Co-investment rights in private equity allow investors to directly participate in specific deals alongside General Partners (GPs), often at reduced or zero fees. This approach offers several advantages, including:

- Lower Fees: Avoid the traditional 2% management and 20% performance fee structure, saving millions over time.

- Direct Deal Access: Investors can selectively join high-quality, vetted opportunities, especially in emerging sectors like Web3 and blockchain.

- Higher Returns: Co-investments typically outperform traditional funds, with gross TVPI multiples averaging 2.7x compared to 2.2x for standard structures.

- Stronger Partnerships: Build closer relationships with fund managers and gain greater visibility into deal processes.

Web3 co-investments stand out for their focus on high-growth areas like DeFi, blockchain infrastructure, and private tokens. By 2030, 88% of institutional investors plan to allocate up to 20% of their portfolios to co-investments, reflecting the growing interest in this cost-efficient, targeted strategy. However, success requires fast decision-making, thorough due diligence, and clear governance terms.

Co-Investment Rights Fee Savings and Performance Benefits in Private Equity

How Co-Investment Rights Reduce Fees

Avoiding Management and Performance Fees

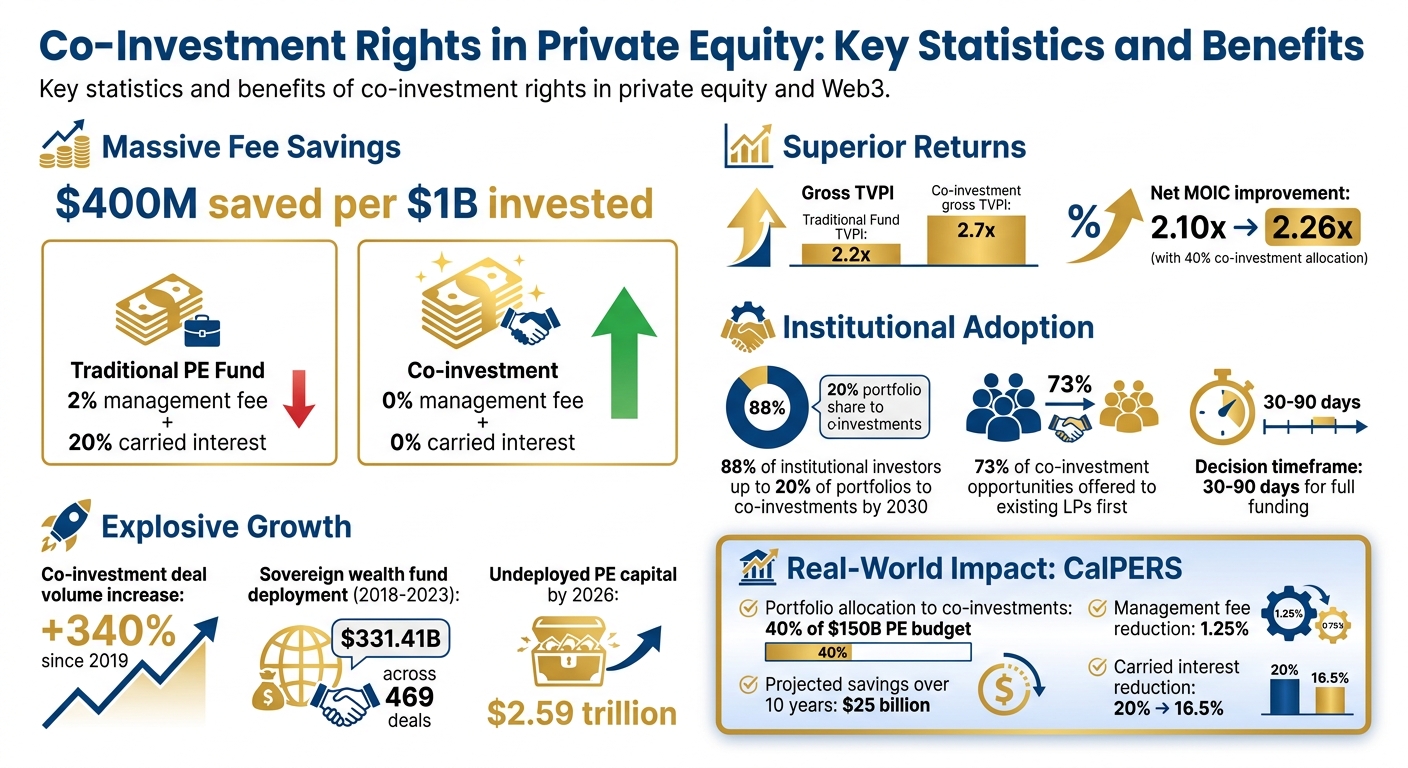

Co-investments offer a way to sidestep the hefty "two and twenty" fee structure that dominates traditional private equity – 2% annual management fees and 20% carried interest on profits [5]. By investing directly alongside a General Partner (GP), these fees are often eliminated. However, it’s worth noting that some GPs may impose indirect fees, such as monitoring, deal-support, or administrative charges, which can chip away at the overall savings [3].

"Although the use of co-investment structures can lead to reduced or no management and incentive fees, co-investors may still bear indirect fees, as the PE Fund and/or its affiliate or another third party will typically charge management fees or other fees and expenses to the Portco." – Myron Mallia-Dare, Partner, Dentons Canada LLP [3]

The savings are significant. For every $1 billion invested in co-investments instead of traditional private equity funds, investors can save around $400 million in management fees and carry over the lifetime of the investment [5]. Between 2018 and 2023, sovereign wealth funds poured $331.41 billion into 469 co-investment deals, showing how major institutional players are leveraging these cost advantages [1]. By cutting fees, co-investments not only reduce expenses but also allow more capital to be deployed directly, boosting overall returns.

Improving Capital Efficiency

Lower fees translate directly into higher net returns. For instance, allocating 40% of a portfolio to fee-free co-investments while keeping 60% in traditional funds can reduce annual management fees from 1.25% to 0.75% and carried interest from 20% to 16.5%. This adjustment increases the Net Multiple on Invested Capital (MOIC) from 2.10x to 2.26x [5].

"A GP that delivers a Net MOIC of 2.10x and offers co-invest is ‘equivalent’ to a GP who delivers a 2.26x Net MOIC with no co-invest." – Matthew Podlesak, Gather Capital [5]

In June 2024, the California Public Employees’ Retirement System (CalPERS) unveiled a plan to allocate 40% of its $150 billion private equity budget to co-investments. This move is expected to save the pension fund $25 billion in fees over the next decade by reducing management fees from 1.25% to 0.75% and carried interest from 20% to 16.5% [5].

This efficiency becomes even more critical in sectors like Web3, where maximizing capital deployment in high-potential projects is essential. With co-investments, 100% of the committed capital goes directly into project growth, avoiding the drain of administrative expenses [7].

Case Study: Fee Reduction in a Blockchain Project

A practical example of these savings can be seen in Pantera Capital‘s approach. In April 2025, Pantera launched Pantera Fund V, incorporating a co-investment structure tailored for blockchain assets [7]. Limited Partners (LPs) committing $25 million or more were granted rights to co-invest in at least 10% of every venture equity, private token, or special opportunity deal valued at over $10 million [7]. The co-investment structure had zero management fees and zero carried interest, offering LPs a cost-effective way to gain exposure to Pantera’s blockchain deal flow [7]. For smaller LPs, Pantera offered access at a reduced fee of roughly 0.1%, subject to availability [7].

Consider a $50 million blockchain infrastructure deal. An LP investing $5 million through the traditional fund structure would face annual management fees of about $100,000 (2% of $5 million), totaling $500,000 over five years. By contrast, investing the same $5 million as a co-investment would incur no management or performance fees. This setup allowed institutional investors to keep more of their capital working directly in blockchain projects, maximizing returns [7].

sbb-itb-c5fef17

Direct Access to High-Value Deals

Access to Exclusive Web3 Projects

Co-investment rights open the door to exclusive deals, giving investors the chance to participate in specific projects while benefiting from the same thorough due diligence, technical know-how, and industry connections as the lead institution [2][6].

In the Web3 space, these opportunities go beyond traditional equity investments. Co-investors can get involved in early-stage private tokens, locked-up treasury tokens, and decentralized infrastructure projects before they hit public markets [7]. Instead of accepting all fund offerings, investors can selectively focus on high-growth areas like DeFi protocols, the intersection of AI and Web3, or infrastructure tied to the Bitcoin ecosystem [2][6].

The numbers back up this trend: co-investment deal volume has skyrocketed by 340% since 2019 [6]. By 2026, private equity firms are expected to hold $2.59 trillion in undeployed capital, with many offering co-investment opportunities to qualified investors to keep their capital moving [6]. Notably, 73% of these opportunities are first offered to existing Limited Partners (LPs) before being made available to outside investors [6].

This targeted access doesn’t just create opportunities – it lays the foundation for deeper, more engaged partnerships with fund managers.

Building Relationships with Fund Managers

Co-investments pave the way for stronger, more collaborative relationships with fund managers. By investing directly alongside General Partners (GPs) in specific deals, LPs gain unparalleled insight into the decision-making and deal processes of these institutions [4]. This fosters a more active, trust-based partnership.

"Co-investments also allow LPs to strengthen their relationships with key sponsors, tighten alignment, gain enhanced visibility into deal processes and execute more control over portfolio management." – Timothy Jonas Clark, Partner, Akin Gump Strauss Hauer & Feld LLP [4]

Increasingly, institutions are formalizing co-investment access to deepen these partnerships. The approach is shifting from one-off deals to structured, ongoing partnerships where LPs can opt in or out of individual investments. Between 2018 and 2023, sovereign wealth funds deployed $331.41 billion across 469 co-investment deals, showcasing how major players use these rights to build lasting strategic relationships [1].

How Institutions Use Web3 Co-Investments

Institutions take these exclusive opportunities a step further by leveraging co-investment rights to gain influence and oversight in emerging Web3 projects. For example, institutional investors often negotiate for board seats or observer roles, providing them with direct involvement in the governance of portfolio companies [3]. This level of engagement is particularly impactful in Web3, where specialized expertise and strategic input can significantly shape a project’s success.

However, accessing these opportunities requires speed and expertise. Fund managers prioritize investors who can act quickly – co-investments typically require full funding within 30 to 90 days [6]. They also favor LPs with deep Web3 knowledge or those who helped source the deal [8]. Smaller private equity (PE) and venture capital (VC) firms, managing $50 million to $250 million, are often more open to offering co-investment rights to LPs capable of swift execution [6].

For investors without fast-moving due diligence teams, these opportunities can slip away. To counter this, institutional investors often maintain specialized teams equipped to conduct independent due diligence and make decisions quickly [8].

How to Use Co-Investment Rights Effectively

Conducting Thorough Due Diligence

Co-investment opportunities often come with tight deadlines – decisions are typically required within 48 to 72 hours [9]. To navigate this fast-paced environment, investors need to have their own evaluation teams ready, rather than relying solely on the lead General Partner’s (GP) research. Decide upfront whether you’ll take an active role in the portfolio company or invest passively through a Special Purpose Vehicle (SPV) managed by the lead sponsor.

Take a close look at the governance terms of the investment. Aim to negotiate observer rights so you can attend board meetings without voting privileges. Secure information rights to access key financial documents, such as budgets, forecasts, and regular financial statements. Review fee structures carefully, including any indirect charges, and push for minority approval rights to veto significant decisions, like taking on new debt or amending critical documents.

It’s also important to clarify exit strategies early in the process. Negotiate tag-along rights, which allow you to sell your stake alongside the lead investor, and review any drag-along provisions that could force you to sell. Additionally, seek preemptive rights to maintain your ownership percentage in future funding rounds.

Once your due diligence is in place, it’s time to think about how to balance your co-investment strategy across different opportunities.

Building a Diversified Co-Investment Portfolio

A balanced investment strategy often combines traditional "blind pool" funds with targeted co-investments. This approach provides broad diversification through funds while using co-investments to focus on high-conviction deals with lower fees [9]. For instance, in June 2024, CalPERS allocated a significant portion of its private equity budget to fee-free co-investments. This strategy allowed them to maintain broad exposure while also taking advantage of select, high-conviction opportunities [5].

"A GP that delivers a Net MOIC of 2.10x and offers co-invest is ‘equivalent’ to a GP who delivers a 2.26x Net MOIC with no co-invest." – Matthew Podlesak, Gather Capital [5]

Co-investments also allow for diversification across different regions and sectors. For example, you can build a portfolio that spans regulatory jurisdictions or focuses on blockchain strategies like DeFi, infrastructure, or gaming. This reduces the risk of being overly exposed to a single sector or region. However, be cautious of adverse selection – some deals may only be offered to fill funding gaps. Always ensure that the quality of co-investment opportunities aligns with the fund’s core investments [9].

After establishing a diversified portfolio, working with experienced partners can further strengthen your investment approach.

Working with Experienced Partners

The success of co-investments often hinges on choosing the right partners. Collaborate with established private equity or venture firms that have a proven track record of sourcing high-quality Web3 deals. When committing to a fund, negotiate your co-investment rights upfront and ensure they are documented in the Limited Partnership Agreement or through side letters.

Specialized platforms like Bestla VC focus on Web3 co-investment opportunities, particularly in areas like AI and blockchain, advanced cryptography, and decentralized infrastructure. Their expertise in digital finance and OTC market solutions can help investors navigate the complexities of early-stage blockchain projects while reducing counterparty risks. These partnerships not only simplify access to deals but also emphasize cost efficiency and effective capital use.

It’s also essential to build in-house analytical capabilities. Lead managers expect co-investors to conduct their own due diligence, so having a team that can independently assess risks is critical [10]. Standardizing Non-Disclosure Agreements to allow the sharing of due diligence materials with your team can make this process smoother.

"Successful co-investments require careful structuring and alignment between co-investors and PE Fund sponsors to create value for investors while allowing operational flexibility for the PE Fund." – Myron Mallia-Dare, Partner, Dentons Canada LLP [3]

Finally, ensure that exit terms are negotiated in advance. This includes securing tag-along rights to sell alongside the lead investor and understanding drag-along provisions that could impact your exit strategy. By doing so, you can ensure that your investment goals remain aligned throughout the lifecycle of the investment.

Conclusion: The Benefits of Co-Investment Rights

Key Takeaways for Investors

Co-investment rights are changing the dynamics of private equity. By avoiding the standard "2 and 20" fee structure, investors can boost their Net MOIC from 2.10x to 2.26x [5]. To put it simply, every $1 billion in co-investments saves $400 million in fees [5].

But it’s not just about saving money. Co-investments offer direct access to exclusive, high-quality opportunities. Instead of committing to a broad pool of assets, investors can focus on deals that align with their specific risk preferences and industry expertise. This targeted approach, combined with better transparency through information rights and governance participation, gives investors more control over their portfolios.

However, success doesn’t happen by chance. Investors need to be ready. This means developing strong internal analytical capabilities to act quickly, negotiating co-investment rights upfront in Limited Partnership Agreements, and ensuring clear governance terms. Elements like observer rights, tag-along provisions, and preemptive rights help maintain alignment with fund managers throughout the investment process. These strategies set the stage for success in an evolving Web3 investment environment.

The Future of Web3 and Blockchain Co-Investments

Looking ahead, the future of Web3 co-investments is filled with potential. The co-investment space is expanding rapidly, especially in Web3 and blockchain. 88% of Limited Partners plan to allocate up to 20% of their portfolios to co-investments between 2024 and 2030 [4]. This marks a major shift in how institutional capital is deployed in private markets, moving beyond traditional buyouts into areas like decentralized infrastructure and private credit platforms.

"Large institutional investors increasingly view co-investment access as a standard component of their relationship with private equity sponsors." – Akin Gump Strauss Hauer & Feld LLP [4]

As the market evolves, expect to see more tailored solutions, such as programmatic partnerships and separately managed accounts, enabling faster investment decisions. The gap between passive investors and active co-investors will grow, with the latter leveraging efficient diligence processes to secure top-tier Web3 deals. For those who build the right expertise and partnerships, co-investment rights are a game-changing way to cut costs while tapping into the future of blockchain innovation.

Co-Investments in Private Equity – Everything You Need to Know

FAQs

Who typically qualifies for co-investment rights?

Co-investment rights in private equity are generally offered to qualified investors, including accredited investors and limited partners. These individuals or entities meet particular financial and regulatory standards, giving them access to exclusive investment opportunities. Additionally, co-investments can often help reduce associated fees, making them an appealing option for those who qualify.

What hidden fees can still apply in co-investments?

When it comes to co-investments, hidden fees can be a concern. These might include indirect charges imposed by the private equity fund or its affiliates for overseeing the investment vehicle. What’s tricky is that these fees could still apply even if co-investors aren’t responsible for paying the main management fees. To avoid surprises, it’s crucial to thoroughly examine all fee structures and identify any potential extra costs.

What governance rights should I negotiate in a co-investment?

When negotiating co-investment governance rights, the goal is to ensure you have a say in decisions that impact your investment. Some key areas to focus on include:

- Preemptive rights: These allow you to maintain your ownership percentage by giving you the chance to participate in future funding rounds.

- Approval rights: These give you a voice in major decisions, such as company exits or significant structural changes.

- Information rights: These ensure you have access to crucial financial and operational data to stay informed about the company’s performance.

In some cases, investors also push for minority approval rights, which provide added protection by requiring their consent for critical matters. These rights help safeguard your interests and keep them aligned with the broader goals of the investment.