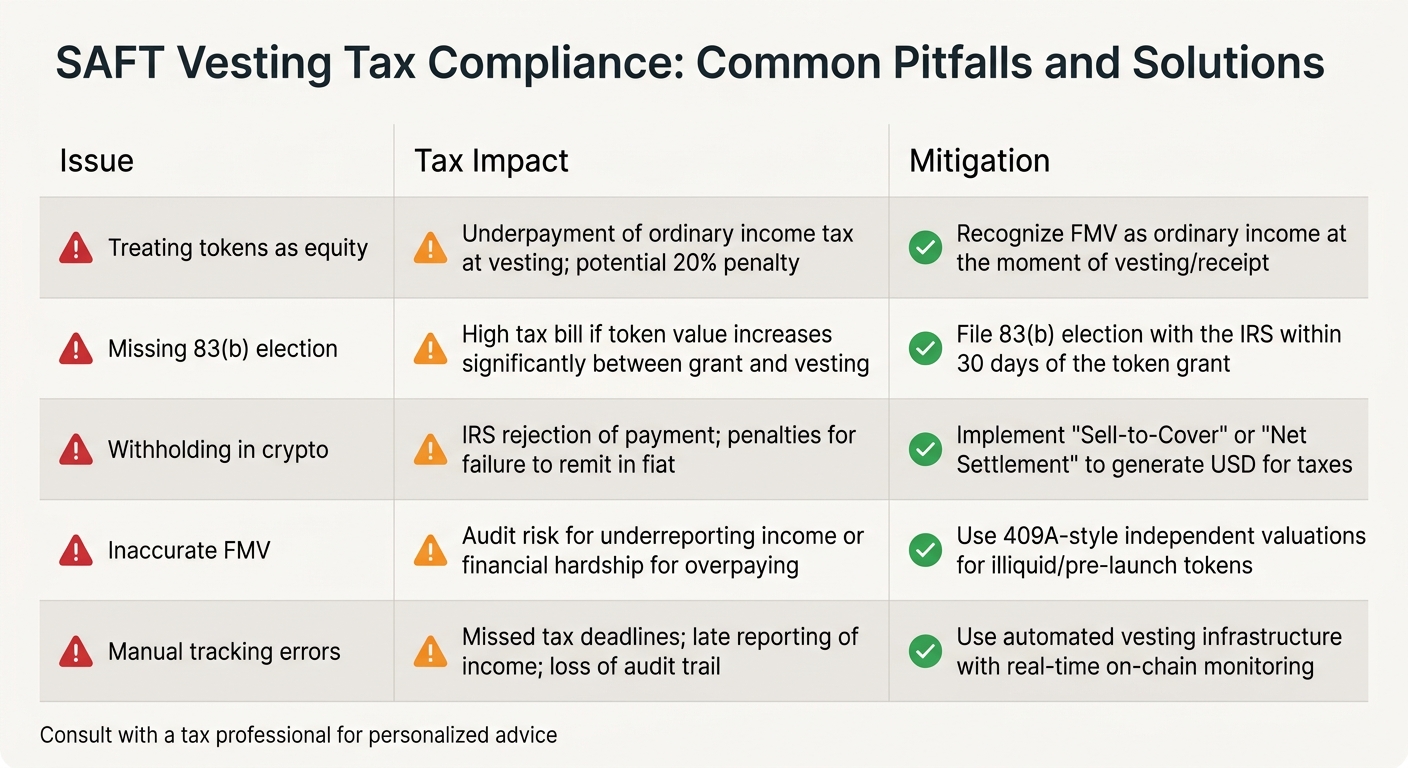

Common Pitfalls and How to Avoid Them

SAFT Vesting Tax Compliance: Common Pitfalls and Solutions

Navigating SAFT vesting tax compliance can be tricky, and there are several common missteps teams often encounter. One of the biggest mistakes is treating tokens like traditional equity. Many assume taxes are only relevant when tokens are sold, but this misreads IRS rules. According to IRS Notice 2014-21, tokens are considered property. This means recipients owe ordinary income tax on the fair market value (FMV) at the moment tokens vest – not when they’re eventually sold [4].

Another major issue is missing the 83(b) election deadline, which can lead to steep tax bills. For example, if a token granted at $0.10 appreciates to $10 by the time it vests, failing to file the election means being taxed on the full vested value. This could have been avoided with timely filing. Similarly, valuation errors can cause problems. Without a "reasonable and defensible" FMV for illiquid or pre-launch tokens (as discussed in the "Conduct 409A Valuation" section), you risk underreporting income – leading to penalties – or overpaying taxes unnecessarily [4].

Handling withholding in cryptocurrency is another hurdle. Since the IRS requires taxes to be paid in U.S. dollars, teams need a strategy to convert tokens into fiat currency upon vesting. A sell-to-cover or net settlement approach can help ensure compliance [4]. Lastly, manual record-keeping can lead to costly errors. Using spreadsheets to track multi-chain vesting often results in missed cliff dates, incorrect distributions, and what experts call "operational black holes" [2][1]. The consequences? The IRS may impose a 20% penalty on under-reported digital asset income, along with interest and potential fraud penalties [2].

The table below outlines these common pitfalls and suggests practical solutions to avoid them.

Comparison Table: Common Pitfalls and Solutions

| Issue | Tax Impact | Mitigation |

|---|---|---|

| Treating tokens as equity | Underpayment of ordinary income tax at vesting; potential 20% penalty. | Recognize FMV as ordinary income at the moment of vesting/receipt. |

| Missing 83(b) election | High tax bill if token value increases significantly between grant and vesting. | File 83(b) election with the IRS within 30 days of the token grant. |

| Withholding in crypto | IRS rejection of payment; penalties for failure to remit in fiat. | Implement "Sell-to-Cover" or "Net Settlement" to generate USD for taxes. |

| Inaccurate FMV | Audit risk for underreporting income or financial hardship for overpaying. | Use 409A-style independent valuations for illiquid/pre-launch tokens. |

| Manual tracking errors | Missed tax deadlines; late reporting of income; loss of audit trail. | Use automated vesting infrastructure with real-time on-chain monitoring. |

Conclusion and Key Takeaways

When it comes to handling SAFT vesting taxes, proactive management is your best strategy. Here are the essential points to keep in mind:

- File your 83(b) election promptly: You have only 30 days from the grant date to submit this form via certified mail. The IRS does not allow extensions for this deadline[5][12]. Filing on time locks in the valuation at the grant date, ensuring any future gains are taxed at the lower long-term capital gains rates (15–20%) instead of the higher ordinary income rates, which can go up to 37%[12].

- Document fair market value meticulously: For every vesting event, maintain clear records of the fair market value. Use sources like exchange prices, decentralized exchange data, or qualified appraisals. This documentation is crucial in case of an audit.

- Understand taxation on vesting events: Each vesting unlock is treated as its own taxable event. According to IRS Notice 2014-21, you owe ordinary income tax based on the fair market value of the tokens at the time they vest – even if you don’t sell them[3].

"Virtual currency is treated as property for U.S. federal tax purposes. General tax principles applicable to property transactions apply to transactions using virtual currency."

– IRS Notice 2014-21[3]

- Plan for tax withholding: Since the IRS requires taxes to be paid in U.S. dollars, consider a sell-to-cover or net settlement strategy to cover these obligations[20].

- Leverage automation: Automating your vesting infrastructure can help you avoid errors and streamline tracking, especially if dealing with multiple blockchain networks[2].

The IRS is ramping up its focus on digital assets, with over $3.1 billion allocated for monitoring these transactions[6]. Additionally, brokers are set to issue Form 1099-DA starting in the 2025 tax year[2]. By staying informed and organized, you can navigate your SAFT vesting tax responsibilities with confidence.

FAQs

How do I determine FMV for illiquid tokens at vesting?

To figure out the fair market value (FMV) of illiquid tokens at the time of vesting, you can rely on IRS guidelines, which classify tokens as property. This means you’ll need to use a reasonable valuation method. Options include hiring a third-party appraiser or applying a valuation model that factors in the token’s utility, future potential, and similar assets in the market.

Keep in mind, every vesting event is considered taxable. The FMV of the tokens at the time they vest will directly impact your income tax liability.

Can I file an 83(b) election for my SAFT tokens?

Yes, you can file an 83(b) election for your SAFT tokens within 30 days of receiving them. This election allows you to pay taxes based on their current value, which could help lower your future tax burden by taking advantage of the lower capital gains rates on any increase in their value over time.

What if my vested tokens aren’t sellable but I still owe tax?

If your vested tokens can’t be sold, you might still have to pay taxes based on their value at the time they vest. To handle this properly, it’s a good idea to consult a tax professional. They can help you explore strategies, like filing an 83(b) election, to better manage your tax responsibilities.