409A valuations are essential for private companies issuing stock options. They help set fair market value (FMV) for equity compensation, ensuring compliance with IRS rules and protecting employees from steep tax penalties. Here’s what you need to know:

- What is a 409A valuation? An independent appraisal to determine the FMV of a company’s common stock, required for setting strike prices of stock options.

- Why does it matter? Non-compliance can lead to 20% federal penalties, income taxes, and interest for employees.

- Key timing: Valuations are valid for 12 months but must be updated after significant events like funding rounds or acquisitions.

- Pre-IPO impact: As companies near an IPO, valuations face increased scrutiny to avoid "cheap stock" issues. Regular updates – quarterly or even per-grant – are common in the final 18-24 months before filing.

Costs vary by stage:

- Early-stage startups: $1,500–$3,500

- Series A-C: $3,500–$12,000

- Late-stage companies: $10,000–$25,000+

Methods used: Discounted Cash Flow (DCF), Comparable Company Analysis, and Option Pricing/Backsolve. The choice depends on company stage, financials, and recent funding activity.

To stay compliant:

- Schedule valuations around major events.

- Adjust frequency as IPO approaches.

- Work with experienced appraisers and engage external auditors early.

Takeaway: Proper 409A valuations ensure compliance, protect employees, and support a smooth pre-IPO process. Plan ahead to keep costs manageable and avoid risks.

What’s a 409A valuation, and why does it matter?

sbb-itb-c5fef17

When and Why 409A Valuations Are Required

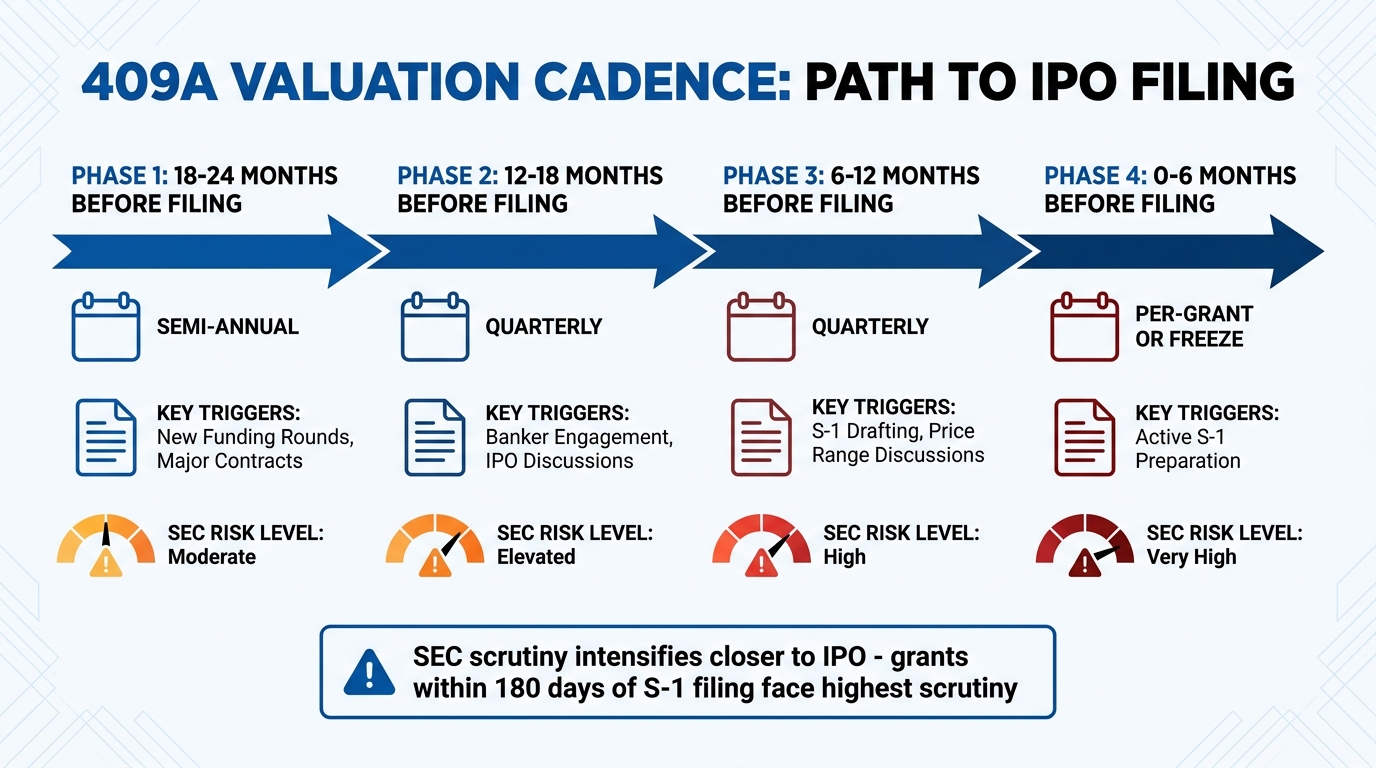

409A Valuation Timeline and Frequency Before IPO Filing

Knowing when to get a 409A valuation is key to avoiding hefty penalties. The IRS has clear rules about timing, and ignoring them can lead to serious financial consequences for both your company and its employees.

IRS Safe Harbor Rules

Obtaining an independent 409A valuation gives your company IRS safe harbor protection. This means the valuation is considered reasonable unless the IRS can prove otherwise – and only if it’s deemed "grossly unreasonable" [6]. A 409A valuation is valid for 12 months, but certain events can void this protection. These include a priced funding round, a major acquisition, or significant changes in financial performance. If any of these occur, you’ll need a new valuation before issuing additional stock options.

"Think of safe harbor as a shield that protects your company and your employees from IRS penalties."

Failing to comply with 409A rules can result in a 20% federal penalty, plus income tax and interest on the difference between the strike price and the fair market value [6].

This framework helps explain how valuation timing ties into key IPO milestones.

Pre-IPO Timing Considerations

The SEC closely examines option grants made in the three to five years before your IPO filing. Grants issued within 180 days of filing an S-1 face even more scrutiny, as the IPO price is often viewed as a foreseeable event [5].

To prepare for this, many companies adjust their valuation schedules as they approach an IPO. Here’s how the cadence typically changes:

- 18–24 months before filing: Semi-annual valuations, triggered by events like new funding rounds or major contracts.

- 12–18 months before filing: Quarterly valuations, especially as banker engagement or IPO discussions begin.

- 6–12 months before filing: Quarterly valuations continue, with focus on S-1 drafting and price range discussions.

- 0–6 months before filing: Valuations are done per grant or paused entirely to avoid "cheap stock" complications.

| Time Before IPO Filing | Recommended Cadence | Key Triggers | SEC Risk Level |

|---|---|---|---|

| 18–24 months | Semi-annual | New rounds, major contracts | Moderate |

| 12–18 months | Quarterly | Banker engagement, IPO discussions | Elevated |

| 6–12 months | Quarterly | S-1 drafting, price range discussions | High |

| 0–6 months | Per-grant or freeze | Active S-1 preparation | Very High |

As SEC scrutiny intensifies closer to an IPO, maintaining safe harbor protection becomes even more critical.

"The cost of a cheap stock restatement – in accounting fees, legal costs, delayed IPO timing, and reputational impact – is routinely measured in hundreds of thousands to millions of dollars."

- 409A-valuation.com [5]

To minimize risks of underpricing, companies should halt all option grants between signing a term sheet for a new funding round and obtaining an updated 409A valuation [3]. Additionally, involving external auditors early ensures everyone agrees on the valuation approach before setting strike prices [5].

3 Methods for Calculating 409A Valuations

Appraisers typically rely on three main approaches to determine a company’s fair market value. Each method is tailored to accommodate different business models and risk levels, making them suitable for both established companies and newer Web3 startups. Often, these methods are combined to arrive at a well-supported valuation.

Discounted Cash Flow (DCF) Method

The DCF method estimates your company’s current value by forecasting financial performance over 3–5 years and then discounting those future cash flows back to their present value using a discount rate[9]. This method is ideal for companies with steady revenue streams but is often used as a secondary check for early-stage Web3 startups with negative or unpredictable cash flows[8]. It’s important to avoid overly optimistic projections, as they can lead to inflated valuations and potential IRS audits[9].

"The resulting enterprise value represents what a hypothetical buyer would pay today for the company’s expected future cash generation."

For Web3 startups, the discount rate should reflect the sector’s high volatility, usually falling between 25% and 50% for early-stage companies[11]. To ensure accuracy, appoint a finance lead, such as a CFO, to consolidate data and align growth assumptions[9]. While thorough, the DCF method should be paired with market-based approaches to strengthen valuation credibility, especially for pre-IPO pricing.

Comparable Company Analysis

This method uses financial ratios from similar companies to estimate your company’s value. Appraisers apply the Guideline Public Company (GPC) and Guideline Transaction (GTM) methods, using data from public peers and recent mergers and acquisitions[17,24]. For startups without profits, Enterprise Value (EV) to Revenue multiples are common, while profitable companies are often evaluated using EV to EBITDA ratios[21,24]. Adjustments are then made for factors like company size, growth rates, and a Discount for Lack of Marketability (DLOM), which typically ranges from 15% to 35% for venture-backed startups[11].

"An independent, qualified and accurate 3rd party valuation will ensure compliance with tax and other regulatory requirements, as well as ensuring fairness for all stakeholders."

For Web3 startups, it’s crucial to select peers with similar revenue models (e.g., protocol fees versus SaaS subscriptions) and comparable regulatory environments[21,23]. The appraiser should clearly document why specific peers were chosen to withstand IRS scrutiny[11]. For companies with complex capital structures, methods like Option Pricing and Backsolve can provide additional clarity.

Option Pricing and Backsolve Methods

The Backsolve method is particularly useful within six months of a priced equity round[14]. It calculates the company’s total enterprise value by working backward from the price investors recently paid, grounding the valuation in actual market data rather than speculative forecasts[26,19].

This method treats each share class – whether preferred, common, options, or warrants – as a call option on the company’s total equity value[26,27]. It’s especially helpful for Web3 startups with complex capital structures, such as convertible preferred shares that offer downside protection while allowing upside participation through conversion to common stock[12].

"The backsolve method anchors value to real transactions, making it especially useful for fast growing startups with limited financial projections."

Backsolve calculations often value common stock at a steep discount – usually 60% to 80% below preferred shares – to reflect differences in marketability and liquidation preferences[2,29]. A final DLOM, typically between 12% and 25%, is applied to account for the illiquidity of private markets[8]. For later-stage companies with clear exit scenarios, like an IPO or acquisition, the Probability-Weighted Expected Return Method (PWERM) may be used instead of the Option Pricing Method (OPM)[28,29]. In cases where multiple liquidity events are anticipated, a hybrid approach may be employed[13]. By tying valuations to recent market transactions, these methods provide a solid basis for pre-IPO pricing and bolster investor confidence.

409A Valuation Costs by Company Stage

Grasping the costs associated with 409A valuations is crucial for planning budgets and timing funding rounds effectively. The price tag depends on factors like your company’s stage, the complexity of its structure, and how quickly you need the valuation completed.

Cost Ranges by Stage

The cost of a 409A valuation shifts depending on where your company is in its lifecycle. For pre-revenue and seed-stage startups with straightforward cap tables, the expense typically falls between $1,500 and $3,500[2]. As companies progress to Series A through Series C, costs rise to somewhere between $3,500 and $12,000[2]. For late-stage companies, valuations can range from $10,000 to $25,000 with boutique firms – or even exceed $50,000 if you go with a Big 4 accounting firm[2].

"The $2,000-$5,000 cost of a proper 409A valuation is cheap insurance against potentially millions in IRS penalties for your option holders."

One way to save on costs is through annual updates. These updates, when done by the same provider, are typically 40–60% cheaper than the initial valuation[16]. Negotiating discounted renewal rates upfront can be a smart move.

Now, let’s dig into the factors that influence these costs.

What Drives Valuation Costs

Several elements can push valuation costs higher:

- Additional security classes: Each class, such as warrants, convertible notes, or preferred shares, can tack on an extra $500 to $2,000[15].

- Complex liquidation preferences or participation rights: These can add another $1,000 to $3,000[15].

- International operations or dual reporting (e.g., US GAAP and IFRS): This complexity can increase costs by $2,000 to $10,000[15].

Timing is another critical factor. If you need a quick turnaround – under two weeks – expect to pay a 25–50% premium[15]. On the flip side, scheduling your valuation during Q1 or Q2 might score you an off-season discount of 10–15%[16].

Keeping your cap table clean and organized with tools like Carta or Pulley can also help. These tools can save you $1,000 to $2,000 in labor costs by giving appraisers ready-to-use data[16]. To avoid rush fees, plan your valuation at least 4–6 weeks in advance.

For companies requiring frequent updates, some providers now offer annual subscription models. These plans, priced between $5,000 and $10,000 per year, include unlimited refreshes and can be a cost-effective solution if you foresee multiple funding rounds or other significant events[2]. Additionally, bundling your 409A valuation with other appraisals – like M&A or IP valuations – can save you 15–25% on combined services[17].

Using 409A Valuations in Pre-IPO Pricing

Grasping how 409A valuations fit into your pre-IPO pricing strategy is crucial. These valuations establish the fair market value of common stock for tax purposes, while the pricing of preferred stock reflects negotiated terms, often with added rights. This distinction impacts everything from employee stock options to compliance with SEC requirements.

Common Stock vs. Preferred Stock Pricing

A 409A valuation determines the fair market value of common stock, primarily for tax compliance. In contrast, preferred stock pricing stems from negotiations, often including enhanced rights and privileges. For early-stage companies, common stock is typically priced at 10%–20% of the preferred stock value. This gap narrows significantly as the company approaches its IPO.

"409A is about taxes and compliance; preferred valuation is about negotiation and growth." – Adam Yohanan, Corporate Lawyer

As a business gets closer to filing its S-1, the fair market value of common stock begins to align more closely with the anticipated IPO price. About 18 to 24 months prior to an IPO, common stock values often reach 40%–65% of the expected IPO price, climbing to 65%–90% or higher in the final six months.

Here’s a breakdown of typical valuation ratios and methods by stage [5]:

| Stage | Common/Preferred Ratio | Dominant Methodology |

|---|---|---|

| Series A | 10%–20% | OPM |

| Series B–C | 20%–40% | OPM or PWERM |

| Pre-IPO (18–12 months) | 40%–65% | PWERM / Hybrid |

| Pre-IPO (6–0 months) | 65%–90%+ | PWERM (High IPO weighting) |

Understanding these trends is essential for Web3 startups and venture capitalists (VCs) aiming to leverage 409A valuations effectively in their pre-IPO strategies.

Practical Steps for Web3 Startups and VCs

Web3 startups often face added complexity due to instruments like SAFEs, convertible notes, and token-based compensation. To navigate these challenges and refine your pre-IPO pricing strategy, consider the following steps:

- Review your cap table thoroughly.

Ensure all SAFEs, convertible notes, and warrants are accurately accounted for, as these instruments affect how enterprise value is distributed across share classes. - Time valuations around significant events.

Schedule a new 409A valuation within 30 to 60 days of major events, such as closing a funding round, receiving an acquisition offer, or hitting a revenue milestone. For Web3 startups, this might also include protocol launches or major customer acquisitions. To avoid risks tied to contemporaneous knowledge, implement a grant freeze from the term sheet stage until the updated valuation is finalized. - Adjust valuation frequency as an IPO nears.

Begin with annual valuations but shift to semi-annual updates 18–24 months before filing an S-1. Move to quarterly updates when you’re 6–12 months out. In the final six months, consider per-grant valuations or temporarily freezing new equity grants to align with SEC expectations. - Upgrade your valuation provider strategically.

Early-stage companies may work with boutique firms, but as an IPO becomes more likely (12–18 months out), transitioning to a nationally recognized provider with IPO expertise is advisable. Pre-IPO valuations are more intricate, and costs may rise accordingly. - Switch valuation methods as needed.

Use the Option Pricing Model (OPM) Backsolve method after closing a priced round. As the IPO approaches, transition to the Probability-Weighted Expected Return Method (PWERM), which better reflects the anticipated public offering. - Engage external auditors early.

Share draft 409A reports with auditors before finalizing stock option grants. This ensures the fair market value aligns with ASC 718 standards, avoiding costly discrepancies during pre-IPO audits. - Document key milestones.

Keep detailed records of significant events, such as protocol launches, customer wins, or strategic partnerships, to support valuation adjustments. Additionally, adopt each 409A valuation through a formal board resolution before issuing new option grants to maintain safe harbor protection. - Explore bundled services.

For startups planning multiple funding rounds, consider subscription-based valuation services that include ongoing updates and cap table management. This approach can simplify processes and reduce costs over time.

Conclusion: Key Takeaways for Founders and Investors

Core Insights

A 409A valuation plays a crucial role in shaping equity compensation, safeguarding employees from hefty tax penalties, and building trust with investors and auditors. By opting for an independent valuation, companies gain safe harbor protection, shifting the burden to the IRS to prove that the valuation is "grossly unreasonable." This helps protect employees from a 20% federal excise tax on the difference between the strike price and fair market value [2,8,1].

At the seed stage, common stock is typically valued at 10%–20% of the preferred stock price, increasing to 70%–85% as the company approaches an IPO [13,12]. This discount reflects the added rights and protections of preferred shares, such as liquidation preferences and anti-dilution rights, which common stock does not offer.

"The real goal is to arrive at the lowest defensible fair market value that can withstand IRS scrutiny"

- Yin Wu, Founder of Pulley [1]

It’s important to note that material events – like priced funding rounds, significant changes in revenue, or M&A activity – can render an existing 409A valuation invalid [3]. Although valuations are generally valid for 12 months, they must be updated within 30 days of a funding round to maintain safe harbor [4].

These details provide a roadmap for ensuring compliance and driving strategic growth.

Next Steps

Pause option grants when a term sheet is executed, resuming only after updating the 409A valuation [3]. Start renewal valuations 30 to 45 days before the current valuation expires to avoid disruptions in offering options [4].

As your company evolves, consider shifting valuation methods – from OPM Backsolve to PWERM – as exit scenarios become clearer [3]. Plan to transition to a nationally recognized valuation provider 12–18 months before filing your S-1, and increase valuation frequency from annually to quarterly as the IPO approaches. Keep detailed records of material milestones and formally adopt each 409A valuation through board resolutions to ensure thorough documentation for M&A due diligence and audits [2,8].

FAQs

What counts as a “material event” that triggers a new 409A?

A "material event" refers to any occurrence that has a major impact on a company’s fair market value, prompting the need for a new 409A valuation. Common examples include fundraising rounds, periods of rapid growth, or structural changes within the company. These events can render the existing valuation irrelevant, even if it was conducted recently.

How do companies avoid “cheap stock” issues before an IPO?

Obtaining a proper 409A valuation is crucial for companies looking to avoid "cheap stock" issues. This process establishes the fair market value (FMV) of their common stock, ensuring compliance and accuracy. Here’s how companies can approach it:

- Schedule regular, independent 409A valuations to determine a defensible FMV for stock options.

- Hire a qualified third-party appraiser to guarantee compliance with IRS guidelines and secure safe harbor protection.

- Update valuations consistently to account for shifts in company value, especially leading up to an IPO.

Taking these steps helps companies stay compliant and avoid potential financial or legal complications.

What should founders prepare before a 409A valuation?

Founders need to have their key financial documents ready, such as financial statements, capitalization tables, and records of recent funding rounds. It’s equally important to ensure that all legal and organizational documents are current. Be prepared to share details about assets, liabilities, and the assumptions behind your valuation. This level of preparation not only ensures a more accurate valuation but also helps the independent appraiser produce a report that stands up to scrutiny.