When investing in Web3, choosing between evergreen funds and closed-end funds comes down to liquidity, reinvestment, and timeline preferences. Here’s the breakdown:

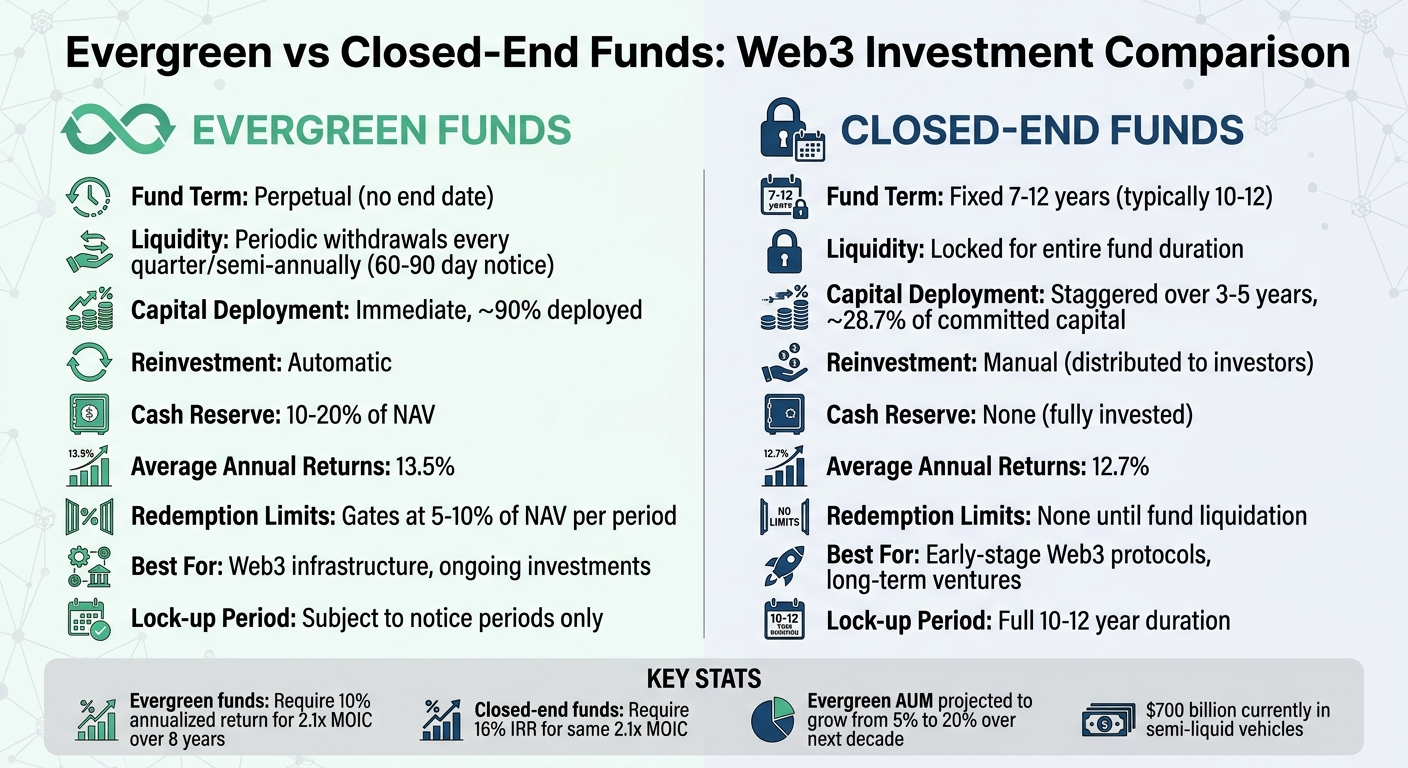

- Evergreen Funds: No set end date, continuous capital deployment, and periodic liquidity (quarterly or semi-annual). Gains are reinvested automatically, keeping capital actively working. However, they require cash reserves (10–20% of NAV), which can reduce returns during strong markets. Redemption gates (5–10% of NAV per period) may limit withdrawals during market stress.

- Closed-End Funds: Fixed lifespan (7–12 years) with locked capital. Returns are distributed to investors upon exits, requiring manual reinvestment. They avoid liquidity reserves, enabling full investment but are less flexible and subject to vintage risk.

Key Stats:

- Evergreen funds maintain ~90% capital deployment, with average annual returns of 13.5%.

- Closed-end funds invest ~28.7% of committed capital on average, with returns around 12.7%.

Quick Comparison:

| Feature | Evergreen Funds | Closed-End Funds |

|---|---|---|

| Fund Term | Perpetual | Fixed (7–12 years) |

| Liquidity | Periodic withdrawals (60–90 days) | Locked for fund duration |

| Reinvestment | Automatic | Manual |

| Capital Deployment | Immediate | Staggered over 3–5 years |

| Cash Reserve | 10–20% of NAV | None |

This decision depends on your goals: evergreen funds suit ongoing Web3 infrastructure investments, while closed-end funds fit long-term, early-stage projects.

Evergreen vs Closed-End Funds Comparison for Web3 Investors

Evergreen Funds: Structure, Liquidity, and Reinvestment

Core Characteristics of Evergreen Funds

Evergreen funds are designed to meet the fast-paced demands of Web3 markets by operating without a fixed end date. This perpetual structure allows for continuous capital deployment, unlike fixed-term funds that adhere to a set lifespan. Investors contribute their capital upfront, eliminating the need for lengthy capital calls and enabling quicker market reactions.

The valuation process for evergreen funds revolves around the fund’s Net Asset Value (NAV). NAV is calculated through regular assessments of the underlying assets, ensuring accurate pricing for new investments and redemptions. When a portfolio company exits – whether through a sale or token listing – the proceeds are automatically reinvested into new opportunities. This keeps the fund consistently active in the market and avoids the delays associated with raising additional capital.

These structural aspects are complemented by liquidity provisions tailored to investor needs.

How Evergreen Funds Handle Liquidity

Evergreen funds offer periodic liquidity windows, typically on a quarterly or semi-annual basis, with notice periods ranging from 60 to 90 days. To maintain portfolio stability, redemption gates are often set, limiting withdrawals to around 5% of the NAV per quarter. This approach offers more flexibility compared to closed-end funds, where capital is locked for a predetermined term.

A notable example is Blackstone‘s Real Estate Income Trust (BREIT). In December 2022, this $69 billion semi-liquid evergreen fund faced redemption requests exceeding its limits – 2% monthly and 5% quarterly. Blackstone responded by gating the fund, fulfilling less than 10% of the requests, which amounted to approximately $200 million in redemptions that month [6]. This scenario underscores the balance evergreen funds must strike between providing liquidity and protecting the portfolio, especially during market volatility when asset valuations may not immediately reflect real-time conditions.

To manage redemptions, evergreen funds often keep a cash reserve of 10–20%. For larger withdrawal requests, liquidating accounts are used, allowing payouts to occur gradually as assets are sold. This avoids the need to sell assets quickly at potentially unfavorable prices.

Reinvestment Approach in Evergreen Funds

Evergreen funds also excel in reinvestment strategies, offering a streamlined approach to capital recycling. Instead of distributing returns to investors after each deal, the General Partner manages reinvestment decisions at the portfolio level. This eliminates "reinvestment friction", a term used to describe the delays and logistical challenges investors face when redeploying distributions from closed-end funds.

"Continuous capital is not simply a product category, but a structural solution to the problem of compounding private returns efficiently in an inherently illiquid market." – PE 150 [2]

By keeping capital actively deployed, evergreen funds maintain higher levels of invested capital compared to traditional drawdown funds. Simulations suggest that evergreen structures can achieve a mean annual return of 13.5%, compared to 12.7% for rolling drawdown funds [2]. For institutional investors focused on Web3, this automatic recycling of capital aligns with long-term growth goals, reducing the effort required to reinvest distributions manually.

This reinvestment efficiency highlights a key advantage of evergreen funds over closed-end structures, which often face delays and inefficiencies in capital deployment.

sbb-itb-c5fef17

Closed-End Funds: Structure, Liquidity, and Reinvestment

Core Characteristics of Closed-End Funds

Closed-end funds follow a fixed timeline of 7 to 12 years, typically divided into three distinct phases: an investment period for deploying capital, a harvest phase for portfolio exits, and a final wind-down period [1][6]. Unlike evergreen models, these funds use a drawdown structure, where Limited Partners (LPs) commit capital upfront, and the General Partner (GP) calls on it gradually as investment opportunities arise [6].

This structure results in concentrated portfolios with 10 to 15 companies, compared to the 100+ holdings often seen in evergreen funds [6]. Such concentration aligns with the long-term strategies needed for early-stage Web3 ventures, where liquidity and valuations tend to be more opaque [1].

"Traditional closed-end (drawdown) private market funds… operate on fixed 8-10 year lifecycles." – Chris Bendtsen [6]

A key challenge for these funds is vintage risk. Returns are heavily influenced by the fund’s vintage year, meaning the specific timing of capital deployment and exits can significantly impact performance. This makes closed-end funds particularly sensitive to market cycles, which can affect liquidity events and the timing of reinvestment in Web3 ventures [7].

How Closed-End Funds Handle Liquidity

Closed-end funds are characterized by locked capital – investors cannot access their funds during the typical 7 to 10-year term [7]. Unlike open-ended structures, there are no interim redemption options; capital is returned only when portfolio companies are exited [6].

This locked structure provides a stable asset base, allowing portfolio managers to stay fully invested in illiquid Web3 assets without needing to reserve cash for withdrawals. However, this stability requires investors to ensure they have sufficient liquidity outside the fund to meet their financial needs during the lock-up period [6].

In some cases, closed-end funds offer a secondary market option. Shares of traditional listed closed-end funds can trade on stock exchanges, enabling investors to sell their shares at market prices. However, these shares often trade at a discount or premium to NAV (Net Asset Value), meaning the sale price depends on market sentiment rather than the actual value of the underlying assets [8].

"CEFs have a generally stable asset base that allows the portfolio manager to implement the fund’s investment strategy without having to manage inflows or redemption requests." – Morgan Stanley [8]

These liquidity constraints also influence how capital is reinvested, which brings additional challenges.

Reinvestment Approach in Closed-End Funds

The locked liquidity model creates hurdles for reinvesting capital, as proceeds from exits are distributed to LPs rather than reinvested. This manual redeployment process, combined with inevitable delays, adds to the fund’s J-curve effect. Early on, returns are negative due to management fees and investment costs, but they improve as portfolio companies mature and generate gains [1].

For Web3 funds, this effect is even more pronounced. Blockchain startups often require long development periods before reaching liquidity events, making patient capital a necessity.

Closed-end funds also face challenges as they approach their fixed termination date. Managers may be forced to sell assets or return capital regardless of whether market conditions are favorable [1]. This can be particularly tricky in the volatile Web3 space, where token valuations and exit opportunities are closely tied to broader crypto market cycles.

While closed-end funds may deliver higher returns on deployed capital compared to evergreen funds – thanks to their ability to remain fully invested in high-risk, high-reward assets without liquidity reserves [6] – investors trade off flexibility in both capital deployment and reinvestment timing.

Liquidity Comparison: Access, Redemptions, and Lock-Up Periods

Liquidity Features: Evergreen vs Closed-End Funds

For institutional investors navigating the Web3 space, understanding liquidity features is critical for managing both capital deployment and risk. Closed-end funds come with a fixed lock-up period of 10–12 years, during which capital is inaccessible. Investors only see returns when portfolio assets are liquidated, usually through IPOs or acquisitions.

"The inherent lock-up [of closed-end funds] protects the fund from being forced to sell assets prematurely due to investor redemptions, enabling more strategic and potentially profitable timing of exits." – Alex Da Costa, Prime Quadrant [9]

Evergreen funds, on the other hand, offer more flexibility. Investors can request withdrawals, but they must adhere to notice periods – typically 60 to 90 days. To prevent destabilizing outflows, fund managers often enforce redemption gates, capping withdrawals at 5% to 25% of the fund’s net asset value (NAV) [3][4].

However, liquidity in evergreen funds isn’t always guaranteed, especially during market turbulence. Morgan Stanley Investment Management highlights this concern:

"Semi-liquid is different than liquid, and liquidity is not guaranteed during times of market stress." [3]

A clear example of this risk is the 2023 Wildermuth Fund crisis. Persistent redemption requests combined with poor performance forced the fund to suspend withdrawals, exposing the challenges of balancing illiquid assets with investor demands [5].

Another key difference lies in their approach to capital deployment. Closed-end funds use a gradual drawdown model, calling capital over 3 to 5 years. Evergreen funds, by contrast, deploy capital immediately while maintaining a cash reserve – usually 10% to 20% of the fund’s NAV – to accommodate redemptions. However, this reserve can lead to "cash drag", potentially dampening returns during strong market periods.

| Feature | Closed-End Funds | Evergreen Funds |

|---|---|---|

| Fund Term | Fixed term (10–12 years)[9] | Perpetual (no end date)[3] |

| Lock-up Period | Full fund duration | Subject to notice periods |

| Redemption Frequency | None until fund liquidation | Monthly or quarterly[3] |

| Notice Period | N/A | Typically 60–90 days[4] |

| Redemption Limits | None | Gates (5%–25% of NAV)[3][4] |

| Capital Deployment | Drawdowns over 3–5 years[9] | Immediate full deployment[3] |

| Minimum Investment | Often $5 million+[9] | As low as $25,000[3] |

Reinvestment Comparison: Capital Recycling and Deployment

How funds handle reinvestment plays a crucial role in shaping long-term returns, especially in the fast-paced Web3 markets where timing and compounding are key. Evergreen funds recycle capital from exits directly into new investments, ensuring consistent market exposure and enabling compounding. This approach aligns well with the liquidity profiles discussed earlier.

On the other hand, closed-end funds distribute profits to investors upon exit rather than reinvesting them within the fund. This creates what’s known as "reinvestment risk", where investors must independently seek new opportunities to maintain market exposure. These funds typically operate on a fixed timeline – usually 10 to 12 years – with capital being drawn down in stages during the first 3 to 5 years.

"The distinguishing feature of this fund type is that once a portfolio company exits the capital is permitted to be reinvested into another investment opportunity as opposed to being distributed out to investors."

– Max Fleitmann, Founder, VC Stack

An example of this shift is Sequoia Capital‘s decision in October 2021 to transition its U.S. and Europe operations to an evergreen structure. By prioritizing ongoing reinvestment over forced distributions, they aimed to sustain compounding growth – a critical strategy in volatile Web3 markets.

Deployment Dynamics

Capital deployment also varies significantly between these two models. Evergreen funds invest capital immediately upon subscription, providing investors with day-one exposure to the portfolio. In contrast, closed-end funds deploy capital incrementally over 3 to 5 years, which can leave committed capital idle for a time.

One of the key advantages of evergreen funds is their ability to avoid the J-curve effect. Closed-end funds often experience early negative returns due to management fees and delayed capital deployment. Evergreen funds bypass this by investing upfront into an already diversified portfolio. According to Long Angle research, an evergreen fund fully deployed from the start requires just a 10% annualized return to achieve a 2.1x multiple on invested capital over eight years. In comparison, a closed-end fund with staggered capital calls would need a 16% internal rate of return to reach the same outcome.

"Full upfront deployment with evergreens allows compounding to begin on day one. This means evergreen funds require lower annualized returns on deployed capital to achieve the same multiple on invested capital (MOIC) as closed-end funds."

– Chris Bendtsen, Author, Long Angle

Challenges of Evergreen Funds

Despite their advantages, evergreen funds face a unique hurdle: cash drag. To accommodate redemptions, these funds typically hold 10% to 20% of their assets in cash or liquid securities, which can dilute returns during strong market periods. Closed-end funds, by contrast, avoid this issue as they remain fully invested until the fund winds down.

Reinvestment Approaches: Evergreen vs Closed-End Funds

| Feature | Evergreen Funds | Closed-End Funds |

|---|---|---|

| Reinvestment Strategy | Recycles distributions into new investments | Returns capital to investors upon exit |

| Capital Deployment | Fully deployed immediately | Staggered over 3–5 years |

| J-Curve Effect | Minimal; compounding starts immediately | More pronounced; early returns often negative |

| Distribution Handling | Proceeds reinvested for compounding | Profits distributed to investors |

| Exposure Management | Maintains continuous market exposure | Market exposure decreases as the fund winds down |

| Cash Management | May face cash drag due to liquidity reserves | Avoids cash drag until capital calls |

| Investment Horizon | Indefinite or perpetual | Fixed, typically 10–12 years |

Benefits and Drawbacks for Web3 Institutional Investors

When it comes to Web3 investments, institutional investors face a key decision: evergreen funds or closed-end funds? The choice boils down to balancing flexibility with structure and liquidity with potential returns. Each option has its own set of strengths and challenges, shaping how investors approach the dynamic blockchain market.

Evergreen funds provide ongoing access and simplified processes. Investors can join or exit quarterly or semi-annually, making these funds ideal for adapting to the fast-changing Web3 landscape. Tax reporting is straightforward, using Form 1099, and capital is deployed immediately, ensuring exposure to market opportunities from day one. However, these funds must maintain 10% to 20% cash reserves to handle redemptions, which can weigh on performance during crypto bull runs. Additionally, during market downturns, their net asset value might not fully reflect real-time conditions, potentially disadvantaging those who remain invested. On the other hand, closed-end funds come with strict timelines and limited liquidity.

"The structures work best where cash flows are observable and valuation can be updated frequently… They are ill-suited to highly binary, long-duration strategies like early-stage venture." – Nick Jones, Practitioner [1]

Closed-end funds, by contrast, emphasize discipline and long-term commitment. With a fixed 10–12-year lifecycle, they shield early-stage Web3 projects from the pressures of premature liquidation caused by redemption demands. All capital is invested without liquidity buffers, allowing investors to capture the full illiquidity premium associated with long-term blockchain ventures. Capital is only called when specific investment opportunities arise. However, this structure comes with drawbacks: investors are locked in until the fund concludes, and tax reporting is more complex, often requiring multi-state K-1 forms.

Here’s a side-by-side look at how these two fund structures compare:

Benefits and Drawbacks: Evergreen vs Closed-End Funds

| Feature | Evergreen Funds | Closed-End Funds |

|---|---|---|

| Flexibility | Perpetual life with ongoing subscriptions and redemptions | Fixed 10–12 year lifecycle with predefined exit schedules |

| Liquidity Buffers | Required; 10–20% cash reserves create performance drag | Not required; capital fully deployed into illiquid assets |

| Illiquidity Premium | Marginally lower due to liquidity sleeves and cash drag | Higher; fully invested in high-return private assets |

| Investment Discipline | Risk of over-deployment if fundraising outpaces deal flow | High; capital called only for specific acquisitions |

| Web3 Fit | Best for decentralized infrastructure with observable cash flows | Best for early-stage venture capital and token projects |

| Tax Reporting | Simplified (Form 1099) | Complex (Multi-state K-1s) |

Both options have their place in the Web3 investment ecosystem, depending on the investor’s goals, risk tolerance, and time horizon.

How to Align Fund Selection with Web3 Investment Goals

When it comes to Web3 investments, aligning your fund structure with your specific goals can make all the difference. Liquidity and reinvestment timing aren’t just details – they’re central to how well your investments perform over time. Matching these factors to your timeline is a critical step.

Choosing the Right Fund Structure: If you’re investing in early-stage Web3 protocols with long development cycles, a closed-end fund with a 10 to 12-year term is often a better fit. This structure helps avoid the pressure to liquidate prematurely due to redemption demands[9]. On the flip side, institutional investors focusing on Web3 infrastructure or private credit might lean toward evergreen funds. Why? These funds allow for immediate capital deployment and automatic reinvestment, which means returns start accruing from day one. Unlike closed-end funds with gradual capital calls, evergreen funds can create a "compounding advantage." For example, an evergreen fund needs just a 10% annualized return to achieve a 2.1x multiple on invested capital over eight years. In contrast, a closed-end fund would need a 16% internal rate of return (IRR) to reach the same outcome[6].

"Evergreen funds are not simply ‘open-ended PE funds.’ They are distinct operating models with specific liquidity, valuation, and governance disciplines designed to balance long-term assets with periodic investor liquidity." – Nick Jones, Evergreen Funds Portal[1]

Planning for Liquidity: Liquidity planning is another key consideration. If you need regular access to capital for rebalancing or meeting obligations, evergreen funds offer flexibility, typically requiring just 60 to 90 days’ notice for withdrawals[4]. However, it’s important to note that these funds often have redemption gates, which limit net outflows to 5% to 10% of NAV per period. While these gates can protect the fund during volatile markets, they may also restrict access when you need it most[1]. This trade-off between flexibility and protection is something to weigh carefully.

Valuation Integrity Matters: Beyond liquidity, ensuring accurate valuations is essential for managing Web3 asset exposure. Evergreen funds require monthly or quarterly NAV calculations, but blockchain investments often lack clear market prices. Without strong valuation controls, there’s a risk of poor decision-making, especially during downturns[1]. To address this, fund managers might turn to AI-driven or third-party valuation models to reduce subjectivity and improve accuracy[10]. For closed-end funds, performance fees tied to realized profits offer another layer of alignment, compared to evergreen structures that may charge fees based on unrealized gains[9].

Choosing the right fund structure and planning for liquidity and valuation are all about ensuring your Web3 investments align with your broader goals. Each decision shapes your portfolio’s ability to grow and adapt in this dynamic space.

Conclusion

When deciding between evergreen funds and closed-end funds, it all comes down to your investment timeline and strategy. Evergreen funds stand out for immediate capital deployment and automatic reinvestment, creating a compounding effect over time. They also provide periodic liquidity windows, which is a big plus for some investors. However, they come with trade-offs like redemption gates that limit outflows to 5–10% of NAV, cash reserves that may underperform during bull markets, and challenges in valuing illiquid Web3 assets.

Closed-end funds, on the other hand, lock capital for 10–12 years, ensuring stability and protecting managers from forced asset sales during downturns. This structure aligns well with early-stage Web3 ventures that require patience to reach maturity. But there’s a catch: investors have to deal with the J-curve effect, and capital often remains idle during the initial 3–5 year drawdown period.

The key is to align the fund structure with your goals and risk tolerance. For backing early-stage protocols with binary outcomes and long development timelines, closed-end funds offer the stability and long-term focus required. Meanwhile, for Web3 infrastructure or yield-generating strategies with steady cash flows, evergreen funds provide the flexibility and compounding benefits that can amplify returns. As Nick Jones from Evergreen Funds Portal explains:

"The structures work best where cash flows are observable and valuation can be updated frequently… They are ill-suited to highly binary, long-duration strategies like early-stage venture."

Both fund types play important roles in the Web3 investment landscape. With evergreen funds projected to grow from 5% to 20% of total AUM over the next decade[5], and about $700 billion already allocated through semi-liquid vehicles[5], the decision between these models will continue to shape how capital flows into blockchain ecosystems. Matching your liquidity needs with the right fund structure is key to ensuring efficient capital deployment and achieving optimal returns in the Web3 space.

FAQs

How do redemption gates affect my ability to withdraw?

Redemption gates are mechanisms that temporarily limit or postpone withdrawals when there’s a surge in demand or during periods of market stress. Their purpose is to help manage a fund’s liquidity, maintain stability, and ensure the fund can continue to meet its long-term goals while safeguarding the interests of its investors.

What’s the tax reporting difference (1099 vs K-1) for investors?

The key distinction comes down to the tax forms investors are issued. If you’re investing in a closed-end fund, you’ll likely receive a Schedule K-1, which requires detailed reporting of income and deductions. This can make tax compliance more complicated. On the other hand, investors in evergreen funds typically get a Form 1099, which focuses on straightforward income types like dividends and interest. For U.S. investors, this simplifies the tax reporting process significantly. However, it’s worth noting that K-1 forms can sometimes result in more complex tax liabilities.

How should I choose based on my Web3 strategy and timeline?

To determine the best fund structure for your Web3 strategy, think about your liquidity requirements and how long you plan to invest.

Closed-end funds are ideal for long-term commitments. They typically have fixed lifecycles ranging from 7 to 15 years and focus on investments that benefit from illiquidity premiums. If you’re aiming for higher returns over an extended period and can lock in your capital, this might be a good fit.

On the other hand, evergreen funds offer more flexibility. These funds allow for periodic liquidity and ongoing capital deployment, making them more adaptable to the ups and downs of Web3 markets. However, they can come with challenges, like managing liquidity and maintaining transparency.

Ultimately, your decision should align with your investment timeline, how much risk you’re comfortable with, and how accessible you need your funds to be.