When deciding between DeFi lending and money market funds in 2026, the choice boils down to yield, risk, and your comfort level with technology. Here’s the gist:

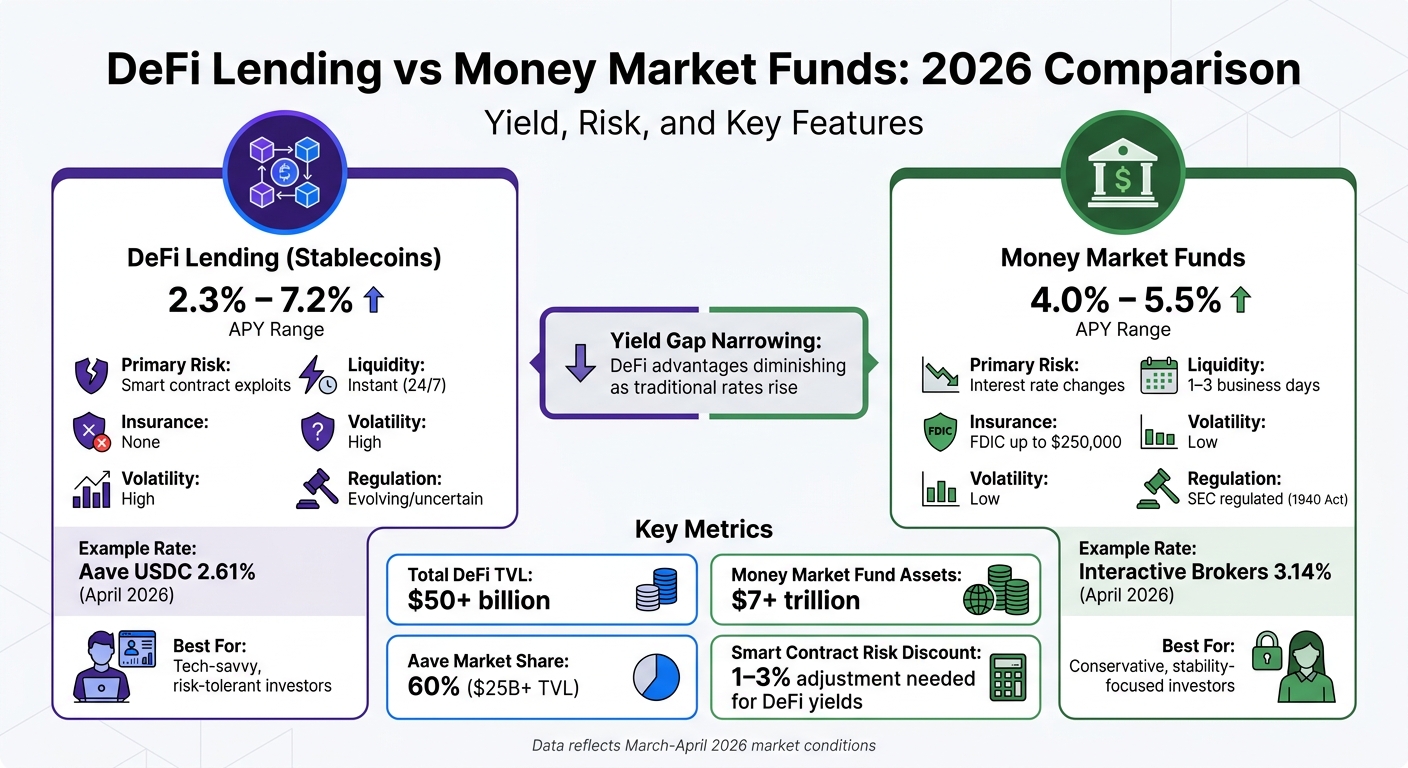

- DeFi lending uses blockchain-based smart contracts to offer yields ranging from 2.3% to 7.2% APY. It provides 24/7 liquidity and unique features like flash loans but comes with risks like smart contract exploits, liquidation penalties, and high volatility. Example: Aave‘s USDC supply APY was 2.61% in April 2026.

- Money market funds invest in short-term, high-quality debt instruments and offer 4.0% to 5.5% APY. They’re regulated, stable, and safer but lack the flexibility of DeFi. Example: Interactive Brokers paid 3.14% on idle cash in the same period.

Quick Comparison:

| Feature | DeFi Lending (Stablecoins) | Money Market Funds |

|---|---|---|

| APY Range | 2.3% – 7.2% | 4.0% – 5.5% |

| Primary Risk | Smart contract exploits | Interest rate changes |

| Liquidity | Instant | 1–3 business days |

| Insurance | None | FDIC (up to $250,000) |

| Volatility | High | Low |

DeFi works for tech-savvy, risk-tolerant investors seeking higher returns and flexibility. Money market funds suit those prioritizing safety and stability. Choose based on your goals and risk tolerance.

DeFi Lending vs Money Market Funds: Yield, Risk, and Features Comparison 2026

DeFi Lending Explained: Aave vs Compound for Beginners

sbb-itb-c5fef17

What Is DeFi Lending?

DeFi lending is a financial service in the world of decentralized finance that allows people to lend and borrow cryptocurrencies directly on a blockchain. It eliminates the need for banks or credit checks by using smart contracts – self-executing programs that handle everything from setting interest rates to liquidating collateral. These contracts automate the entire process, making it possible for someone in one part of the world to get a loan funded by someone on the other side of the globe, all within minutes and without traditional banking hours.

As of April 2026, DeFi lending protocols collectively manage over $50 billion in total value locked (TVL) [1]. Aave, the market leader, holds about 60% of this market with over $25 billion in TVL, while Compound manages approximately $2.64 billion [2]. Since its launch, Aave has facilitated more than $1 trillion in loans [1].

How DeFi Lending Works

DeFi lending relies on two key elements: liquidity pools and over-collateralization. Instead of direct transactions between lenders and borrowers, assets like USDC or ETH are deposited into liquidity pools managed by smart contracts. Borrowers then access funds from these pools by providing collateral.

To manage risk, borrowers must over-collateralize their loans – typically providing collateral worth at least 150% of the loan value to account for market volatility. For instance, borrowing $10,000 in USDC usually requires depositing about $15,000 in ETH. If the value of the collateral drops too much and the loan’s health factor hits 1.0, liquidators step in to seize the collateral, often with a penalty of 5–10% [5].

Interest rates are determined algorithmically based on the utilization ratio, which measures how much of the deposited assets are currently borrowed. As the utilization ratio increases, rates climb gradually until hitting an optimal level (usually 60–80%). Beyond this point, rates spike sharply to discourage excessive borrowing and ensure liquidity remains available.

Flash loans are another standout feature in DeFi lending. These are unsecured loans that must be borrowed and repaid within the same blockchain transaction. If repayment doesn’t happen, the transaction is reversed entirely. Flash loans are primarily used by traders for activities like arbitrage and liquidations, allowing them to borrow large sums without needing collateral.

Main Platforms and Applications

Several platforms dominate the DeFi lending space, each offering unique features and approaches.

Aave is the clear leader, managing over $25 billion in TVL as of April 2026 [1]. In March 2026, Aave introduced its V4 upgrade on Ethereum, featuring a "Hub-and-Spoke" architecture. This setup centralizes liquidity management while supporting independent lending markets tailored to specific risks. Operating on more than 14 blockchains, Aave offers tools like flash loans and Efficiency Mode (E-Mode), which increases borrowing power when the collateral and borrowed assets are closely correlated in price (e.g., stablecoins or ETH/stETH pairs). During this time, Aave’s native stablecoin, GHO, surpassed a $500 million market cap [1].

Compound, known for its straightforward design and predictable interest rates, manages around $2.64 billion in TVL [2]. It issues cTokens, such as cUSDC, which represent a user’s share of a lending pool and automatically accumulate interest. In March 2026, Compound DAO approved Proposals 553 and 554, removing COMP token incentives from ten markets across Ethereum, Linea, and OP Mainnet. This shift redirected resources toward key Ethereum markets and moved service provider payments to USDC, easing selling pressure on the COMP token [1].

Maple Finance takes a different approach by combining traditional finance with DeFi. It offers tokenized corporate loans and borrower pools verified through KYC processes. By early 2026, Maple Finance had $2.4 billion in active loans. The platform appeals to institutional investors looking to access corporate credit markets while enjoying the transparency of blockchain-based settlements.

What Are Money Market Funds?

Money market funds are investment pools that focus on short-term, high-quality debt instruments such as Treasury bills, certificates of deposit, and commercial paper. Their primary goal is to safeguard capital while offering yields that typically exceed those of standard bank savings accounts. As of January 31, 2026, U.S.-based money market funds managed over $7 trillion in assets collectively [12].

These funds are regulated under the Investment Company Act of 1940 and are overseen by the SEC. However, they are not insured by the FDIC, and the SIPC only offers protection against brokerage failures – not market losses [11].

To minimize risk, money market funds operate under strict regulations. Their portfolios must maintain a weighted average maturity of 60 days or less. Additionally, at least 25% of assets must be held in daily liquid assets, and 50% in weekly liquid assets [11]. To limit exposure to any single issuer, these funds generally avoid allocating more than 5% of their assets to one entity, with the exception of government securities.

Core Features of Money Market Funds

Money market funds primarily invest in short-term debt instruments. Their portfolios often include U.S. Treasuries, commercial paper from well-established companies, certificates of deposit issued by banks, and repurchase agreements. Government money market funds, which invest 99.5% of their assets in cash and government-backed securities, are considered the safest option. Meanwhile, prime funds include corporate debt and commercial paper, which offer higher yields but come with added risk [10][11].

Returns from money market funds are driven by yields rather than capital gains. These yields are closely tied to Federal Reserve policies and prevailing interest rates. The "7-day SEC yield" is the industry standard for measuring returns – an annualized figure based on average payouts over a one-week period [10]. Following SEC reforms in July 2023, funds now face stricter liquidity requirements and must impose liquidity fees in certain situations. These changes replace the previous system of redemption "gates", which could temporarily block withdrawals [12]. These regulations help ensure money market funds remain stable and aligned with current interest rates.

The financial crisis of 2008 highlighted weaknesses in the structure of money market funds. In September 2008, the Reserve Primary Fund’s net asset value (NAV) dropped to $0.97 per share after Lehman Brothers went bankrupt. This triggered a massive run on prime money market funds, with over $234 billion withdrawn, forcing U.S. Treasury intervention to stabilize the market [11][3]. Similarly, during the market turmoil of 2020 caused by COVID-19, investors redeemed approximately $139 billion from prime funds in a matter of weeks – nearly 17% of total assets [3].

"With these reforms in place, Paul Olmsted, a Morningstar principal for fixed-income strategies, considers most money market funds a relatively safe bet." [12]

Tokenized Money Market Funds

Tokenized money market funds take the principles of traditional money market funds and integrate them with blockchain technology. These funds offer real-time liquidity, instant settlement, and programmability, while maintaining the same asset backing as conventional funds.

For example, BlackRock’s BUIDL fund (BlackRock USD Institutional Digital Liquidity Fund), launched in 2024, surpassed $1 billion in assets under management by early 2025. Operating on the Ethereum blockchain, the fund provides institutional investors with a stable $1.00 NAV backed by cash, U.S. Treasury bills, and repurchase agreements. Its tokenized structure allows for instantaneous settlement of shares [3]. Similarly, Franklin Templeton’s OnChain U.S. Government Money Fund (FOBXX) uses blockchain technology on Stellar and Polygon to record share ownership. This fund invests at least 99.5% of its assets in government securities and cash [12].

New regulatory frameworks, such as the EU’s MiCA and the U.S. GENIUS Act, are bringing stablecoins and tokenized money market funds under similar transparency and reserve requirements [3]. This evolving environment blends traditional financial tools with decentralized finance, allowing these funds to operate outside standard market hours while adhering to regulatory standards.

Yield Comparison: DeFi Lending vs Money Market Funds

DeFi Lending Returns

In 2026, DeFi lending offered annual yields ranging from 2.3% to 7.2% APY for stablecoin-focused strategies. For example, in March 2026, Aave V3 provided returns of 3.5% to 5.0% on USDC deposits, while Morpho Blue delivered slightly higher rates of 4.0% to 7.2%. Meanwhile, Compound V3 lagged with yields between 3.0% and 4.5% [5].

These returns are heavily influenced by on-chain utilization rates, which measure the percentage of liquidity actively borrowed from lending pools. Borrowing demand – driven largely by leveraged trading – also plays a crucial role in sustaining these yields [5][8]. By 2026, yields from genuine borrower demand had stabilized between 6% and 8%, a sharp decline from the double-digit APYs seen in earlier years [8].

However, gross DeFi yields often need adjustments. Analysts typically reduce them by 1%–3% to reflect risks associated with smart contracts [6]. This is no minor consideration, given that over $2.47 billion in cryptocurrency was stolen during the first half of 2025 due to exploits [13]. Additionally, transaction fees can cut into returns. For instance, Ethereum mainnet gas fees can range from $50 to $150 for complex transactions, while Layer 2 solutions like Arbitrum and Base significantly lower costs to about $0.50 [5][6].

Money Market Fund Returns

Money market funds, on the other hand, provide consistent but lower yields, typically ranging from 4.0% to 5.5% APY as of early 2026 [7][14]. These returns align closely with the Federal Reserve’s benchmark rate, which stood at 3.50%–3.75% in January 2026 [7]. Government money market funds – investing nearly all assets in cash and U.S. Treasuries – offered around 4.5% APY, while prime funds, which include corporate debt, provided slightly higher yields but with added credit risk [6][8].

High-yield savings accounts (HYSAs) mirrored similar rates during this time. For instance, Varo Money offered 5.00% APY in February 2026, while the national average for savings accounts remained at just 0.39% [7]. Interactive Brokers, meanwhile, paid 3.14% on idle cash [13]. Unlike DeFi, these yields are determined by institutions and adjust gradually based on Federal Reserve policies, offering stable and predictable income streams.

Money market funds also avoid the risks tied to DeFi, such as smart contract vulnerabilities or blockchain-related volatility. Their returns are largely influenced by central bank policies and inflation expectations, remaining steady regardless of broader market conditions [14].

Yield Comparison Table

| Metric | DeFi Lending (Stablecoins) | Money Market Funds |

|---|---|---|

| Typical APY Range | 2.3% – 7.2% | 4.0% – 5.5% |

| Primary Yield Driver | On-chain utilization & leverage demand | Federal Reserve benchmark rates |

| Volatility | High; rates change quickly | Low; rates set by institutions |

| Net Real Return | 4.2% – 6.8% (after risk/gas adjustments) | 4.0% – 5.5% |

| Insurance | None (smart contract risk) | FDIC insured up to $250,000 |

| Liquidity | Instant (subject to pool utilization) | Instant to 3 business days |

Data reflects March 2026 market conditions [5][6][7][14].

These trends highlight a narrowing gap between DeFi and traditional finance. For instance, in April 2026, Aave’s USDC pool on Ethereum offered a modest 2.61% APY, falling short of the 3.14% paid by Interactive Brokers on idle cash [13]. Paul Frambot, Co-founder of Morpho, shed light on this convergence:

"Undifferentiated lending converges toward risk-free rates because when every depositor shares the same collateral… there is limited room for specialization and returns compress." [13]

As the difference between DeFi and traditional finance shrinks, investors face a tough choice: are the slightly higher yields in DeFi worth the added technical risks and operational challenges?

Risk Analysis: DeFi Lending vs Money Market Funds

DeFi Lending Risks

DeFi lending comes with its own set of challenges, particularly smart contract vulnerabilities, which can lead to massive losses. For instance, in March 2023, Euler Finance was hit by an exploit that cost them around $197 million due to a flaw in their liquidation logic [16]. Similarly, in April 2026, Drift Protocol on Solana faced a $270 million loss when attackers compromised a Security Council multisig [4].

Another significant concern is liquidation risk, especially during market volatility. When market dips happen – like a 15% drop – health factors can quickly decline from 1.3 to 1.0, triggering liquidations with penalties ranging from 5% to 10% [5]. A notable example occurred during a 48-hour ETH crash in May 2025, which led to over $600 million in liquidations on platforms such as Aave and Compound [16]. And let’s not forget March 2020’s "Black Thursday", when network congestion caused MakerDAO vaults to be liquidated for as little as $0, creating $8.3 million in bad debt [15].

Oracle manipulation is another risk to watch. In October 2022, an attacker exploited Mango Markets by inflating MNGO’s price through flash loans, ultimately borrowing $114 million against the manipulated collateral [15]. Governance attacks are equally concerning – Beanstalk lost $182 million in April 2022 when an attacker used a $1 billion flash loan to gain a two-thirds voting majority and drained the treasury [15].

"If you cannot identify exactly which risks you are taking on for a given yield, you are probably the exit liquidity."

- Jorge Rodriguez, Lince Yields [15]

With such a wide range of technical and operational risks, DeFi lending presents a complex risk landscape compared to traditional financial instruments.

Money Market Fund Risks

Money market funds operate differently, benefiting from regulatory oversight and well-established frameworks. While they avoid the technical risks seen in DeFi, they aren’t without challenges. Interest rate changes directly affect returns. For example, when the Federal Reserve adjusts rates, money market fund (MMF) yields shift accordingly, though the impact tends to be gradual [3]. Credit risk exists in prime funds holding corporate debt, but strict SEC diversification and quality rules help mitigate these risks [3].

Liquidity constraints can arise during times of market stress. During the COVID-19 crisis in 2020, investors withdrew about $139 billion from prime MMFs within weeks [3]. A historic example is the Reserve Primary Fund, which "broke the buck" in September 2008 after Lehman Brothers’ collapse, causing its net asset value to drop to $0.97 and triggering a massive run that required U.S. Treasury intervention [3].

While DeFi risks can lead to total losses, money market fund risks are often contained within regulatory frameworks. During periods of stress, funds may impose redemption gates or liquidity fees. Additionally, many funds benefit from FDIC insurance (up to $250,000) or central bank backstops.

Risk Comparison Table

Here’s a side-by-side look at the main risks in DeFi lending and money market funds:

| Risk Category | DeFi Lending | Money Market Funds |

|---|---|---|

| Smart Contract | High risk of total loss from code exploits | Not applicable – operates on traditional systems |

| Liquidation | Automatic penalties (5–10%) during volatility | Not applicable – no collateral-based lending |

| Oracle Failure | High; price manipulation can cause exploits | Not applicable – no reliance on blockchain oracles |

| Liquidity Access | Instant, but withdrawals may be blocked | Daily liquidity; possible fees during stress |

| Regulatory | Evolving and uncertain | Highly regulated under SEC frameworks |

| Credit Risk | Minimal; often over-collateralized | Low; backed by T-bills and corporate debt |

| Counterparty | Protocol-specific risks (e.g., admin keys) | Issuer-specific (banks, corporate debt) |

| Insurance | Optional via services like Nexus Mutual | FDIC insured up to $250,000; central bank support |

Adjusting for Risk

To account for potential losses from exploits, analysts often apply a "Smart Contract Risk Discount" of 1% to 3% to DeFi’s gross APYs. This adjustment frequently reduces or even erases the yield advantage DeFi might have over traditional money market funds [6].

Investment Considerations

When deciding between traditional finance and DeFi options, it’s important to align your choice with your financial goals and risk tolerance. A key factor to weigh is the "Liquidity Premium" – the gap between risk-free returns (like U.S. Treasuries) and what you actually earn from DeFi after accounting for gas fees and smart contract risks [6].

In early 2026, the Federal funds rate was 3.50–3.75% [7], and high-yield savings accounts offered up to 5% APY, often surpassing the returns from flagship DeFi protocols. For instance, in April 2026, Aave V3’s USDC supply APY ranged from 2.61% to 2.72%, while Interactive Brokers offered 3.14% on idle cash for accounts exceeding $100,000 [4][1]. This yield inversion has shifted the risk-reward dynamic of DeFi investments.

Adding the typical 1–3% "Smart Contract Risk Discount" into the equation, even seemingly high DeFi yields can fall short compared to traditional returns. The Calcix Research Team explains:

"A 12% DeFi APY often results in a lower net return than a 4.5% Treasury Bill once you factor in the 2% average smart contract risk discount and the inevitable 5.7% drag caused by impermanent loss" [6].

This is why institutional investors often require a 3–5% premium over the 10-year Treasury yield to justify DeFi’s technical risks [6]. By understanding these factors, you can make more informed decisions. Below, we explore scenarios where DeFi lending or money market funds might be the better choice.

When to Choose DeFi Lending

DeFi lending is a good fit for risk-tolerant investors who are comfortable with potential losses and understand the technical complexities of smart contracts. It offers unique advantages over traditional finance, including:

- 24/7 liquidity

- Composability, like using deposit tokens (e.g., aUSDC) as collateral to maximize yields

- Isolated lending markets with tailored risk-return profiles [1][4]

In April 2026, Apollo Global Management, a $940 billion asset manager, partnered with Morpho to leverage its isolated lending markets. This move underscores how institutional investors value DeFi for capital efficiency rather than just headline yields [4][9].

One useful guideline is the "10x Gas Rule": only invest if your first month’s earnings are at least ten times your gas costs [6]. For smaller portfolios, this rule can eliminate many DeFi opportunities. To reduce risks, diversify across multiple protocols (like Aave, Compound, and Morpho) and chains (such as Ethereum, Arbitrum, and Base). Remember, DeFi lacks a lender of last resort, so diversification is key [7][1].

When to Choose Money Market Funds

For conservative investors who prioritize safety and steady returns, money market funds and high-yield savings accounts are often the better choice. These options are ideal for goals like saving for a house down payment or covering quarterly tax bills, where capital preservation is critical [6][7].

Money market funds come with strict regulations and FDIC insurance, offering a level of security that DeFi cannot match [3]. In early 2026, top U.S. high-yield savings accounts provided up to 5% APY, rivaling or exceeding many DeFi protocols without the added risks [7].

Another advantage is tax simplicity. Traditional options provide straightforward tax forms like the 1099-INT, while DeFi often involves complex "phantom gain" tax liabilities that require meticulous self-reporting [6][7]. For institutions, money market funds also provide a clear audit trail and regulatory compliance, areas where DeFi still lags.

Bestla VC‘s DeFi Yield Investment Services

Bestla VC specializes in guiding institutional clients through the complexities of DeFi yield investments. The firm focuses on curated vaults and isolated lending markets, such as those offered by Morpho, to create tailored risk-return profiles beyond what standard lending pools can offer [4].

Their approach includes risk-tiered strategies:

- Conservative portfolios (Tier 1) target 3–5% APY with safer options like tokenized T-bills or Aave.

- Only advanced clients access Tier 4 strategies (15%+ APY), which involve more complex setups like recursive loops and leverage [8].

To protect investments, Bestla VC uses automated monitoring tools that track Health Factors in real time, helping to prevent liquidations during market downturns [5]. Beyond yield optimization, they offer services like legal consultancy for compliant investment structures, OTC market solutions for liquidity management, and strategic partnerships with emerging DeFi protocols. These strategies reflect the broader evolution of the financial landscape, where yield compression signals a maturing market [4].

Conclusion

Deciding between DeFi lending and money market funds boils down to your individual risk tolerance and financial goals. By 2026, the financial landscape has evolved significantly. For instance, Aave V3’s USDC supply APY (2.61%–2.72% [1][4]) now lags behind traditional high-yield savings accounts, which can offer up to 5% APY [7]. This shift has challenged DeFi’s previous edge in delivering consistently higher returns.

Instead of focusing solely on headline APYs, it’s crucial to calculate net real returns. After accounting for gas fees, a typical 1–3% discount for smart contract risk, and the possibility of impermanent loss, DeFi rates often fall short compared to traditional options [6]. As the Calcix Research Team wisely notes:

"A true professional doesn’t just look for the highest number; they look for the most ‘efficient’ number – the highest return per unit of stress and risk" [6].

For many conservative investors, this analysis makes money market funds a more appealing choice, especially with the added security of FDIC insurance up to $250,000 [7]. On the other hand, investors with a higher risk appetite and a solid understanding of technical complexities can still tap into DeFi’s advantages, such as 24/7 liquidity [3] and tailored lending markets that offer specific risk-return profiles [4].

Institutional investors have even more tools at their disposal. Bestla VC, for example, provides tailored strategies, automated monitoring, and access to exclusive vaults beyond standard lending pools. Their offerings range from conservative Tier 1 portfolios aiming for 3–5% APY [8] to comprehensive support services, including legal consultancy and strategic partnerships with emerging DeFi protocols. These solutions make navigating the evolving financial ecosystem more manageable for professionals seeking optimized returns.

FAQs

How can I estimate my net DeFi APY after accounting for gas fees and smart contract risk?

To figure out your net DeFi APY, begin with the gross APY provided by your selected platform. Then, deduct gas fees, which can range from $50 to $150 per transaction, depending on the blockchain. Next, factor in a risk discount – typically 1% to 3% – to account for potential issues like smart contract vulnerabilities. If your assets are subject to high volatility, you may need to make additional adjustments.

For instance, if your gross APY is 8%, these deductions could bring your net APY down to somewhere between 6.8% and 7.5%.

Is DeFi lending safer if I only lend stablecoins like USDC?

Lending stablecoins like USDC in decentralized finance (DeFi) tends to carry less risk compared to lending volatile cryptocurrencies. Since stablecoins are pegged to fiat currencies like the U.S. dollar, they’re designed to avoid the dramatic price swings seen with assets like Bitcoin or Ethereum. This makes them a popular choice for those looking to minimize exposure to market fluctuations.

That said, lending stablecoins isn’t without its risks. Issues like smart contract vulnerabilities or platform insolvencies can still pose threats. While stablecoins help reduce market-related risks, they don’t address potential problems tied to the security or reliability of the lending platform itself.

Which is better for cash I may need soon: DeFi lending or a money market fund?

For short-term cash needs, money market funds or high-yield savings accounts are often the go-to options. Why? They provide liquidity, insurance protections (up to $250,000 or $500,000, depending on the account), and allow for easy withdrawals – making them both safe and convenient.

On the other hand, DeFi lending can offer higher yields, typically ranging from 2.6% to 7%. However, it comes with greater risks, such as smart contract vulnerabilities and market volatility. Because of these risks, DeFi lending is usually a better fit for longer-term goals or higher-risk strategies rather than immediate cash needs.