Pre-IPO gains – profits from selling private shares before a company goes public – are taxed differently depending on where you live. Here’s a quick breakdown:

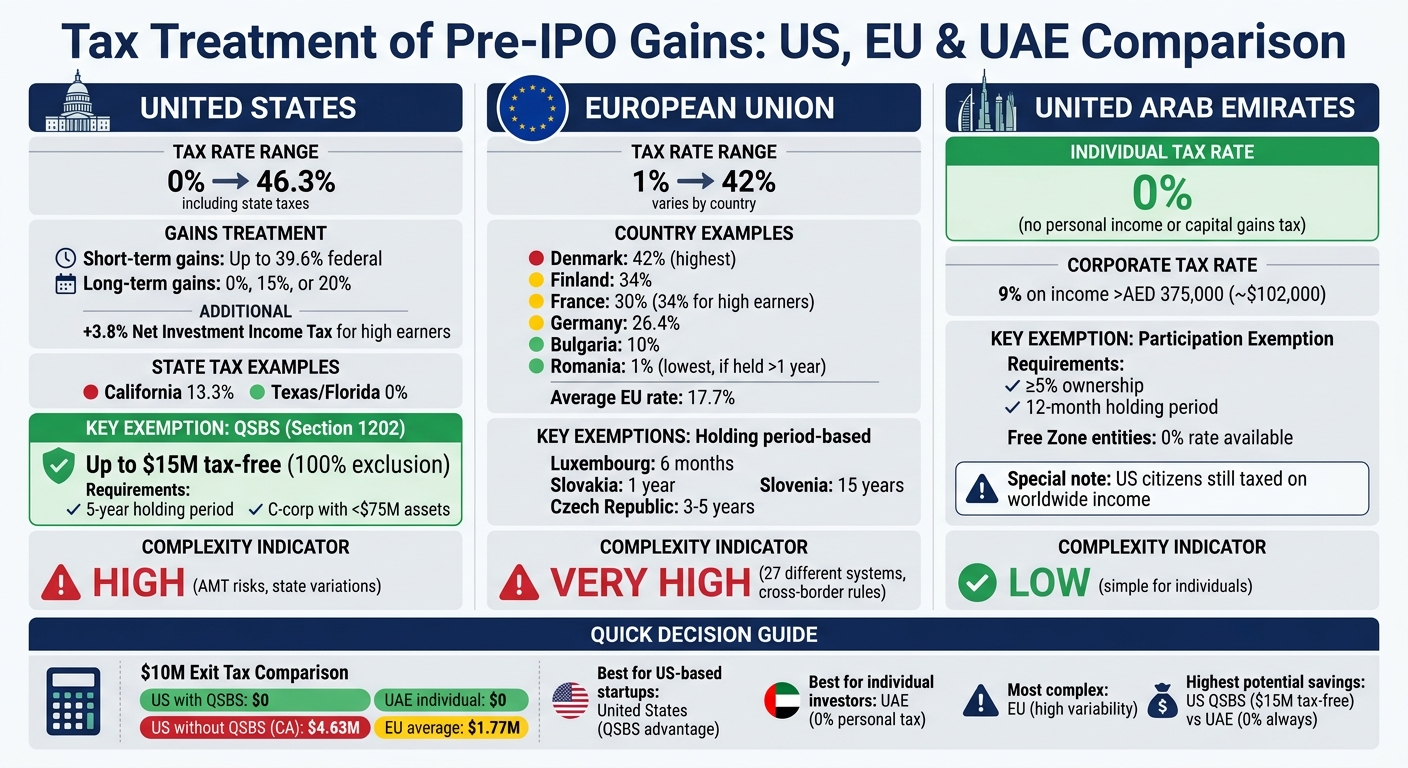

- United States: Taxes depend on holding periods. Short-term gains are taxed as high as 39.6% federally, plus state taxes. Long-term gains may qualify for lower rates (0%-23.8%). Special exemptions like QSBS (Section 1202) can eliminate federal taxes on gains up to $15 million, but strict rules apply.

- European Union: Tax rates vary widely, from 1% in Romania to 42% in Denmark. Some countries offer exemptions based on holding periods. Regulations differ across member states, adding complexity for cross-border investors.

- United Arab Emirates (UAE): Individuals enjoy 0% capital gains tax, making it a tax-friendly jurisdiction. However, U.S. citizens living in the UAE remain subject to U.S. global tax laws.

Quick Comparison

| Region | Tax Rate | Exemptions | Key Considerations |

|---|---|---|---|

| US | 0%-46.3% (including state taxes) | QSBS (up to $15M federal tax-free) | Complex rules; state taxes vary; IRS compliance required. |

| EU | 1%-42% (varies by country) | Based on holding periods (e.g., 1 year in Romania) | High variability across countries; cross-border rules add complexity. |

| UAE | 0% (individuals); 9% (corporate) | Participation exemptions for qualifying businesses | No personal tax reporting; U.S. citizens taxed on worldwide income by the U.S. system. |

Each jurisdiction offers unique opportunities and challenges. While the UAE provides a simple tax-free environment for individuals, the U.S. and EU present more nuanced systems with potential for exemptions but also higher complexity. Where you live and your investment strategy will heavily influence your after-tax returns.

Pre-IPO Capital Gains Tax Rates Comparison: US vs EU vs UAE

1. United States

Tax Rates

Tax rates in the U.S. for pre-IPO stock depend on how long you hold the shares. If you sell within 12 months of acquiring the stock, the gains are taxed as ordinary income, with a top federal rate of 39.6% starting in 2026 [1]. However, if you hold the stock for more than a year, the gains qualify for long-term capital gains rates of 0%, 15%, or 20% [4].

For high earners, an additional 3.8% Net Investment Income Tax applies once modified adjusted gross income exceeds $200,000 for single filers or $250,000 for joint filers. This increases the effective top federal rate on long-term capital gains to 23.8% [4][1].

State taxes also play a big role. For example, California has a 13.3% tax on capital gains, while states like Texas and Florida impose no state-level taxes. On a $50 million exit, this could mean a difference of up to $6.65 million in state taxes [2]. Washington state takes a different route with a 7% excise tax on long-term gains above $278,000 and 9.9% on gains exceeding $1 million [2].

Exemptions

The Qualified Small Business Stock (QSBS) exemption under Section 1202 of the tax code provides a major tax break for startup investors. If you hold qualifying shares for at least five years, you can exclude up to 100% of federal gains. This exclusion is capped at the greater of $15 million or 10 times your cost basis for stock issued after July 4, 2025 [8][9].

"Section 1202 of the Internal Revenue Code, often referred to as Qualified Small Business Stock (QSBS), is perhaps the greatest tax gift ever offered to the tech industry." – Calcix Research Team [1]

The One Big Beautiful Bill Act of 2025 expanded QSBS benefits significantly. Companies can now qualify with up to $75 million in gross assets at the time of stock issuance, up from the previous $50 million limit [8][11]. The legislation also introduced tiered exclusions: a 50% exclusion after three years and 75% after four years, replacing the previous all-or-nothing five-year rule [8][9].

However, not all states align with federal QSBS treatment. California, Pennsylvania, Mississippi, Alabama, and Washington D.C. tax the full gain at state rates regardless of federal exemptions [9][1]. Another option, Section 1045, allows investors to defer taxes by reinvesting QSBS proceeds into new QSBS within 60 days if sold before the five-year mark [5].

To benefit from these exemptions, investors need to follow specific reporting rules to stay compliant.

Reporting Requirements

Accurate reporting is critical to navigating tax rates and exemptions. For pre-IPO sales, investors must report gains on Form 8949 and summarize them on Schedule D, which is attached to their Form 1040 [12]. Venture capital funds, on the other hand, issue Schedule K-1 by March 15 each year, detailing each investor’s share of income, deductions, and credits [10].

Since the IRS doesn’t certify QSBS status, the burden of proof lies with the investor. A QSBS attestation letter from the issuing company, obtained during stock issuance and each financing round, is essential for audits [5].

High-gain investors should also make quarterly estimated tax payments to avoid penalties. For those exceeding income thresholds, the 3.8% Net Investment Income Tax adds another layer of complexity to tax planning [12][1].

Investment Considerations

Filing an 83(b) election within 30 days of exercising stock options or receiving restricted stock is a smart move. This locks in the current tax basis and starts the QSBS holding period [6][7]. Missing this deadline can result in millions of dollars in extra taxes.

"Choosing the wrong entity at formation is the most expensive avoidable error in startup law. On a $20 million exit, a founder who formed as an S corp instead of a C corp could owe over $3 million in federal capital gains tax that would have been $0 with QSBS." – Joe Wallin, Startup Law Attorney [5]

Where you live also matters. Moving to a state like Texas, Florida, or Nevada at least 6 to 12 months before an exit can eliminate state-level capital gains taxes. However, "trailing nexus" rules might still apply if shares were vested in a high-tax state [2][1].

Finally, the Alternative Minimum Tax (AMT) is a potential pitfall for those exercising Incentive Stock Options. Even without selling shares, the IRS can tax the difference between the exercise price and the fair market value, leading to a tax bill without liquid cash to cover it [1][6].

These strategies, combined with the tax rates and exemptions, can help investors reduce their overall tax liability significantly.

sbb-itb-c5fef17

2. European Union

Tax Rates

Capital gains tax rates across the European Union vary widely, ranging from 0% in some member states to as high as 42% in Denmark, with an average rate of 17.7% as of 2026 [13]. Denmark leads with a top rate of 42%, followed by Finland at 34%. On the other end, Bulgaria (10%) and Romania (1%) offer some of the lowest rates. Germany imposes a flat 25% tax, supplemented by a 5.5% surcharge, leading to a total rate of 26.4%. France applies a flat 30% rate, with an additional 4% surcharge for high-income earners, resulting in a maximum rate of 34% [13]. In 2026, Belgium introduced a 10% tax on capital gains from financial assets exceeding an annual exemption of about $10,800.

The Netherlands takes a different approach, taxing unrealized investment gains annually at 36% under its "Box 3" regime, which assumes a notional return of approximately 6.17% on investments [16][17]. However, startup founders and certain angel investors holding more than 5% ownership are exempt from this tax until an actual sale occurs.

For investors, it’s also important to note that the EU’s average integrated tax rate on corporate income sits at 35.7% [14]. Additionally, exemptions and holding period rules in different countries significantly impact the final tax burden.

Exemptions

Capital gains tax exemptions in the EU are influenced by holding periods and special conditions, which vary by country. Luxembourg offers an exemption after just 6 months, Slovakia after 1 year, and the Czech Republic requires holding periods of 3 to 5 years depending on the type of entity. Slovenia, however, demands a lengthy 15-year holding period [13][15]. Some nations, like Cyprus and Greece, provide 0% tax rates under specific conditions.

Romania stands out with its tiered system: capital gains are taxed at only 1% if the assets are held for more than a year, compared to 3% for shorter holding periods [13]. In the Netherlands, startups enjoy a tax exemption if they are less than five years old, have annual revenues below $32.4 million, and are not owned more than 25% by non-startup entities. Once these conditions are no longer met, small shareholders are taxed at 36% on unrealized gains [16].

"The real risk lies in the broader signal this sends to mobile capital in a Europe already struggling to compete with the United States for venture investment."

– Daniel Gray, Contextual Solutions [16]

France and Italy have introduced measures to encourage investments in innovative startups. France expanded its tax deductions, while Italy offers deductions ranging from 50% to 65%. These incentives aim to retain capital, especially as nearly 30% of European unicorns relocated their headquarters between 2008 and 2021 [16].

Reporting Requirements

The EU’s varied tax systems also bring differing reporting requirements. Investors typically report capital gains when they sell, gift, or emigrate. For those holding "substantial interests" (usually 5% or more), separate corporate or specialized tax regimes may apply [16].

In the Netherlands, pre-IPO founders benefit from "Box 2" treatment, where gains are taxed between 24.5% and 31% only when realized, avoiding the 36% annual tax on unrealized gains [16].

From January 1, 2026, the EU Directive on Administrative Cooperation (DAC8) will require service providers to report transaction data on crypto-assets and tokenized assets. The first data exchanges are expected in early 2027 [17]. Additionally, some countries, like Austria, France, and Norway, impose exit taxes on unrealized gains when individuals change their tax residency. The Netherlands allows deferral of such exit taxes over 12 years [15][16]. These evolving reporting frameworks are critical for planning tax-efficient exits, especially for pre-IPO investments.

Investment Considerations

When navigating the EU’s tax landscape, timing is everything. Missing key holding period thresholds can lead to higher taxes, such as Slovakia’s one-year exemption compared to the Czech Republic’s three-year requirement, where rates can climb up to 42% [13][15].

In the Netherlands, startup investors need to be mindful of the "cliff" effect. Once a startup exceeds five years in age or annual revenues surpass $32.4 million, small shareholders lose their favorable tax treatment and face the 36% tax on unrealized gains [16]. This creates a strong incentive to exit before hitting these thresholds.

"Higher taxes also cause investors to sell their assets less frequently, which leads to fewer taxes being assessed. This is known as the realization or lock-in effect."

– Alex Mengden, Economist, Tax Foundation [13]

Cross-border investments add another layer of complexity due to the lack of harmonized tax rules across EU member states – an issue institutional investors must carefully consider when structuring deals [14][18]. Notably, reforms in the Netherlands set for 2027 will allow employee stock options to be taxed only upon the sale of shares, rather than at the time of exercise or vesting, providing greater flexibility for startup employees [16].

3. United Arab Emirates

Tax Rates

In the UAE, individuals are not subject to personal income or capital gains tax, meaning that selling pre-IPO shares doesn’t result in any tax liability. However, U.S. citizens living in the UAE are still taxed on their worldwide income, including capital gains, due to the U.S.’s citizenship-based taxation policy.

For businesses, the UAE has implemented a 9% federal Corporate Tax on taxable income exceeding AED 375,000 (around $102,000). Income below this amount remains tax-free [20][22]. Additionally, capital gains from share sales can be entirely exempt if the company qualifies by holding at least a 5% ownership (referred to as a "Qualifying Shareholding") for a minimum of 12 consecutive months. Companies operating as Qualifying Free Zone Persons can enjoy a 0% tax rate on capital gains and dividends, provided they meet specific substance requirements.

"The UAE does not impose any capital gains tax on individuals, regardless of residency status."

– Titan Wealth International [3]

Next, let’s explore the exemptions available for UAE-based holding companies and investment funds.

Exemptions

The Participation Exemption is a key benefit for holding companies in the UAE. To qualify, a company must hold at least 5% of the shares for 12 consecutive months. Additionally, the subsidiary being sold must be subject to a corporate tax rate of at least 9% in its home country, and no more than 50% of its assets can consist of non-qualifying interests [19][20].

"The Participation Exemption makes the UAE an attractive location for holding companies… It allows for the tax‑free disposal of underperforming assets or the profitable exit from successful ventures."

– Excellence Accounting Services [21]

Investment funds have their own set of benefits. Funds can apply for "Qualifying Investment Fund" (QIF) or "Qualifying Limited Partnership" (QLP) status, which grants them full exemption from Corporate Tax. This is outlined in Cabinet Decision No. 34 of 2025, effective from March 27, 2025. The UAE also offers restructuring reliefs, such as Intra-Group Transfer Relief, which allows tax-neutral transfers of assets during mergers or reorganizations, deferring tax on gains as long as companies maintain 75% group ownership for at least two years [21].

Reporting Requirements

Even when capital gains qualify for exemptions, UAE entities are required to report all gains in their annual Corporate Tax return. They must also maintain detailed records, such as proof of ownership, holding period documentation, purchase agreements, and tax residency certificates for the investee company, to validate exemption claims during audits [20][21].

For individual investors, capital gains are generally free from reporting or tax obligations. However, if an individual’s investment activities become systematic enough to require a commercial license – essentially operating as a business – those gains are taxed as business income at the 9% rate and must be reported.

Investment Considerations

To make the most of the UAE’s tax framework, timing and structure are critical.

Corporate investors need to ensure the 12-month holding period for the Participation Exemption is met; exiting even a day early will result in the 9% Corporate Tax being applied. For individual investors, the UAE offers simplicity, as there’s no tax or reporting required for personal investments. Institutional investors, on the other hand, should establish a Qualifying Shareholding structure well in advance of a pre-IPO exit to benefit from the exemption. Free Zone entities must also confirm they are not engaged in excluded activities (like banking or insurance) that could disqualify them from the 0% tax rate.

One important consideration is the absence of a tax treaty between the UAE and the U.S., which can present challenges for estate planning. For UAE residents who are not U.S. citizens, U.S.-based assets are only exempt from U.S. estate tax up to $60,000, compared to the $13.99 million exemption available to U.S. citizens as of 2025 [3].

How to Avoid Capital Gains Tax on Startup Stock (QSBS Explained)

Advantages and Disadvantages

This section breaks down the key trade-offs for pre-IPO investors across three jurisdictions: the United States, the United Arab Emirates (UAE), and the European Union (EU). Each location offers a different mix of benefits and challenges, making jurisdictional selection a crucial factor for optimizing returns.

The United States stands out with a strong tax incentive through Section 1202, also known as Qualified Small Business Stock (QSBS). This provision allows for a 100% federal tax exclusion on gains up to $15 million, provided the stock is held for at least five years[2]. For qualifying exits, this can reduce the federal tax rate to 0%. However, navigating the U.S. tax system isn’t straightforward. Investors face hurdles like the Alternative Minimum Tax (AMT) when exercising Incentive Stock Options, the 3.8% Net Investment Income Tax for high earners, and state-level tax complications, as some states don’t align with QSBS rules[1].

"State capital gains tax planning represents one of the single highest-ROI tax strategies available to venture-backed founders"

– Peyton Carr, Co-Founder of Keystone Global Partners[2]

The United Arab Emirates offers a much simpler tax framework for individual investors, with 0% personal income and capital gains tax[3][25]. This eliminates the need for personal tax reporting, making it particularly appealing to founders and angel investors. However, the UAE’s lack of a tax treaty with the U.S. creates challenges. For example, U.S.-sourced dividends are subject to a flat 30% withholding tax, and the estate tax exemption for non-resident aliens is capped at just $60,000, compared to $13.99 million for U.S. citizens[3][25].

"US tax rules do not care that local personal income tax is zero. Net self-employment income is still reportable in the US"

– Huntly Mayo-Malasky, CEO of Taxes for Expats[24]

The European Union presents a mixed picture. While some member states, like Ireland, offer low corporate tax rates (12.5% to 15%)[23], individual capital gains taxes are often high – 33% in Ireland and 30% in France[23]. Beyond taxes, regulatory hurdles have grown. By 2024, 24 out of 27 EU member states had adopted Foreign Direct Investment (FDI) screening, leading to a 75% increase in reviewed transactions (3,136 in total)[26]. These reviews can delay cross-border deals by 12 to 24 months, with penalties for non-compliance reaching up to $60 million[26]. For venture capitalists, this regulatory complexity can significantly impact liquidity planning, especially as mergers and acquisitions (M&A) accounted for 98% of all VC-backed exits globally by mid-2025[26].

Here’s a snapshot of the trade-offs across these jurisdictions:

| Jurisdiction | Key Advantage | Key Disadvantage | Effective Tax Rate |

|---|---|---|---|

| United States | QSBS: 100% exclusion on gains up to $15M[2] | High complexity (AMT, state tax traps)[1] | 0% to 46.3%[1] |

| UAE | 0% personal income & CGT; simple reporting[3][25] | No US tax treaty; 30% withholding on US dividends[3][25] | 0% (individuals) / 9%[23][24] |

| EU (General) | Low corporate rates in select jurisdictions (e.g., Ireland 12.5%-15%)[23] | High individual CGT (30–33%) and extended FDI delays[23][26] | 30% to 33%[23] |

This comparison highlights how tax policies directly affect net returns. For instance, on a $10 million exit, a 0% capital gains tax (CGT) regime could deliver $4 million more in after-tax proceeds compared to a 40% tax rate[26]. Understanding these differences is essential for investors, as the effective tax rate can vary widely. A short-term sale in California, for example, could result in a 46.3% effective tax rate, while a QSBS-eligible sale might be taxed at 0%[1].

Conclusion

Choosing the right jurisdiction for pre-IPO investments depends heavily on the investor’s profile and strategic goals. For venture capitalists targeting U.S.-based startups, Section 1202 (QSBS) offers a major tax advantage, potentially eliminating federal taxes on gains up to $15 million for stock acquired after July 4, 2025[2]. That said, these benefits come with strings attached: a mandatory five-year holding period and varying state-level tax treatments that require careful planning[1]. These U.S.-centric strategies stand in contrast to approaches used in other global markets.

Retail investors face their own set of tax considerations. U.S. citizens can benefit by qualifying for QSBS and, when feasible, relocating to zero-tax states like Texas or Florida at least 6–12 months before a major exit[2]. While the UAE’s 0% capital gains tax is attractive, U.S. citizens are still subject to federal taxes on their worldwide income, limiting the appeal of such jurisdictions for individual investors[3].

On the other hand, institutional investors can take advantage of the UAE’s DIFC and ADGM frameworks, which provide tax-neutral structures like the Qualifying Investment Fund (QIF) and Qualifying Limited Partnership (QLP). These designations, effective March 27, 2025, streamline compliance by bypassing U.S. AMT issues and EU cross-border tax complexities[27]. However, managing ownership thresholds remains a critical consideration for maintaining these benefits[27].

The upcoming 2026 U.S. tax changes add urgency to strategic planning. With the top federal ordinary income tax rate projected to return to 39.6%[1], investors holding pre-IPO stock should carefully model exit strategies to maximize after-tax returns. For cross-border investors, extended FDI review timelines in the EU – now stretching to 12–24 months for many transactions – underscore the importance of early planning to maintain liquidity[26]. These insights emphasize that proactive, jurisdiction-specific strategies are key to optimizing tax outcomes across global markets.

FAQs

Do my pre-IPO shares qualify for QSBS?

Your pre-IPO shares might be eligible for QSBS (Qualified Small Business Stock) benefits if they align with the requirements outlined in Section 1202 of the Internal Revenue Code. To qualify, you need to have acquired the shares directly at original issuance, held them for more than five years, and ensured the issuing company meets the "active business" criteria. Recent changes in legislation have broadened certain QSBS advantages, which could simplify the qualification process.

What records do I need to prove QSBS in an IRS audit?

To demonstrate QSBS eligibility during an IRS audit, it’s crucial to maintain detailed records that confirm the stock complies with Section 1202 requirements. Key documentation to keep includes:

- Stock issuance details: Proof of when and how the stock was issued.

- Company qualification status: Evidence that the company met the necessary criteria at the time of issuance.

- Holding period: Records showing you held the stock for the required length of time.

- Acquisition specifics: Information on how the stock was acquired.

Additionally, support your claim with timely attestations from valuation experts. Keeping organized, accurate records is essential to back up your eligibility.

If I move (or become a UAE resident), which country taxes my pre-IPO gain?

As a UAE resident, you generally don’t have to worry about taxes on pre-IPO gains, thanks to the absence of capital gains tax for individuals acting in a personal capacity. However, if you’ve recently moved from a country that does impose capital gains taxes – like some European nations with exit taxes on unrealized gains – you might still be liable for taxes in your former country when you leave.