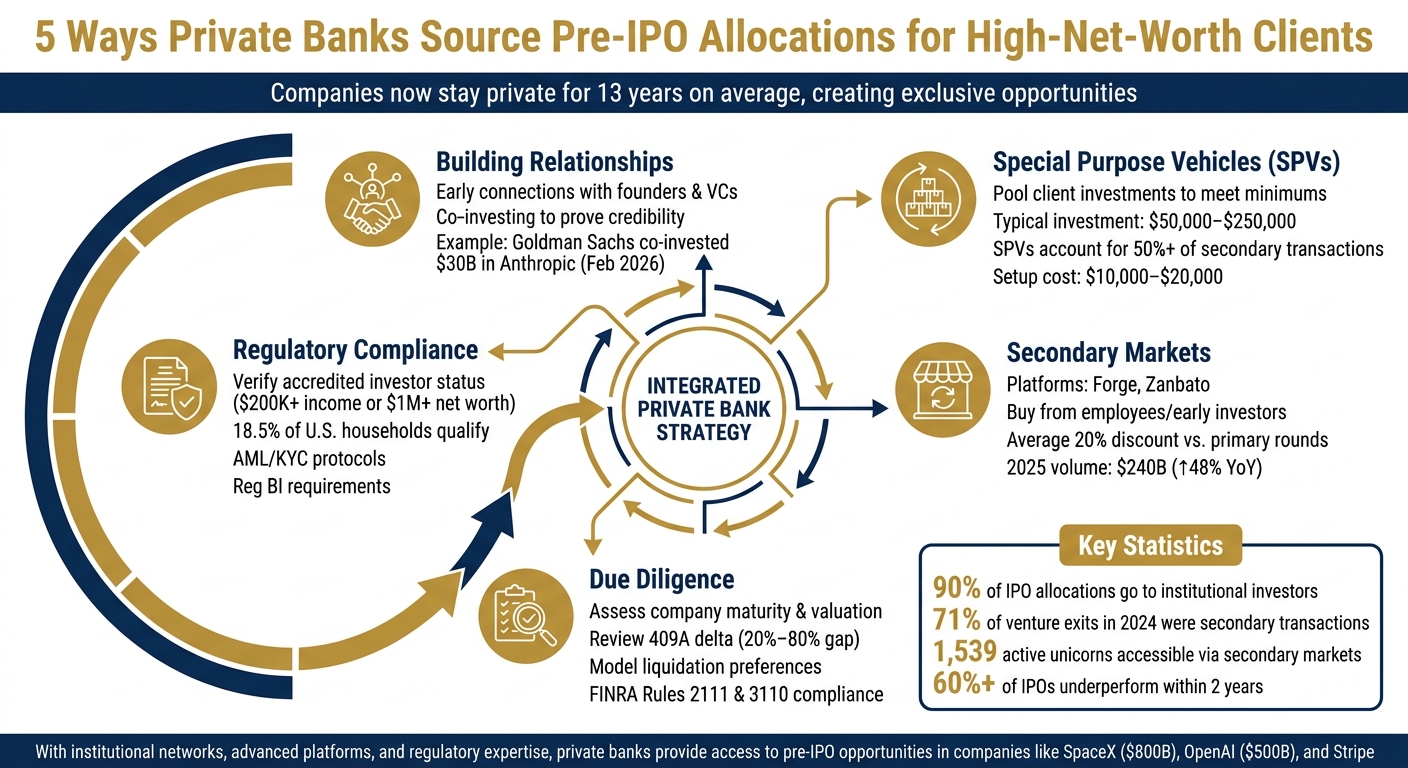

Private banks are helping high-net-worth clients gain access to Tier 1 pre-IPO allocations – exclusive investment opportunities in late-stage private companies like SpaceX, OpenAI, and Stripe. These investments allow clients to capture growth before IPOs, offering diversification and potential returns. Here’s how they do it:

- Building Relationships: Banks establish early connections with company founders and venture capital firms to secure allocations.

- Special Purpose Vehicles (SPVs): These pooled investment structures help clients meet high minimums (typically $50,000–$250,000) and simplify transactions.

- Secondary Markets: Platforms like Forge and Zanbato enable banks to buy shares from employees or early investors, often at discounted prices.

- Due Diligence: Banks assess company maturity, valuation, and risks to protect clients from overpaying or investing in problematic firms.

- Regulatory Compliance: Strict adherence to SEC rules ensures only accredited investors participate and reduces risks like fraud.

With companies staying private longer (13 years on average), private banks are leveraging institutional networks, advanced platforms, and regulatory expertise to provide access to these sought-after opportunities.

How Private Banks Source Pre-IPO Allocations: 5 Key Methods

Building Partnerships to Source Allocations

Working with Venture Capital Firms

Private banks often start building relationships with CEOs and founders well before any liquidity events occur. The key to success lies in establishing trust and visibility long before a Confidential Information Memorandum (CIM) is issued. By doing this groundwork early, private banks ensure they are positioned as a preferred partner when allocation opportunities arise.

"Firms win competitive processes by doing the work years before the CIM lands in their inbox: building CEO relationships, establishing credibility, and creating visibility long before a banker calls." – Nevin Raj, Co-founder, Grata [7]

To show their commitment, banks frequently co-invest alongside their wealth clients. For example, in February 2026, Goldman Sachs participated in a $30 billion funding round for Anthropic, an AI company valued at $350 billion. They co-invested through a Special Purpose Vehicle (SPV) alongside ultra-high-net-worth clients. Similarly, Morgan Stanley provided access to comparable opportunities using a flat placement fee structure [9].

Using SPVs allows banks to commit capital early and prove their institutional credibility. This strategy not only gives clients access to the same rigorous due diligence used for institutional investments but also strengthens the bank’s position in competitive allocation processes [9].

By building these early partnerships, private banks can leverage their institutional networks to secure broader allocation opportunities over time.

Institutional Relationships and Networks

Beyond direct partnerships with venture capital firms, private banks rely on institutional investors – such as private equity firms, hedge funds, and family offices – to access pre-IPO placements. These institutional investors often buy significant blocks of shares at a discount before companies go public. Private banks tap into these networks to gain entry into the "institutional tranche" of IPO offerings. Historically, institutional investors have received about 90% of total IPO allocations, leaving only 10% for retail investors [1].

Investment banks play a vital role here, acting as intermediaries between the "buy side" (PE and VC firms) and the "sell side" (companies seeking capital). Through these networks, private banks gain access to Tender Offers, which are company-approved opportunities for purchasing stock from existing shareholders. These offers have become more common as companies delay going public; the average age of a company at IPO has risen to 13 years as of 2025, compared to a median of 10 years in 2018 [3].

To simplify cap tables and avoid surpassing the 2,000-holder-of-record threshold (which triggers public reporting requirements), companies often prefer selling to a single institutional fund or SPV rather than multiple individual investors. This preference has driven the growth of the secondary market, where SPVs now account for more than 50% of all transactions [3]. Private banks with strong institutional ties can offer clients access to these exclusive opportunities, often at pricing comparable to what institutions receive.

How Bestla VC Supports Web3 Investment Partnerships

Bestla VC applies these strategies to the Web3 ecosystem, helping clients become long-term, active participants in blockchain projects. In this space, foundations and founders often prioritize strategic partnerships over purely financial bids. They seek collaborators who will hold tokens and actively engage with the network, rather than those focused solely on short-term profits.

"Foundations aren’t interested in the highest bid, but in partners who will hold tokens and participate in the network." – Nick Cote, CEO & Co-founder, SecondLane [10]

Bestla VC guides private banks in identifying opportunities within Web3 infrastructure, as current investments favor centralized platforms that bridge Web2 and Web3. For instance, in July 2025, crypto mining firm MARA raised $950 million through a Post-IPO convertible debt deal, showcasing how traditional financial tools are being used to support Web3 infrastructure. Around the same time, Mill City Ventures III secured $450 million via a PIPE round to build a Sui treasury, highlighting the growing role of traditional finance in blockchain ecosystems [8].

Bestla VC also helps banks analyze fund vintages to uncover liquidity opportunities. Many venture capital funds from the 2015–2017 period are nearing the end of their 10-year cycles and face pressure to deliver Distributions to Paid-In Capital (DPI). This creates openings for private banks to acquire allocations from these funds on favorable terms [10]. Additionally, Bestla VC aggregates smaller advisor stakes into larger blocks using SPV structures, making it easier for banks to participate in these deals [10].

sbb-itb-c5fef17

Using Secondary Market Platforms for Liquidity

Accessing Liquidity in the Secondary Market

Secondary markets have become a key tool for private banks managing pre-IPO allocations. With companies now staying private for an average of 13 years as of 2025, these platforms act as essential outlets for liquidity [6][11]. In 2025, the global secondary market hit $240 billion in transaction volume – a 48% jump from the previous year – with secondary transactions making up 71% of all venture exit value in 2024 [14].

Private banks typically rely on three methods to tap into these markets:

- Company-Sponsored Tender Offers: These allow banks to buy shares directly from employees or early investors, provided the company approves the transaction.

- Direct Secondary Purchases: Banks negotiate directly with shareholders seeking liquidity ahead of an IPO.

- Secondary Exchanges: Platforms like Forge and Zanbato connect buyers and sellers in a controlled environment, ensuring compliance [11].

These platforms provide access to 1,539 active unicorns, capturing opportunities that often remain hidden from public markets [6].

"The steepest part of the value creation curve now occurs entirely outside public market visibility, with venture capitalists and growth equity investors capturing returns that historically accrued to IPO participants." – AltStreet Briefing [6]

One major advantage is pricing. Secondary shares in Q1 2025 traded at an average 20% discount compared to their last primary funding round valuations [6]. For example, SpaceX reached an $800 billion valuation in a December 2025 secondary sale, while OpenAI hit $500 billion in October 2025 [14]. These discounts enable private banks to offer clients entry points that are often unavailable through primary funding rounds or public markets. This is particularly compelling given that over 60% of IPOs in the past decade underperformed market benchmarks within two years of listing [13].

Reducing Counterparty Risk

Ensuring secure transactions in secondary markets is a top priority. Unlike public market trades, which settle in a single day (T+1), secondary trades often take 6–8 weeks, creating more opportunities for complications [2]. One common hurdle is the Right of First Refusal (ROFR), where companies have a 30-day window to match a secondary offer and buy back the shares themselves. To navigate this, private banks often work directly with company transfer agents to verify share ownership and update cap tables before committing client funds [2].

Special Purpose Vehicles (SPVs) simplify the legal and administrative challenges in over half of secondary market deals [3]. These entities pool client capital into a single structure, shifting the administrative burden to a fund manager who handles the complexities of share acquisition and transfer. SPV setup costs range from $10,000 to $20,000, shared among participants, with annual management fees of 1%–2% and carried interest of 10%–20% on profits [2]. Additionally, transaction fees for secondary trades typically range from 3% to 5% of the deal value for both buyers and sellers [6].

For Web3 and digital asset allocations, private banks rely on institutional-grade custodians like BitGo, Anchorage, or Fireblocks to securely hold assets during and after transactions [12]. Strict Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols further reduce regulatory and reputational risks. Notably, a 2024 survey revealed that over 40% of family offices had made late-stage secondaries a core part of their portfolios, up from just 12% in 2018 [13]. These risk management practices lay the groundwork for more advanced over-the-counter (OTC) solutions.

Bestla VC’s OTC Market Solutions

Bestla VC builds on these risk management strategies with specialized OTC solutions tailored for Web3 transactions. The firm draws from five liquidity sources: foundations (treasuries), early venture capital investors, founders, employees, and advisors [10]. By coordinating directly with Web3 foundations or issuing companies, Bestla VC ensures transfer approvals and eliminates risks such as blacklisted tokens or voided transactions [10].

Through SPVs, Bestla VC aggregates smaller stakes into larger block trades, reducing market volatility from on-chain token sell-offs [10]. The firm also helps private banks time their acquisitions by analyzing fund vintages. For example, venture capital funds from 2015–2017 are nearing the end of their 10-year cycles, increasing pressure to deliver Distributions to Paid-In Capital (DPI). This creates opportunities for private banks to acquire allocations at favorable terms [10]. In fact, Europe recorded only 1,021 exits in 2025 – the lowest in a decade – further pressuring VCs to offload winning assets via secondary sales to meet obligations to limited partners [10].

"If you want to get liquidity early or access top-tier Web3 projects, you have to get comfortable in this secondary world. Mainstream adoption is picking up speed." – Omar-Shakeeb, CBDO, SecondLane [12]

Bestla VC also provides legal consultancy services to ensure compliance with U.S. regulations. This includes preparing essential documentation such as Private Placement Memorandums (PPMs), Operating Agreements, and Subscription Agreements [3]. By following this structured approach, private banks can offer clients access to sought-after Web3 companies at lower minimum investment levels compared to direct share purchases.

Due Diligence and Regulatory Compliance

Due Diligence Processes

Private banks face unique challenges when dealing with pre-IPO investments due to the limited transparency of private companies. Unlike public companies that provide quarterly earnings reports and SEC filings, private firms operate with far less disclosure. This forces banks to create their own frameworks to protect clients from overvalued or structurally problematic investments.

The process begins with assessing the company’s maturity. Banks need to determine if the company has consistent revenue, a proven product-market fit, and a clear path to liquidity – whether through an IPO, acquisition, or continued access to the secondary market. This step is critical, as many private companies delay liquidity events due to prolonged private tenures.

Valuation analysis is another key step. Banks compare the company’s internal valuations across various platforms and funds to account for discrepancies. For instance, secondary market transactions often occur at a discount compared to primary funding rounds. Additionally, they evaluate the 409A delta – the difference between common stock prices (traded in secondary markets) and preferred share prices (set by venture capital firms). This gap can range from 20% to 80%, meaning clients could unknowingly pay a premium for subordinated equity[2].

Structural reviews help clarify the actual equity stake being purchased. Banks examine whether clients are buying direct shares or participating through a Special Purpose Vehicle (SPV), which may involve extra fees and limited access to information. They also model liquidation preference waterfalls to predict how proceeds would be distributed in different exit scenarios. In moderate exits, preferred shareholders might claim over 75% of the proceeds, leaving common shareholders – often secondary market buyers – with far less than the headline valuation suggests[2].

Red flags such as overly optimistic projections, outdated financials, or companies unwilling to provide a Private Placement Memorandum (PPM) are scrutinized. Under FINRA Rules 2111 and 3110, broker-dealers are required to conduct a "reasonable investigation" and cannot rely solely on issuer-provided materials[17]. This obligation has grown more stringent, especially after a 34% increase in SEC examinations of broker-dealers in 2025, focusing on those serving accredited but non-institutional investors[16].

Once due diligence is complete, private banks must ensure compliance with evolving U.S. regulatory standards.

Meeting U.S. Regulatory Requirements

In addition to thorough due diligence, private banks must adhere to increasingly strict regulatory standards. Since 2026, regulators have shifted their focus from simply requiring documentation to demanding proof that banks’ procedures effectively identify bad actors[16].

The cornerstone of compliance is verifying accredited investor status. Under Regulation D, banks must confirm that clients meet SEC income or net worth thresholds. Rule 506(c) requires banks to take reasonable steps to verify this status, such as reviewing tax returns showing $200,000+ in individual income or $300,000+ for joint income, or examining bank statements proving a net worth of $1 million+ (excluding the primary residence). Although Rule 506(b) allows self-certification, most private fund offerings (90–95%) still rely on this less stringent standard[15]. By early 2026, about 18.5% of U.S. households qualified as accredited investors[2]. The SEC has also broadened the definition to include individuals holding FINRA Series 7, 65, or 82 licenses, acknowledging professional expertise beyond wealth[15][2].

To streamline compliance, banks increasingly use third-party verification services. These services, often provided by CPAs or attorneys, cost between $50 and $150 per verification and typically take 24–48 hours to complete. They also help protect client privacy and reduce friction[15].

Anti-Money Laundering (AML) compliance has also evolved. Banks must verify the source of wealth for first-time investors with investments exceeding $500,000 and identify the beneficial owners of LLCs or trusts[16]. According to Jeff Barnes, CEO of Angel Investors Network:

"AML compliance is moving from documentation to demonstration. You need to prove your procedures would actually catch bad actors, not just that you have procedures"[16].

Regulation Best Interest (Reg BI) adds another layer of scrutiny. Banks must demonstrate that pre-IPO recommendations align with the client’s best interests by considering their overall portfolio and concentration risks. Regulators now interpret "best execution" to mean achieving the best overall outcome, requiring banks to document why a specific pre-IPO deal was chosen over similar opportunities and disclose all forms of compensation, direct or indirect[16]. Maintaining a "thinking" file that shows multiple comparable options were evaluated can help banks meet these requirements during audits[16].

Another challenge is navigating the Right of First Refusal (ROFR) process. This 30–60 day period allows the issuing company or existing investors to claim the negotiated allocation, creating significant execution risk during the 6–8 week settlement period for private securities[2]. To mitigate these risks, banks often rely on third-party escrow services, which ensure funds are only released once the transfer agent updates the cap table[2].

These robust processes help private banks manage the complexities of pre-IPO investments while safeguarding their high-net-worth clients.

"The regulatory environment isn’t making private capital markets harder. It’s making them more professional."

– Jeff Barnes, CEO, Angel Investors Network[16]

Securing Allocations in Web3 and Blockchain

Opportunities in Web3

Private banks, traditionally focused on pre-IPO strategies, are evolving to keep pace with the rapidly growing Web3 and blockchain sectors. Unlike conventional software companies with steady revenue streams, Web3 startups often blend equity and token models, presenting both opportunities and unique challenges for investors.

The potential in this space is clear. Take ConsenSys, for example – the creator of MetaMask. Between 2019 and 2021, its revenue soared from $52 million to $218 million, with its user base exceeding 30 million by April 2026. This growth fueled a jump in valuation from $3.2 billion in late 2021 to $7 billion by March 2022, following a $650 million Series D funding round[18].

"We’re giving people the keys to Web3"

– Joseph Lubin, Co-Founder and CEO, ConsenSys[18]

To identify promising opportunities, private banks are turning to platforms like Harmonic, PitchBook, and VCBacked. These tools help track team developments, product launches, and early-stage metrics like developer retention and on-chain activity. However, about 60–70% of the best deals still come through warm introductions, often from portfolio founders or co-investors[19][10]. Banks also monitor accelerators like Y Combinator, which has produced over 80 unicorns, to tap into a curated pipeline of Web3 startups[19].

Another innovative strategy involves examining liquidity pools to spot "distressed" sellers. These are often venture funds from 2015–2017 nearing the end of their lifecycle and under pressure to deliver returns to Limited Partners[10].

"In private markets, who is selling matters as much as what they are selling"

– Nick Cote, CEO and Co-founder, SecondLane[10]

On the regulatory front, significant progress has been made. In March 2026, the SEC and CFTC signed a Memorandum of Understanding to align digital asset policies[20]. Additionally, the SEC launched "Project Crypto" in July 2025 to modernize securities laws and bring financial markets on-chain[20].

These data-driven and regulatory-backed strategies are shaping how private banks approach blockchain investments, setting the stage for firms like Bestla VC to lead with specialized expertise.

Bestla VC’s Blockchain Investment Expertise

Bestla VC has developed a tailored approach to blockchain investments, focusing on areas like AI integration, advanced cryptography, and decentralized infrastructure. By prioritizing practical applications and sustainable business models, the firm helps private banks separate high-potential projects from speculative ventures.

A standout feature of Bestla VC’s strategy is its ability to analyze on-chain activity and developer retention. This ensures that any potential investments are backed by solid blockchain data, adding an extra layer of confidence to their evaluations[10].

The firm also addresses execution risks in Web3 transactions through OTC market solutions. These solutions help navigate the complexities of extended ROFR (Right of First Refusal) periods and secure issuer approvals, ensuring that allocations are successfully finalized[2][10].

Bestla VC places a strong emphasis on long-term capital alignment. In the Web3 space, founders increasingly favor partners who hold tokens and actively participate in their networks rather than those focused solely on financial returns[10]. This approach aligns well with a broader shift in the sector, where investors are moving back to equity-based investments that offer traditional legal protections and tangible ownership[10].

Case Studies of Private Bank Allocations

Case Study: A High-Growth Web3 Startup

In February 2023, Goldman Sachs introduced a specialized investment option for its private wealth clients, allowing them to participate in a $4 billion fundraising round for Stripe, the fintech leader. To qualify, clients needed at least $10 million in assets. Acting as a fiduciary, Goldman Sachs co-invested with its clients, granting them access typically reserved for institutional investors. This allocation enabled Stripe to address critical financial needs, such as paying out restricted stock units (RSUs) to long-serving employees and covering related tax expenses[21].

Fast forward to April 2026, and another notable example emerged. OpenAI raised over $3 billion from individual investors through private banking channels, as part of a massive $122 billion funding round that valued the company at $852 billion. For the first time, OpenAI expanded participation beyond traditional venture capital firms, allowing private banks to allocate shares to their affluent clients. This represented a significant change in how large funding rounds incorporate individual investor capital[4].

"Private wealth is a real power alley for us, and those continue to be good sources of funding."

– Julian Salisbury, Global Asset Management Head, Goldman Sachs[21]

These examples shed light on the execution strategies used and reveal key insights into managing fee structures and timing in pre-IPO allocations.

Lessons from Blockchain Allocations

These case studies also highlight the importance of structuring allocations strategically while addressing regulatory and operational challenges in bank-driven deals.

Private banks have realized that regulatory compliance plays a vital role in building trust when it comes to Web3 allocations. Companies preparing for IPOs or formal disclosures – such as Circle and Coinbase – are more likely to attract institutional partnerships and sovereign wealth fund investments, which collectively amount to roughly $13 trillion globally[5].

The fee structures in these deals vary widely. For example, Goldman Sachs charged a management fee along with carried interest, whereas Morgan Stanley opted for lower placement fees[9].

Timing and infrastructure are equally critical. When JPMorgan integrated its stake in Zanbato, it significantly improved deal execution speed. As a result, the bank’s order flow from trading counterparties doubled every month for six consecutive months, showcasing the growing demand for private market access facilitated by banks[22].

"One of the things we say in the private market is that time is the enemy of every deal. Zanbato creates efficiency in execution which hopefully decreases the time it takes to get a deal closed."

– Andrew Tuthill, Global Head of Private Market Equities, JPMorgan[22]

Another key takeaway has been the shift from tokens to equity. Token unlock events often lead to substantial price drops – 90% of these events cause downward pressure, with an average 25% decline during team token unlocks. In contrast, equity structures provide traditional legal protections and tangible ownership rights, making them increasingly appealing to institutional investors[5].

These lessons emphasize the importance of strategic partnerships, strong compliance measures, and efficient execution in delivering premium pre-IPO opportunities to high-net-worth clients.

Strategies for High-Net-Worth Client Access

Matching Opportunities to Client Needs

Private banks take a highly personalized approach when allocating pre-IPO opportunities, tailoring them to align with each client’s financial profile. Allocations often depend on the client’s total assets and their contribution to the bank’s revenue, with long-standing relationships often receiving priority treatment[1]. For instance, a client with $70 million in assets is likely to access different opportunities than a client with $20 million.

For smaller allocations, banks frequently use SPVs (special purpose vehicles) to pool funds, while ultra-high-net-worth clients seeking cap table rights often prefer direct share purchases[2][3]. Banks also educate clients on the "409A delta", which highlights the pricing gap between secondary common shares and venture capital-preferred shares[2]. This tailored approach ensures that clients receive high-value, exclusive opportunities that align with their financial goals.

A recent example illustrates this strategy in action: In February 2024, Goldman Sachs and Morgan Stanley secured allocations in Anthropic’s $30 billion funding round. Goldman Sachs offered the opportunity to clients averaging $70 million in assets through an SPV, charging a 1.25% management fee and 17.5% carry. Meanwhile, Morgan Stanley targeted clients with $20 million or more in assets, offering a flat 1% placement fee with no carry[9].

Using Technology and Analytics

Tier 1 opportunities often close within 48 to 72 hours, making speed and efficiency essential. Private banks increasingly rely on technology platforms to automate tasks like subscription documents, capital calls, and distribution processing. These advancements reduce administrative time by as much as 70% to 80%[23]. Automation also allows banks to pool smaller client commitments (e.g., $100,000–$250,000) into a single tranche that meets institutional minimums, typically ranging from $5 million to $25 million[23].

Digital tools, such as "Vaults" and dashboards, provide real-time pricing data and help manage cap tables. These platforms also track curated "Venture 50" lists, which highlight high-priority investment opportunities[3]. Deals are categorized into two main types to match client risk profiles: "Growth Stage" investments, which offer predictable revenue and a 3 to 5-year holding period, and "Early Stage Moonshots", which involve higher risk and a 7 to 10-year holding period[23]. By leveraging these tools, banks can close deals in as little as 72 hours, compared to over five days with manual processes[23].

"The opportunity for us came about when we realized that us as wealth managers, we’re able to take that 25 mil US tranche, and then we just split it within all our client base."

– Antoine Chaume, Wealth Advisor, Assante Wealth Management[23]

These technological advancements streamline operations and enable banks to provide clients with access to exclusive, high-demand opportunities.

The Advantage of Bestla VC

Bestla VC excels at sourcing Tier 1 allocations in cutting-edge sectors like AI and Web3. With a focus on AI-driven Web3 strategies and blockchain infrastructure, Bestla VC’s expertise extends to secondary market investments and OTC solutions. This specialization allows private banks to tap into exclusive opportunities that are difficult to access elsewhere.

Pre-IPO Investing: Risks, Rewards, and Strategy

Conclusion

Securing Tier 1 pre-IPO allocations requires a mix of strategic partnerships, thorough due diligence, and leveraging advanced platforms. The most successful banks tap into five key liquidity pools: foundations, venture capital investors, founders, employees, and advisors [10].

Direct alignment with issuers is essential for gaining access to private markets. As Nick Cote, CEO & Co-founder of SecondLane, puts it:

"The issuer holds the keys to access, and access is everything on the private market" [10].

This principle is especially important in sectors like Web3 and blockchain, where foundations often manage transfer switches to reduce counterparty risk.

Timing also plays a crucial role. Private banks that closely track fund vintages gain an edge – venture capital funds from 2016–2017, for instance, are under mounting pressure to demonstrate Distributed to Paid-In Capital (DPI) as their 10-year lifecycles near completion [10]. This creates opportunities for banks to secure favorable terms for their clients. Take the Anthropic deal in February 2026 as an example, where a $350 billion valuation allowed for innovative fee structures to be applied [9].

Advanced technology platforms add another layer of efficiency. These platforms simplify subscription management and SPV structuring, enabling smaller stakes to be aggregated into institution-sized blocks [10].

In this dynamic environment, Bestla VC stands out with its expertise in AI-driven Web3 strategies and blockchain infrastructure. Its specialized focus on secondary market investments and OTC solutions makes it an invaluable partner for private banks seeking exclusive opportunities in emerging digital finance. By combining technical knowledge with strong networks, Bestla VC helps banks deliver unmatched pre-IPO opportunities to their high-net-worth clients.

FAQs

How do I qualify for Tier 1 pre-IPO allocations through a private bank?

To access Tier 1 pre-IPO allocations, certain financial requirements and banking relationships typically come into play. These opportunities are often reserved for high-net-worth individuals (HNWIs) or ultra-high-net-worth individuals (UHNWIs). Factors such as assets under management (AUM), a proven investment track record, and the capacity to commit significant capital are key elements banks evaluate when determining eligibility.

What’s the difference between buying pre-IPO shares via an SPV vs. direct shares?

Buying pre-IPO shares through a Special Purpose Vehicle (SPV) offers a different approach compared to purchasing direct shares. An SPV pools funds from multiple investors, making it easier to manage investments, spread risk across different holdings, and transfer shares. This structure is particularly appealing for those seeking a more streamlined process.

On the other hand, buying direct shares – whether through the company itself or private placements – demands more capital upfront, thorough due diligence, and navigating regulatory requirements. However, direct ownership provides a stronger level of control and a closer connection to the company.

SPVs often attract high-net-worth individuals due to their accessibility and the convenience they bring to investing in pre-IPO opportunities.

What are the biggest risks in pre-IPO secondary deals (ROFR, pricing, fees)?

The main risks in pre-IPO secondary deals revolve around Right of First Refusal (ROFR), pricing challenges, and fees.

- ROFR: This can complicate or delay transactions if existing shareholders decide to exercise their rights, potentially blocking or altering the deal.

- Pricing: Limited transparency and fluctuating valuations make it tough to determine fair pricing, increasing the risk of overpaying for shares.

- Fees: Platform charges and transaction costs can eat into potential returns, reducing the overall profitability of the investment.

To navigate these risks, conducting thorough due diligence and carefully assessing each of these factors is essential.