Pre-IPO shares can offer big rewards, but they come with higher risks. Many startups fail, shares are often illiquid, and fraud can occur. To make informed decisions, follow these five steps:

- Verify Brokers: Ensure your broker is registered with FINRA or the SEC. Avoid unregistered agents or high-pressure sales tactics.

- Analyze Financials: Check revenue growth, cash runway, and key metrics like ARR and gross margins. Look for sustainable business models and market potential.

- Review Legal Terms: Understand share classes, liquidation preferences, and transfer restrictions. Legal documents like the Cap Table and PPM are key.

- Assess Valuation: Compare the price of shares with market benchmarks and calculate risks like dilution or waterfall preferences.

- Plan for Liquidity: Pre-IPO shares are illiquid for years. Ensure they align with your investment goals and portfolio strategy.

Key takeaway: Investing in pre-IPO shares requires thorough research. Focus on transparency, financial health, and liquidity risks to avoid costly mistakes.

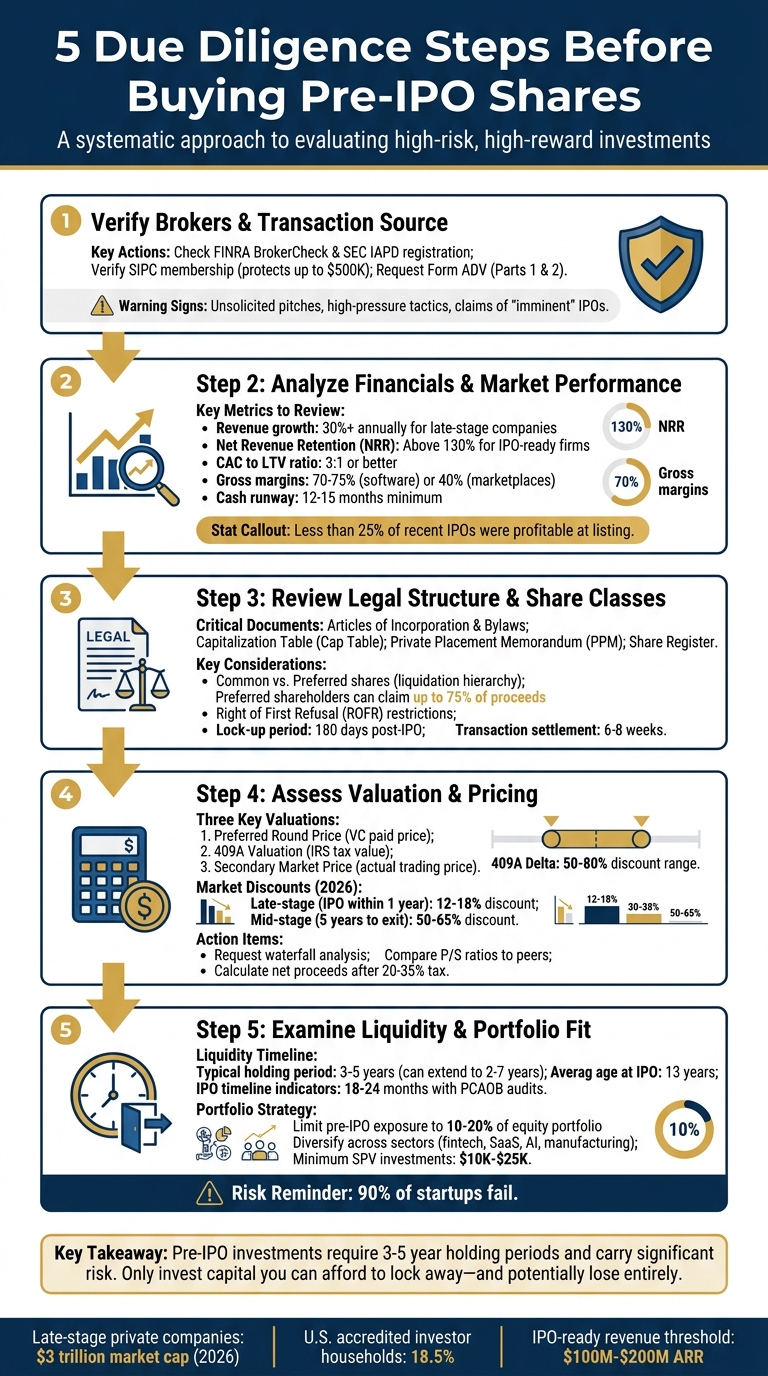

5 Essential Due Diligence Steps Before Buying Pre-IPO Shares

1. Verify the Transaction Source and Broker Legitimacy

Fraud and Counterparty Risk Prevention

Before diving into pre-IPO investments, it’s essential to confirm the legitimacy of your transaction source. Cases like the SEC’s charges against a group in New Jersey and New York highlight the dangers - this particular scheme defrauded over 4,000 investors worldwide, raking in more than $528 million. The group used unregistered agents and hid hefty markups, pocketing $88 million in the process[7].

Start your due diligence by checking the broker’s credentials. Tools like FINRA’s BrokerCheck and the SEC’s IAPD can help verify registration and uncover any disciplinary history[7]. Additionally, ensure the brokerage firm is a member of the Securities Investor Protection Corporation (SIPC), which offers protection up to $500,000 (including $250,000 for cash) if the firm fails[7]. Always make payments directly to the member firm - never to an individual broker[7]. These steps are critical for reducing counterparty risks.

Stay alert for warning signs like unsolicited pitches, high-pressure sales tactics, claims of “imminent” IPOs, or hesitation to provide written documentation[6][7]. A trustworthy advisor will willingly share Form ADV (Parts 1 and 2), which outlines their services, fees, and any disciplinary history[7]. If someone avoids your questions or seems in a rush, it’s a clear signal to walk away.

“If you can’t get straight answers or the individual seems rushed or otherwise unwilling to provide you with full and clear information, go elsewhere.” – Investopedia[7]

A quick online search of the broker or firm can also uncover valuable insights, such as news reports, regulatory actions, or complaints from other investors[7]. For example, platforms like EquityZen, which has facilitated over 41,000 transactions across more than 450 late-stage private companies, operate as registered broker-dealers under FINRA and SIPC oversight[8]. Such regulatory compliance is non-negotiable when evaluating potential brokers.

sbb-itb-c5fef17

2. Conduct Financial and Market Analysis

Financial and Market Performance Evaluation

Once you’ve verified your broker, the next step is to dig into the company’s financial health and market standing. This helps you distinguish between businesses built for long-term success and those thriving on hype. Start by reviewing revenue trends - look for consistent annual growth of 30% or more in late-stage companies[11]. For SaaS businesses, pay close attention to metrics like Annual Recurring Revenue (ARR) and Net Revenue Retention (NRR). Companies gearing up for an IPO often report NRR above 130%, which reflects strong customer loyalty and growth within the existing customer base[1].

Another key area is unit economics. A solid Customer Acquisition Cost (CAC) to Lifetime Value (LTV) ratio should be 3:1 or better[11]. If CAC is dropping while payback periods are improving, it’s usually a sign of sustainable growth[1]. Don’t overlook gross margins either - high-growth software companies often maintain margins above 70% to 75%, while marketplaces typically hover around 40%[11][1]. These figures help you gauge whether the business model can scale effectively and profitably.

Cash management is just as important. A company should have at least 12–15 months of operational cash, which you can assess by calculating its burn rate[3]. If the runway is under 12 months and there’s no confirmed funding, the risk of dilution rises significantly[3]. Keep in mind that less than 25% of recent IPOs were profitable at the time of listing[12], so understanding how a company plans to improve margins or achieve profitability is critical.

“Revenue growth alone is never enough. Sustainability almost always wins over hype.” – Supremus Angel[3]

Diversification of revenue sources is another factor to evaluate. Ideally, the top 10 customers should contribute less than 30% of total revenue[11]. Heavy reliance on a single client poses a significant risk. Additionally, assess the Total Addressable Market (TAM) and the company’s competitive edge. Is the sector growing structurally? Does the company have technological advantages or barriers to entry that protect its position?

For example, in April 2026, Anthropic was valued at nearly $1 trillion on the Forge Global secondary marketplace. CEO Kelly Rodriques highlighted that this valuation was driven by eager buyers, despite much lower valuations in recent primary funding rounds[11]. This illustrates why independent market analysis is crucial - headline valuations can be misleading.

3. Review Legal Structure, Share Class, and Transfer Restrictions

Legal and Structural Alignment with Investment Goals

Understanding the legal structure of a company is just as important as analyzing its financials when it comes to managing pre-IPO risks. Once you’ve evaluated the numbers, it’s time to clarify what exactly you’re purchasing from a legal perspective. The type of share class you acquire directly impacts your rights, payout priority, and flexibility when exiting the investment. For example, most secondary buyers end up with common shares, which rank last in the liquidation hierarchy. This means that venture capital firms holding preferred shares are paid first during an acquisition or IPO. In some cases, these preference structures can take up as much as 75% of the proceeds, leaving common shareholders with far less than the headline valuation might suggest[4].

To avoid surprises, start by reviewing the company’s Articles of Incorporation and Bylaws. These documents will outline the authorized share classes and governance rules[14][15]. Next, examine the Capitalization Table (Cap Table) and Share Register to verify ownership percentages and ensure there are no discrepancies[14][15]. Any inconsistencies in these records could put your investment at risk. The Private Placement Memorandum (PPM) is another critical document, as it details the investment terms, business risks, and specifics about the share class you’re purchasing[16]. Pay close attention to the “Use of Proceeds” section - look for detailed allocations rather than vague terms like “general working capital”[16]. Once the legal framework is clear, it’s time to consider how transfer restrictions could affect your ability to liquidate your shares.

“Missing IP assignments kill more deals than any other single issue, particularly for technology companies.” – Laura Ryan, Barrister and Chartered Accountant[14]

Transfer Restrictions and Liquidity Challenges

Transfer restrictions can significantly impact your liquidity. Many private companies enforce a Right of First Refusal (ROFR), which gives the company or existing investors the option to purchase your shares at the agreed price before you can sell them to a third party[4]. These restrictions, combined with the SEC Rule 144 holding period of six months to one year, can delay your ability to resell shares[4][18]. Additionally, post-IPO, you’ll likely face a lock-up period of 180 days, during which selling is prohibited[4].

To better understand potential challenges, investigate whether the company has a history of exercising or waiving ROFR through secondary market data[4]. Also, confirm that the company has secured intellectual property (IP) assignment agreements from all founders, employees, and contractors. Missing IP agreements are a leading cause of deal failures, especially for tech companies[14]. Review any Buy-Sell Agreements or Shareholder Control Agreements that might impose further restrictions on your ability to exit[9][15]. Keep in mind that pre-IPO transactions typically take 6 to 8 weeks to settle, compared to the single-day settlement process for public stocks[4].

If you’re investing through a Special Purpose Vehicle (SPV), it’s important to understand how this structure could affect your investment. SPVs with multiple layers between the investor and the actual equity can lead to higher fees and less transparency[17]. Investors in these vehicles lack direct financial or voting rights and rely entirely on the SPV manager for updates[4]. Costs for setting up an SPV range from $10,000 to $20,000, with transaction fees of 2% to 5% and carried interest of 10% to 20% of profits[4]. For smaller investments under $100,000, SPVs can be a cost-effective option since expenses are shared, but this comes at the expense of access to detailed information[4].

4. Check Valuation Metrics and Pricing

Accurate and Disciplined Valuation Assessment

Once you’ve completed your financial and legal analysis, the next step is to dig into valuation metrics and pricing assumptions. When it comes to pre-IPO pricing, there are three key valuations to consider: the Preferred Round Price (what venture capital firms paid), the 409A Valuation (an IRS-compliant tax value), and the Secondary Market Price (the price at which common shares are actually traded) [4][20]. The difference between these figures, often called the “409A Delta”, typically ranges between 50% and 80% [4]. For instance, if the preferred share price is $100, common shares might be valued somewhere between $20 and $50.

Take SpaceX in early 2026 as an example. Its Series J preferred shares were priced at $110, while the 409A valuation for common stock was $45 (a 59% discount). Meanwhile, secondary market transactions for common shares cleared at $85, reflecting a 23% discount to preferred shares [4]. This discrepancy is largely due to the liquidation preferences and protective provisions enjoyed by preferred shareholders, which common shareholders do not benefit from. To get a clearer picture before investing, request a waterfall analysis. This will help you understand how proceeds are distributed in an exit scenario. In some cases, preferred shareholders’ preferences can consume over 75% of the proceeds, leaving common shareholders with much less than the headline valuation might suggest [4][19].

“In the secondary market, the buyer often knows more than the seller.” – Calcix Research Team [19]

Discounts in the secondary market depend on the company’s stage and its timeline to liquidity. In 2026, late-stage companies nearing an IPO (within one year) typically face discounts of 12% to 18%, while mid-stage companies with a longer horizon (around five years) can see discounts as high as 50% to 65% [19]. With the risk-free rate hovering around 4.5% in early 2026, investors are demanding larger discounts for illiquid assets [19]. These discount ranges reflect the market’s appetite for risk and should guide your pricing strategy. Also, companies with less than 12 to 15 months of cash runway face higher dilution risks, which should be factored into your valuation [3].

Compare the asking price to peers’ Price-to-Sales (P/S) ratios. For example, if similar companies trade at a P/S of 5x but your target’s pre-IPO valuation is at 10x, you’re likely paying a premium that may not be justified [3][10]. In the 2026 market, most companies require $100 million to $200 million in Annual Recurring Revenue to be IPO-ready [19]. If the company’s last funding round was over 18 months ago, adjust the valuation to account for changes in public market performance - such as declines in the SaaS index, which should lower private valuations accordingly [19].

“Time is the single most aggressive ‘tax’ on your private share value.” – Calcix Research Team [19]

Don’t forget to calculate your net proceeds after accounting for a 20% to 35% tax on gains [19]. The 2026 market has shown a clear preference for quality. Companies with a clear 18-month path to liquidity are trading at a premium compared to those with vague three-to-five-year exit plans [19]. Finally, check the company’s burn rate against its cash reserves. For instance, if a company burns $10 million monthly but has $200 million in the bank, it has a 20-month runway. While that provides some breathing room, it still requires close monitoring [10].

5. Examine Liquidity Terms, Exit Timeline, and Portfolio Fit

Liquidity and Portfolio Diversification Considerations

Pre-IPO investments come with a major caveat: liquidity isn’t guaranteed. Generally, these investments require holding periods of three to five years, though in some cases, they can extend anywhere from two to seven years before a liquidity event occurs [3]. Common exit routes include an IPO, a merger, an acquisition, or a secondary sale [21][22]. However, the landscape has shifted - by 2025, the average company age at IPO has climbed to 13 years [23]. This trend of companies staying private longer directly impacts liquidity timelines, making it essential to understand how such investments align with your broader risk strategy.

“For many of today’s top startups, an IPO isn’t about raising money - it’s a liquidity event.” – Stock Analysis [5]

To gauge the likelihood of an exit, start by checking whether the company has initiated the IPO filing process or attracted acquisition interest. Look for signs such as experienced finance and legal teams, PCAOB-compliant audits, or confidential draft registration statements submitted to the SEC - these are strong signals that an IPO could be 18 to 24 months away [13][3]. Be aware of legal restrictions and transfer limitations within the company’s capital structure, as these can further complicate your ability to exit through secondary markets [3][22]. Examining these details upfront is critical to managing liquidity risks.

Proper due diligence doesn’t stop at financial and legal analysis. It’s equally important to evaluate how the investment fits into your overall portfolio strategy. Experts recommend capping pre-IPO exposure at 10% to 20% of your total equity portfolio [3]. With 90% of startups failing [2][5], over-concentration in these high-risk, illiquid assets can be disastrous. Only invest funds you can afford to lock away for years - and possibly lose entirely. To mitigate risks, consider diversifying through Special Purpose Vehicles (SPVs) with minimum investments ranging from $10,000 to $25,000, or explore curated venture funds like the Fundrise Innovation Fund or ARK Venture Fund, which offer built-in diversification [4][5]. Spreading investments across sectors such as fintech, SaaS, AI, and manufacturing can also shield you from downturns in any single industry [3].

Lastly, take the time to model potential exit scenarios. Use sensitivity analysis to estimate the value of your common shares at various exit valuations (e.g., $500 million vs. $2 billion), factoring in the preference stack and liquidation waterfall [4]. Consulting a tax expert is also wise, as they can help you understand the tax implications of holding unlisted shares beyond 24 months, potentially qualifying for long-term capital gains rates [3]. Always ensure that shares are properly credited to the correct account - like a demat account in certain markets - before finalizing the transaction [3]. Your investment should align with both your liquidity needs and your risk tolerance.

Pre-IPO Investing: Risks, Rewards, and Strategy

Conclusion

Investing in pre-IPO companies requires a disciplined approach. Unlike public companies, private firms disclose far less information, creating potential gaps in knowledge and increasing the risk of misinformed decisions [3][21]. Without proper due diligence, structural complexities like liquidation waterfalls can result in common shareholders receiving minimal returns - even in a $400 million exit scenario [4]. The five steps outlined - verifying transaction sources, analyzing financials, reviewing legal structures, assessing valuations, and examining liquidity terms - serve as a practical guide to focus on the essentials.

“The real risk is in details not captured in the pitch deck.” – Bhaskar Ahuja, CFO & CIO [1]

Carefully revisiting financials, legal frameworks, valuations, and liquidity terms helps ensure your investments align with sound principles. Look for companies with at least 12–15 months of operational cash on hand [3]. Leadership stability is another key indicator - around 80% of successful tech IPOs have CFOs with prior exit experience [1]. Modeling various exit scenarios can help you evaluate when the preference stack clears [4]. Pay close attention to the “409A delta”, where the difference between headline valuations and the real value of common shares can range from 50–80% [4].

The pre-IPO market has grown considerably. By 2026, late-stage private companies are expected to collectively represent over $3 trillion in market capitalization, while about 18.5% of U.S. households now qualify as accredited investors [4]. But access to these opportunities doesn’t guarantee success. With typical lock-up periods lasting 3–5 years and a recommended 10–20% equity portfolio cap, aligning these investments with your risk tolerance is essential [3][5].

Top-performing companies generally exhibit net revenue retention above 130% and gross margins over 70% before going public [1]. If the financials don’t back up the narrative, it’s wise to walk away. Ultimately, thorough due diligence is the cornerstone of achieving sustainable returns in the unpredictable world of pre-IPO investing. While risks can’t be eliminated entirely, a methodical approach significantly enhances your chances of success in this challenging yet rewarding market.

FAQs

What documents should I request before buying pre-IPO shares?

Before buying pre-IPO shares, it’s crucial to gather and review essential documents to ensure you’re making a well-informed investment. Key documents to request include:

- Corporate governance records: These outline the company’s structure and decision-making processes.

- Financial statements and projections: These provide insight into the company’s current and future financial health.

- Intellectual property documents: These confirm the ownership and protection of key assets.

- Customer contracts and operational agreements: These reflect the company’s business relationships and day-to-day operations.

- Valuation and funding history: This helps you understand the company’s growth trajectory and past investment activity.

Taking the time to analyze these documents can give you a clearer picture of the company’s financial stability, legal standing, and overall operations.

How do I estimate what common shares are really worth after liquidation preferences?

When figuring out the value of common shares after accounting for liquidation preferences, the key is to analyze how the proceeds are allocated during a liquidity event. Preferred shareholders are typically first in line to receive their guaranteed payout - often referred to as a 1x preference or similar. Once their claims are satisfied, any leftover funds are divided among common shareholders based on their ownership percentages.

However, if the total proceeds fall short of covering the preferred shareholders’ preferences, common shares might end up with little or no value. By modeling different payout scenarios, you can better understand what common shareholders might realistically expect in various outcomes.

What are the biggest reasons I might not be able to sell my pre-IPO shares for years?

Selling pre-IPO shares can be a long waiting game due to various restrictions imposed by companies and regulatory bodies. Many businesses outright ban secondary market sales or require their approval before any transaction can occur. Even when sales are permitted, you might face lock-up periods - typically lasting six months after the IPO - and regulations like SEC Rule 144, which impose additional limitations. These rules are designed to maintain market stability and safeguard the company, often delaying when you can cash out your shares.