Side letters are supplemental agreements that modify or clarify investment terms between fund managers (GPs) and investors (LPs). These agreements are particularly valuable for tailoring rights to meet specific legal, tax, or governance needs. In fast-evolving sectors like Web3, side letters address unique challenges such as token allocations, decentralized governance, and compliance with regulations like ERISA.

Key Takeaways:

- Information Rights: Access to financials, cap table updates, and event notifications ensures transparency.

- Pro Rata Rights: Protect your ownership by participating in future funding rounds.

- MFN Clauses: Guarantee access to better terms offered to others.

- Token Allocation: Secure rights to future tokens in Web3 deals through side letters or warrants.

- Governance Rights: Gain board observation privileges without full board liability.

Sophisticated investors should prioritize these provisions to maintain influence, manage risks, and maximize returns while navigating complex investment landscapes. These agreements are your leverage to secure terms that align with your goals.

5 Essential Side Letter Terms for Sophisticated Investors

Terms Sophisticated Investors Should Demand

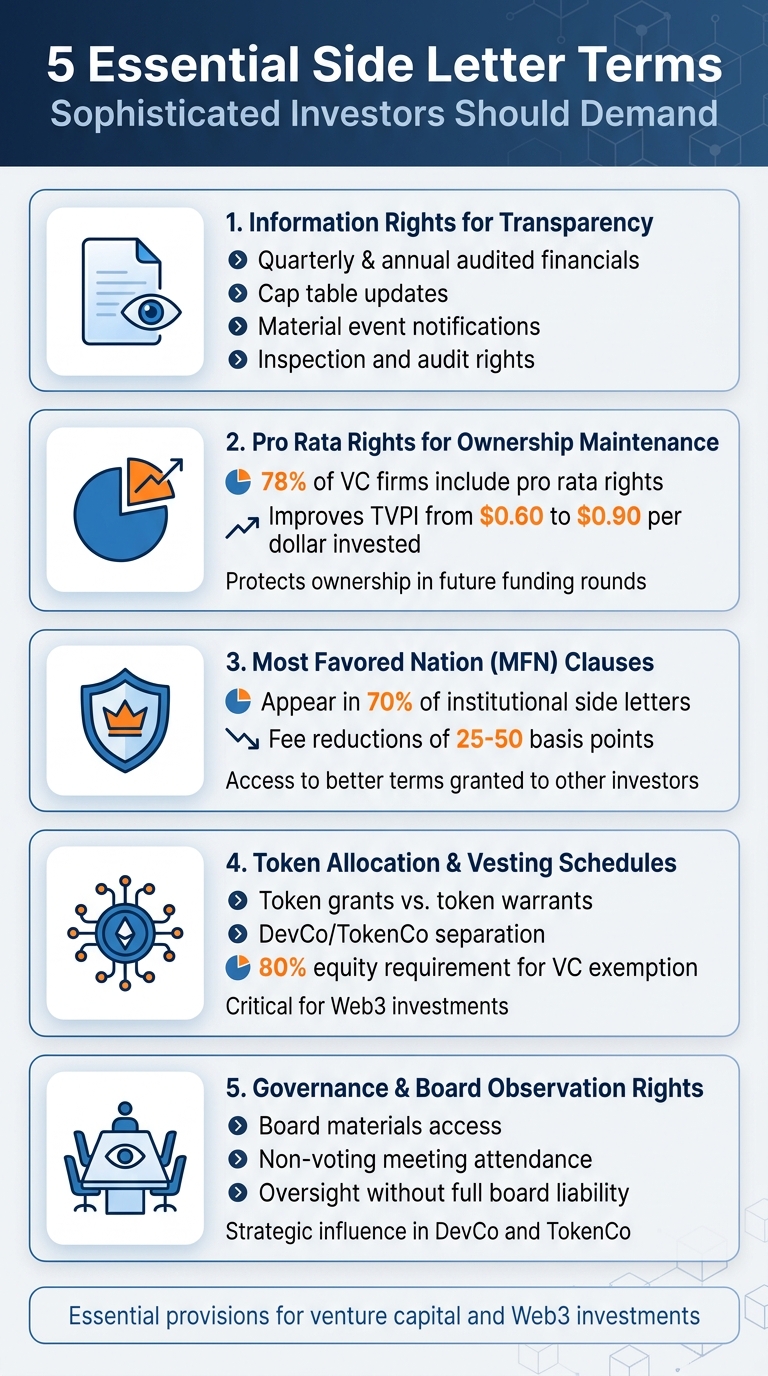

Information Rights for Transparency

Transparency is critical for effective portfolio management. Sophisticated investors should insist on access to quarterly and annual audited financials, including profit and loss statements, balance sheets, and detailed capital account statements [2][10]. Updates to the cap table are equally important for tracking dilution, while annual budget plans provide insight into burn rates and runway projections [4].

Institutional investors often require direct access to portfolio company financials for underwriting and risk management [2]. Additionally, the right to receive early notice of material events – such as financing rounds, significant transactions, or key personnel changes – is essential [10][1][4]. Inspection and audit rights, which allow on-site due diligence visits to fund managers or portfolio companies, add another layer of oversight [1]. To reduce administrative strain, these rights are typically reserved for "Major Investors" who meet specific investment thresholds [4].

These measures are not just about oversight – they also help investors maintain influence, a priority further supported by pro rata provisions.

Pro Rata Rights for Ownership Maintenance

Pro rata rights are a key tool for investors to preserve their ownership stakes as ventures grow. These rights enable investors to purchase additional shares in future funding rounds, ensuring their ownership percentage remains intact [11]. In fact, 78% of venture capital firms include pro rata rights in their deals [11][12]. Why? Data shows that exercising these rights can improve TVPI ratios from $0.60 to $0.90 per dollar invested [12].

In Web3 deals, pro rata rights are often outlined in side letters attached to SAFEs or convertible instruments, ensuring token allocation when a protocol launches [5][6]. A Token Side Letter gives investors the option to receive tokens as part of their equity agreement, while a Token Warrant allows them to purchase tokens at a fixed price or discount [5][6].

Some investors negotiate "super pro rata" rights, which allow them to increase their ownership percentage. While this can be attractive for high-conviction investors, founders need to be cautious, as over-granting such rights can lead to "cap table congestion", complicating future funding rounds [12][4]. To streamline processes, investors often agree to exercise windows of 5–10 business days during fast-paced funding rounds [2]. Sunset provisions, which terminate pro rata rights after events like an IPO or change of control, can also help manage long-term obligations [11][4].

Most Favored Nation (MFN) Clauses

MFN clauses are a powerful tool in side letter negotiations. These provisions ensure that an investor can access any better terms granted to others in the same deal or fund, safeguarding against "economic dilution" [2][13]. If a later investor secures more favorable terms, the MFN clause allows the original investor to match them.

"The most favored nation side letter clause is arguably the most widely requested provision in the entire LP side letter ecosystem." – Michael Kaufman, Founder & Editor-in-Chief, VC Beast [2]

MFN clauses are particularly common, appearing in 70% of institutional side letters [13]. For instance, large investors often negotiate management fee reductions of 25 to 50 basis points through these clauses [13]. It’s important to distinguish between the right to elect better terms and the right to be notified of them. Notification rights require the GP to disclose new side letters, ensuring transparency.

These clauses are often "tiered" based on investment size, meaning an investor’s MFN rights apply only to others who invested an equal or smaller amount [2]. Investors should negotiate access to the full text of other side letters during the election window, as summaries provided by GPs may omit critical details [13]. In Web3 deals, MFNs are especially important for "Token Side Letters." For example, if a later VC negotiates a shorter lock-up period or a higher percentage of unlocked tokens at the Token Generation Event (TGE), early investors can claim those terms.

While MFN clauses protect against unfavorable changes, token allocation terms ensure fair participation in the evolving digital asset space.

Token Allocation and Vesting Schedules

Token rights in Web3 deals come in several forms, each with distinct implications for equity-to-token conversions. Token grants allow investors to receive tokens without extra payment, while token warrants require a separate purchase under specific terms [5].

Flexibility is key here. Early-stage agreements should avoid fixed token prices or launch dates [5]. The separation between the development company (DevCo) and the token-issuing entity (TokenCo) is also critical. Typically, DevCo handles Token Side Letters, while TokenCo manages Token Warrants [5]. This division helps ensure compliance with the "Venture Capital Adviser Exemption", which requires that 80% of capital be allocated to equity securities [8].

Token vesting schedules should align with equity vesting to ensure long-term commitment and stability. Investors should prioritize transparency around token unlock schedules, total supply allocations, and any team or founder vesting terms that could affect token prices upon release.

Governance and Board Observation Rights

Governance rights offer investors a strategic role without the legal responsibilities of full board membership. This is especially important in Web3, where decentralized governance models often complicate traditional decision-making.

Observation rights typically include access to board materials, attendance at meetings (non-voting), and advance notice of major actions. In Web3 projects, these rights extend to discussions about tokenomics, protocol upgrades, and treasury management. Investors should clarify whether these rights apply to both DevCo and TokenCo, as governance structures may differ between the two.

While managing multiple observers can be challenging, these rights are often reserved for investors meeting a minimum threshold. The advantages are clear: experienced investors can provide valuable insights into scaling, regulatory compliance, and ecosystem development. Side letters should specify the duration of these rights and whether they continue through liquidity events or transfer to successor funds.

sbb-itb-c5fef17

How to Negotiate Better Side Letter Terms

Using Leverage in Negotiations

Timing, market conditions, and your unique contributions can all work in your favor during negotiations. For instance, during slower fundraising periods, fund managers often take longer to close deals, giving investors more room to negotiate customized terms [9]. If you’re an anchor investor committing a large amount of capital, you might be able to secure reduced management fees – say, 1.5% instead of the usual 2% – or gain enhanced co-investment rights [2][10].

It’s not just about the size of your investment; the value you bring to the table also matters. If you offer expertise in areas like Web3, regulatory frameworks, or industry connections, you could use this to negotiate better terms. The shifting market dynamics in Q3 2023, with down rounds hitting 27% – the highest since 2014 – have tilted negotiating power toward investors [14].

"Side letters are where LPs exercise real leverage."

- Michael Kaufman, Founder & Editor-in-Chief, VC Beast [2]

In the Web3 space, the 80/20 compliance rule can be a powerful tool. To meet the Venture Capital Adviser Exemption, funds must allocate 80% of their capital to equity [8]. This creates room to negotiate bundled deals, such as pairing equity with token warrants. Token warrants, in particular, often come with steep discounts – up to 99.95% – making them an attractive option [5].

Prioritizing and Sequencing Terms

Not all terms in a side letter carry the same weight. Start by addressing mandatory regulatory and tax requirements. These are typically non-negotiable and driven by legal obligations rather than investor preferences [2][1].

Once those are settled, shift your focus to economic terms, especially if you’re committing a significant amount of capital. Fee discounts and preferential carried interest terms can make a big difference in reducing your overall costs [2][1]. Establishing your status as a "Major Investor" or "Anchor Investor" is also key. This designation can unlock valuable rights like MFN clauses, board observer seats, and pro rata rights [4][2][1].

"Institutional LPs – particularly fund-of-funds and pensions – treat MFN as non-negotiable table stakes."

- Michael Kaufman, Founder & Editor-in-Chief, VC Beast [2]

For Web3 investments, it’s crucial to decide on the legal instrument early. Depending on the jurisdiction, you may need to choose between a Token Side Letter and a Token Warrant – warrants are often preferred in the U.S. for regulatory reasons – before finalizing token allocations or vesting schedules [5][8]. Institutional investors with fiduciary responsibilities should also prioritize transparency and reporting rights to meet internal oversight requirements [9][7].

A side letter matrix can help track the terms granted to different investors, ensuring compliance with MFN clauses and avoiding conflicting obligations [2]. This structured approach helps align interests between founders and investors.

Aligning Founder and Investor Interests

The best negotiations create value for both sides. Before entering discussions in the Web3 space, take the time to understand the founder’s goals and constraints. For example, they may want to avoid excessive reporting requirements or minimize shareholder dilution. Framing your requests in a way that addresses these concerns can lead to better outcomes for everyone involved [15].

Match privileges like board observer seats or enhanced voting rights to your level of contribution [15][16]. Be careful not to push for terms that could lead to a ratcheting effect, where future investors demand even better provisions, complicating future fundraising efforts [15][16].

"The managers who handle side letters well treat them like a product – standardized, tiered, and consistent."

- VC Beast [16]

When requesting reporting or transparency requirements, ensure they’re realistic and won’t disrupt the company’s operations [15][16]. If you’re negotiating MFN clauses, consider adding carve-outs for co-investment rights or fee breaks offered to fund employees. This protects the general partner’s ability to attract strategic partners while safeguarding your interests [2][1].

Set clear boundaries on non-negotiables before negotiations begin. Identify any terms that could negatively impact existing stakeholders or limit future fundraising flexibility, and communicate these upfront [15]. Engage legal counsel early to flag potential governance issues like restrictive veto rights or unequal exit preferences [15][2]. Lastly, maintaining open communication with existing investors about the rationale for side letters can help build trust and reduce concerns about preferential treatment [15].

Enforcement and Dispute Resolution Provisions

Setting Up Enforcement Mechanisms

The enforceability of a side letter is what gives it real value. Without a clear path to enforcement, even the most favorable terms can fall flat. To ensure this, start by addressing capital call remedies. These provisions lay out what happens if you’re late on a capital call or face a temporary default. Side letters can adjust standard penalties to offer protections or leniency tailored to your specific needs [10].

For larger investors, negotiating GP removal rights below the standard LPA threshold is crucial. This gives you greater control if the fund manager’s performance declines [2]. If you’re an institutional investor dealing with regulations like the Volcker Rule, include regulatory withdrawal rights. These allow you to exit the fund if staying in would cause compliance issues [2].

Provisions like Right of First Refusal (ROFR) and Right of First Offer (ROFO) are key to safeguarding your ownership stake. They give you priority when other investors want to sell or when the company considers a sale [10][4]. This is especially relevant in Web3 deals, where secondary markets for tokens and equity can be unpredictable. For public institutional investors, securing FOIA cooperation protocols helps protect sensitive fund data [2].

To enforce MFN rights, establish a formal notice period and a 30–60 day election window. Fund managers should also maintain a side letter matrix to track all granted provisions and ensure compliance across the investor base [2].

These mechanisms lay the groundwork for effective dispute resolution, ensuring that all negotiated terms can be upheld.

Choosing Dispute Resolution Methods

In the complex regulatory environment of Web3, dispute resolution needs to be carefully tailored. The U.S. presents particular challenges, as tokens often risk being classified as securities. This makes selecting the right jurisdiction and approach critical for managing regulatory uncertainty.

For U.S.-based projects, token warrants are often a better choice than token side letters. Warrants enable the Developer Company (DevCo) to transfer obligations to a Token Issuer Company (TokenCo), reducing exposure to U.S. regulatory scrutiny [5]. In fact, as of August 2025, Legal Nodes recommended that Web3 startups, especially those with Delaware C-Corp development labs, use SAFE documents paired with token warrants instead of side letters. This approach minimizes the risk of tokens being treated as securities under U.S. law [5].

"Because using a Token Side Letter gives the Developer Company the responsibility to distribute the tokens, it is highly recommended to use a Token Warrant if you’re operating out of the U.S."

To streamline disputes over token distribution, entity separation ensures these matters are exclusively handled by TokenCo [5][6]. If an SPV cannot legally hold or distribute tokens, include assignment rights. These provisions allow the SPV to transfer warrant rights directly to its members on a pro-rata basis [8].

Finally, always cross-check your side letter provisions against the LPA to avoid contradictions with the fund’s core governance documents. For example, German pension funds require side letter provisions on transfer rights to demonstrate "free transferability" for regulatory compliance [3].

Key Takeaways for Sophisticated Investors

Summary of Core Terms

When negotiating side letters, make sure to secure these five key provisions:

- Information rights: These grant access to quarterly and annual financial reports, cap table updates, and budget details. For Web3 investments, consider requesting direct portfolio company financials along with ESG/DEI reporting if your institution requires it [17][4][2][1].

- Pro rata rights: These protect your ownership percentage by allowing you to participate in future funding rounds, shielding you from dilution [17][4].

- MFN clauses: These ensure you automatically receive any better terms offered to other investors [2].

- Token allocation rights: Critical for Web3 deals, these rights – secured through Token Warrants (U.S.-based projects) or Token Side Letters (for non-U.S. entities) – guarantee your entitlement to future tokens issued by the project [18][20].

- Governance rights: Options like Board Observer seats and LPAC membership provide oversight without the liabilities tied to a full board seat [2][4].

These provisions, combined with competitive fee terms, form the foundation of a strong investment agreement. Typical fees include a 2% management fee and 20% carry, but anchor investors often negotiate reduced fees, such as 1.5%–1.75% management fees and a 15% carry [19][16]. For commitments of $10 million or more, securing an LPAC seat should be considered essential [2].

Final Recommendations for Negotiation

Negotiating side letters requires a strategic approach. Begin by identifying your non-negotiables, particularly regulatory requirements like ERISA compliance, UBTI/ECI tax considerations, or FOIA carve-outs for public institutions. These are especially critical in Web3 deals, as they aren’t mere preferences but legal necessities that the GP must address [2][1].

Adopt a tiered strategy for MFN clauses. Limit their scope to apply only to investors with similar or smaller commitments, allowing GPs the flexibility to offer distinct terms to larger anchor investors [2][1]. When requesting co-investment rights, use clear, binding language such as "shall offer" to avoid any ambiguity [2].

"Side letters are where LPs exercise real leverage." – Michael Kaufman, Founder & Editor-in-Chief, VC Beast [2]

Work with specialized fund formation counsel to avoid future issues. Keep a side letter matrix to track all granted provisions across your portfolio, ensuring GPs adhere to their agreements [2]. Since negotiated terms often become visible to other LPs, prioritize those that align with your broader strategy and provide the most value [2]. By applying these principles, your side letter can effectively support your Web3 investment goals.

Investment Fund Side Letters Explained

FAQs

When should I ask for a side letter in a VC deal?

During negotiations, it’s a good idea to request a side letter if you need certain rights, protections, or exemptions that aren’t included in the standard limited partnership agreement. This is especially common for large or strategic investors who have enough leverage to negotiate preferential terms. Side letters are often used to address specific concerns or ensure that the agreement aligns with your investment objectives.

How do I keep MFN rights from becoming too broad?

To keep MFN (Most Favored Nations) rights manageable, it’s crucial to define and narrow their scope in the side letter. Instead of offering broad, all-encompassing rights, focus on specific areas like fee structures or particular privileges. Also, make sure to set clear time limits for these clauses and outline processes for updates or renegotiations. This precise strategy helps avoid unintended consequences or overly extensive application of MFN provisions down the line.

In Web3, should I use a token side letter or a token warrant?

Choosing between a token side letter and a token warrant comes down to what you’re aiming to achieve with your investment.

A token side letter is all about customizing terms. It can grant investors special rights, such as preferential access to tokens or opportunities to co-invest. This is ideal if you’re looking for tailored benefits or unique arrangements in your investment.

On the other hand, a token warrant gives you the option to buy tokens at a predetermined price in the future. This approach ties your potential gains to the project’s success, making it a strategic choice if you’re betting on long-term growth.

In short, go with a side letter for personalized advantages, and choose a warrant if you’re focused on securing future token acquisition at a fixed price.