GP stakes investing is changing how institutions back fund managers. Instead of just investing in funds, they now buy minority ownership stakes (10%-30%) in management companies. This approach allows investors to earn from management fees and carried interest across all funds managed by the firm, not just one. It offers steady income and broad exposure, making it appealing for long-term growth.

Key takeaways:

- Why it’s popular: Stable income (7%-10% returns) and access to multiple funds.

- How it works: Investors buy a share of the GP’s revenue, not the funds themselves.

- Risks: Valuation volatility, dependence on key personnel, and tax complexities.

- Trends: Web3 growth is driving more deals, with GP transactions increasing by 40% from 2024 to 2025.

GP stakes are becoming a go-to strategy for institutions seeking diversified, recurring returns while partnering with top fund managers.

The Future of GP Stakes

sbb-itb-c5fef17

How GP Stake Transactions Work

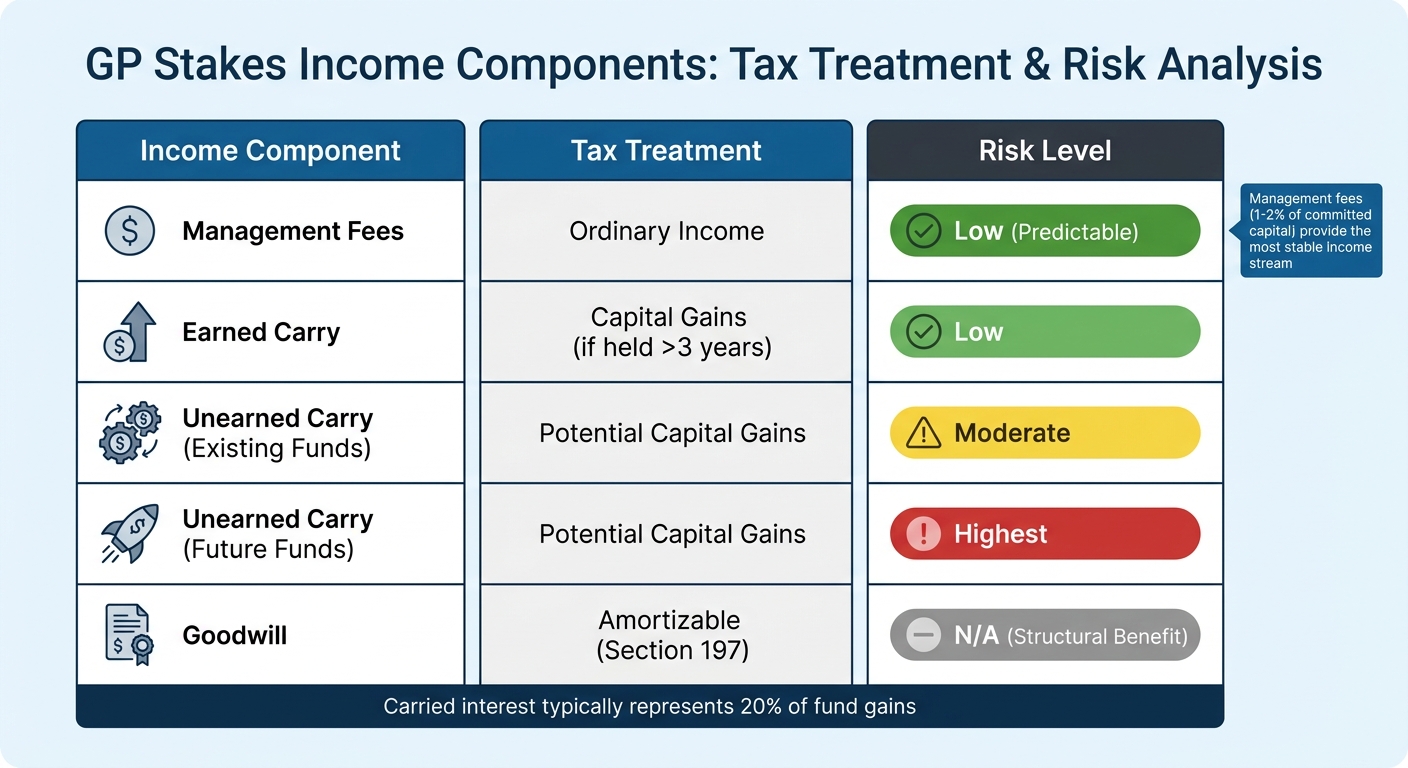

GP Stakes Income Components: Tax Treatment and Risk Levels

GP stake transactions involve purchasing a minority ownership position – typically around 20% – in a fund manager’s management company [5]. Unlike investing in a single fund, this approach gives buyers access to all revenue streams generated across the manager’s platform. The structure and pricing of these deals depend on how the firm’s assets are valued and how the agreement is tailored to meet the goals of both parties. The next section explains how these stakes are valued with precision.

How GP Stakes Are Valued

Valuation focuses on three main revenue streams: management fee profits, carried interest, and balance sheet returns from the GP’s own co-investments [7]. Management fees, which are typically 1% to 2% of committed capital, are considered the most stable and predictable income source, often referred to as the "bread and butter" of these deals [6].

Carried interest, which usually accounts for 20% of fund gains, is more complex. Investors assess carried interest across four risk tiers:

- Earned carry: Already realized and carries the lowest risk.

- Unearned carry from existing funds: Moderate risk.

- Unearned carry from uncommitted capital ("dry powder"): Higher risk.

- Unearned carry from future funds not yet raised: Highest risk [6].

Each tier is evaluated and priced based on its risk profile.

A significant portion of the purchase price often includes goodwill and intangibles. Structured properly, this goodwill can be amortized over 15 years under Section 197 of the U.S. tax code [6]. Additionally, the valuation considers the firm’s ability to raise future funds and expand into areas like private credit or infrastructure, often referred to as platform-level economics [3][8].

"Management fees = ordinary income; Future carried interest = potential capital gain; Goodwill = amortizable under Section 197."

This insight from PwC highlights how various revenue components are treated for tax and valuation purposes [6].

Once valuations are determined, the deal structures illustrate how capital is deployed and risks are managed.

Common Deal Structures

GP stake deals generally fall into two main categories. Secondary transactions provide liquidity to legacy partners or founders, often as part of succession planning. These deals allow buyers to receive a step-up in basis for tax purposes [6]. On the other hand, primary transactions involve injecting capital directly into the firm to support growth initiatives, such as launching new funds, expanding teams, or upgrading technology. These are typically structured as post-money valuations and do not include the tax step-up benefits.

Another emerging structure involves preferred equity and securitized assets, where buyers acquire specific income streams rather than permanent equity. In these deals, investors receive a priority share of cash flow until they achieve a target Internal Rate of Return (IRR) or Multiple on Invested Capital (MOIC) [6]. This approach offers distinct risk-return profiles and tax implications compared to traditional equity ownership.

For example, in October 2021, Blue Owl Capital acquired a minority stake in Oak Hill Advisors to expand its credit platform and diversify its alternative asset offerings [3]. Similarly, in 2023, Ares Management made a strategic investment in Crestline Investors, gaining exposure to specialized credit and opportunistic strategies [3].

| Income Component | Tax Treatment | Risk Level |

|---|---|---|

| Management Fees | Ordinary Income | Low (Predictable) |

| Earned Carry | Capital Gains (if held >3 years) | Low |

| Unearned Carry (Existing Funds) | Potential Capital Gains | Moderate |

| Unearned Carry (Future Funds) | Potential Capital Gains | Highest |

| Goodwill | Amortizable (Section 197) | N/A (Structural Benefit) |

Buyers must carefully analyze the tax impact of acquiring existing carry versus future carry, as these income streams can significantly influence overall returns [6]. Additionally, negotiating minority protections – such as board observer rights, information rights, and veto powers over key corporate decisions – is crucial to safeguard the investment, even without controlling ownership [3].

Why Institutional Investors Buy GP Stakes

Institutional investors are drawn to GP stakes for their ability to provide steady income and strategic access to the market. These investments generate reliable, recurring revenue through management fees, often locked in for a decade or longer [9]. This predictable income stream is particularly appealing to pension funds and insurance companies, which need to match long-term liabilities. Another key attraction is the ability of GP stakes to preserve capital, even during challenging market conditions.

But it’s not just about income stability. GP stakes also offer strategic perks. For instance, they grant priority access to co-investment opportunities – frequently with reduced or even zero fees – and ensure allocations in oversubscribed funds [1][4]. This means institutional investors can partner directly with top-performing managers without having to compete for limited fund capacity. The result? Enhanced portfolio performance through exclusive deal opportunities.

The diversification benefits are just as important. Unlike putting money into a single fund, investing in a GP stake spreads exposure across various funds, strategies, regions, and vintages [5][9]. This broad diversification typically yields returns of 7% to 10% initially, with the potential to climb into the mid-teens as the portfolio matures [1]. Reports from the market continue to show strong institutional confidence in this investment strategy [2].

Emerging sectors, such as Web3 and venture capital, add another layer of opportunity. For investors eyeing high-growth areas, GP stakes provide a way to partner with specialized managers. A notable example occurred in September 2025, when Hunter Point Capital and Temasek Holdings acquired a minority stake in Nuveen Private Capital. Temasek not only provided the capital for the deal but also committed to future fund investments [2]. This case highlights how GP stakes can support strategic growth and align long-term objectives.

The growing interest in GP stakes is reflected in market activity. By July 2024, deals targeting GPs had surged by 84% year-over-year, with 89 transactions announced or completed [1]. With the private capital industry projected to manage $21.6 trillion in assets by 2028 [9], GP stakes are becoming an essential part of institutional portfolios, offering both income stability and access to high-growth opportunities.

Risks and Due Diligence in GP Stakes Investing

Common Risks in GP Stake Investments

Investing in GP stakes comes with its own set of challenges, and understanding these risks is crucial for institutional investors. One of the primary concerns is valuation volatility. Management fees, which typically range from 1% to 2% of committed capital, provide a steady income stream. However, carried interest – often 20% of profits – can vary greatly depending on fund performance. This can lead to an unpredictable income profile, with returns fluctuating significantly from year to year [6][3].

Another key risk is the heavy reliance on key personnel. The value of a GP is closely tied to its founders and top investment professionals. If a star performer leaves or succession planning is inadequate, the investment could suffer [6][4]. This issue is especially pronounced in areas like Web3 and venture capital, where personal relationships and expertise are critical for deal flow.

Tax complications add another layer of complexity. Investors may face exposure to Effectively Connected Income (ECI), Unrelated Business Income Tax (UBIT), and state-level tax apportionment. Poor structuring can lead to "phantom income", where taxes are owed on earnings not yet received, or prevent the amortization of goodwill over the standard 15-year period [6].

"Tax is not just a line item – it’s an essential ingredient. Whether you’re structuring profit interests, allocating purchase price, or managing ECI exposure… even small tax oversights can spoil the meal." – PwC [6]

Regulatory scrutiny is also on the rise. The SEC has increased its focus on fee transparency and conflicts of interest, particularly when an investor holds both LP positions in a fund and GP equity [3][4]. The illiquidity of GP stakes further complicates matters, as these are long-term positions with virtually no secondary market [4]. Addressing these risks requires thorough and detailed due diligence.

What to Review During Due Diligence

Once the key risks are identified, conducting targeted due diligence becomes essential to protect the investment. GP stakes require a deep dive into both financial and operational aspects. Start by reviewing consolidated financial statements to validate Fee-Related Earnings (FRE) and Performance-Related Earnings (PRE). Since many privately held managers don’t have audited statements, it’s important to establish a clear connection between adjusted earnings and historical actuals [6].

Leadership continuity is another critical area. Evaluate succession plans, carry allocations, and retention incentives to ensure the firm’s long-term stability [6]. Tax exposure must also be assessed carefully. Model the after-tax yield while factoring in ECI, local tax leakage, and withholding obligations [6]. Structuring deals with tools like Section 754 step-up elections can also help by allowing the amortization of intangibles in secondary transactions [6].

Minority protections should be negotiated upfront. These include securing board observer rights, access to essential information, and veto power over major decisions such as launching new funds, GP restructurings, or the departure of key personnel [6][3]. Finally, assess the quality of LP relationships by examining the manager’s fundraising history, LP concentration, fee terms, and strategic market position. This ensures the business model can weather market cycles.

| Diligence Category | Key Review Items |

|---|---|

| Financials | Consolidated statements, FRE/PRE mix, bridge to historical actuals, distributable earnings |

| Tax | ECI risk, Section 754 step-up, state/local leakage, Section 1061 compliance |

| Legal/Governance | Entity structure, veto rights, board observer rights, buy-in/buy-out mechanics |

| Human Capital | Succession plans, next-gen leadership, carry allocation, retention incentives |

| Market/LP | Fundraising track record, LP concentration, fee terms, strategic market position |

Conclusion

GP stakes investing has transitioned from a niche strategy to a common choice for institutional investors seeking diversified returns [7]. By purchasing minority ownership stakes – usually ranging from 10% to 30% – in fund managers, investors tap into two key benefits: steady, recurring cash flow from management fees and capital growth potential from carried interest and equity value [7]. This combination generates what’s often referred to as "GP Alpha" – returns that go beyond those of traditional fund investments by sharing in a manager’s fee and equity upside [7].

For institutional investors, the appeal of GP stakes lies not just in cash flow but also in the strategic advantages they offer. These include priority access to co-investment opportunities and valuable insights into emerging sectors like digital assets [4][11]. Unlike traditional secondary funds, which eventually wind down after assets are realized, GP stakes benefit from a perpetual investment cycle. As managers raise new fund vintages, the portfolio is continually refreshed, ensuring ongoing value creation [7][10]. These aspects make GP stakes an attractive long-term strategy.

As highlighted by industry experts:

"By partnering directly with the managers themselves, these entities can deepen strategic relationships, secure advantaged access to deals, and capture a share of the economics across a manager’s entire platform." – Danielle Kline and Raegan Kennedy, Torys LLP [4]

However, success in GP stakes investing requires rigorous due diligence and well-structured minority protections [3]. With more investors directly participating in these transactions, confidence in this approach continues to grow [2].

The alignment between institutional capital and experienced fund managers, particularly in fast-evolving areas like Web3, sets the stage for lasting value creation. As asset management continues to transform, GP stakes remain a powerful tool for institutional investors aiming to achieve stable, diversified growth.

FAQs

How are GP stakes different from investing in a VC fund?

GP stakes and VC fund investments operate differently in both structure and focus. When you invest in a VC fund, you’re essentially purchasing limited partner (LP) interests. This gives you exposure to a diverse portfolio of startups. On the other hand, investing in GP stakes means acquiring a minority ownership in the management company itself. Instead of gaining direct access to the startups in the fund, GP stake investors benefit from the long-term economics of the management company, such as management fees and carried interest.

What should I look for when valuing a GP’s management fees and carry?

When evaluating a GP’s management fees and carried interest, focus on three main factors: stability of management fees, potential upside from carried interest, and growth opportunities within the GP’s business model. Stable management fees typically come from well-diversified portfolios backed by a strong performance history. Look at accrued carry as an indicator of long-term growth potential. Additionally, consider the GP’s capacity to raise new funds and increase assets under management to assess their future prospects.

What are the biggest tax and governance risks in GP stakes deals?

When it comes to GP stakes deals, two key risks often stand out: tax complications and governance challenges.

Tax issues typically arise from the way the investment is structured. If not handled carefully, these can lead to unexpected liabilities or inefficiencies, which can impact the overall return on investment. On the governance side, potential misaligned incentives or conflicts of interest between General Partners (GPs) and Limited Partners (LPs) can create friction. These misalignments might influence how decisions are made or how priorities are set within the partnership.

Because of these risks, it’s critical to thoroughly review the deal terms and ensure strategies are in place to align interests and avoid governance pitfalls.