Decentralized Finance (DeFi) has become a $55+ billion asset class that institutions can no longer ignore. By 2025, DeFi lending protocols like Aave managed $33 billion in total value locked, while the stablecoin market grew to $295 billion by early 2026. Institutional adoption is accelerating, but success hinges on three critical factors:

- Custody Solutions: Institutions need secure methods to manage digital assets. Options include non-custodial wallets for direct control or regulated qualified custodians for compliance with SEC rules.

- Compliance Frameworks: Regulatory clarity has improved with laws like the EU’s MiCA and the U.S. GENIUS Act. Institutions must follow SEC and CFTC guidelines, adhere to AML/KYC rules, and use permissioned liquidity pools for verified transactions.

- Risk Management: DeFi’s risks – like smart contract exploits – require robust safeguards, including threat detection, economic stress testing, and real-time portfolio monitoring.

"Questions Institutions Need to Consider When Offering Custody Services" with Zodia Custody

sbb-itb-c5fef17

Custody Solutions for Institutional DeFi

Picking the right custody model is a critical step for institutions diving into DeFi. The choice largely depends on regulatory compliance, operational control, and security measures. By 2025, 32% of financial advisors were investing in crypto for client accounts, with over 40% of Registered Investment Advisors (RIAs) allocating to digital assets. This trend highlights the growing institutional interest in crypto and the increasing focus on custody practices [6].

The SEC’s Custody Rule (Rule 206(4)-2) mandates that many regulated advisors keep client assets with a "qualified custodian" [6][3]. Self-custody setups often fall short of meeting these regulatory standards for "safekeeping", exposing institutions to potential legal risks. Enforcement actions in the past have shown that non-compliance with this rule can lead to hefty penalties [3]. For regulated entities, working with qualified custodians isn’t just a best practice – it’s a necessity.

Non-Custodial Wallets

Non-custodial wallets, also known as self-custody wallets, give institutions complete control over their private keys. This setup allows for direct access to DeFi protocols without waiting for third-party integrations, enabling institutions to seize yield opportunities quickly.

However, this model comes with significant responsibilities and risks. Institutions are fully accountable for managing keys, backups, and security protocols. Mistakes, insider threats, or technical failures could result in severe consequences. Additionally, insurance costs for self-custody are notably higher, often ranging from 5-15% of the coverage amount, compared to 1.5-4% when using a qualified custodian [5]. Most importantly, self-custody does not meet the SEC’s "qualified custodian" criteria, making it unsuitable for RIAs and other regulated entities [3][6].

While self-custody offers unmatched flexibility, regulated alternatives provide the compliance and security safeguards that institutions often need.

Qualified Custodians and SEC Compliance

Qualified custodians are regulated entities that manage digital assets in compliance with strict oversight standards [8]. Licensed by authorities such as the New York Department of Financial Services (NYDFS) or Germany’s BaFin, these custodians ensure client assets are segregated and protected from creditors in case of insolvency [6][5].

"By utilizing Fireblocks Trust Company LLC, we marry world-class technical innovation with the elite oversight of a New York-chartered trust… it provides a sophisticated governance framework that satisfies the most stringent institutional requirements." – Sam Auch, Vice President, Head of Client Success & Partnerships, Bakkt [6]

Qualified custodians offer structured governance, complete with multi-level approval workflows and detailed audit trails. They also provide robust insurance coverage, often underwritten by Lloyd’s of London, with policies ranging from $30 million to over $100 million [1][8]. Fees typically include annual custody charges of 10 to 50 basis points (bps) on assets under management, along with transaction fees, and minimum balances often fall between $250,000 and $10 million [1][5].

For example, in 2025, Valor Capital Group partnered with Fireblocks Trust to secure a portfolio token within five days. This collaboration ensured both speed and compliance, meeting the security requirements of their limited partners [6].

Multi-Party Computation (MPC) Technology

Multi-Party Computation (MPC) technology enhances security by splitting private keys into multiple shares, which are distributed across different parties or locations [9][7]. No single entity ever possesses the entire key. Transactions are approved collaboratively, with a quorum (e.g., 2-of-3 or 3-of-5) performing cryptographic operations to produce a final signature without reconstructing the full key [9][1].

"Think of MPC not as a single key, but as a key that is instantly shattered into multiple pieces, or ‘shares,’ and distributed across different locations and parties. No single person or system ever holds the complete key." – Fystack [9]

MPC offers advantages over traditional multi-signature setups, such as generating a standard single signature compatible with all blockchain protocols. This eliminates the need for chain-specific smart contracts, making MPC easier to use across various DeFi platforms [7]. Additionally, MPC allows for "refreshing" key shares without changing the wallet address [1].

In July 2022, Blockdaemon acquired Sepior, an MPC technology leader, to enhance its custodial wallet capabilities. By April 2026, this infrastructure was securing over $2 billion in daily transactions for global banks and exchanges, using a threshold security module to distribute private key shares across multiple nodes [7][10]. Fireblocks, combining MPC with Trusted Execution Environments (TEE) and Hardware Security Modules (HSM), safeguards more than $10 trillion in digital assets for over 2,400 institutions [6].

Both self-custody solutions and qualified custodians now incorporate MPC technology to improve security [1][7]. The key difference lies in who controls the key shares: institutions manage them internally in self-custody setups, while qualified custodians handle them within a regulated framework. To maximize security, institutions should distribute MPC nodes across different Cloud Service Providers (CSPs) to prevent outages or breaches from affecting a single provider [7]. MPC has become a cornerstone of institutional custody strategies, blending flexibility with enhanced security.

Regulatory Compliance Frameworks

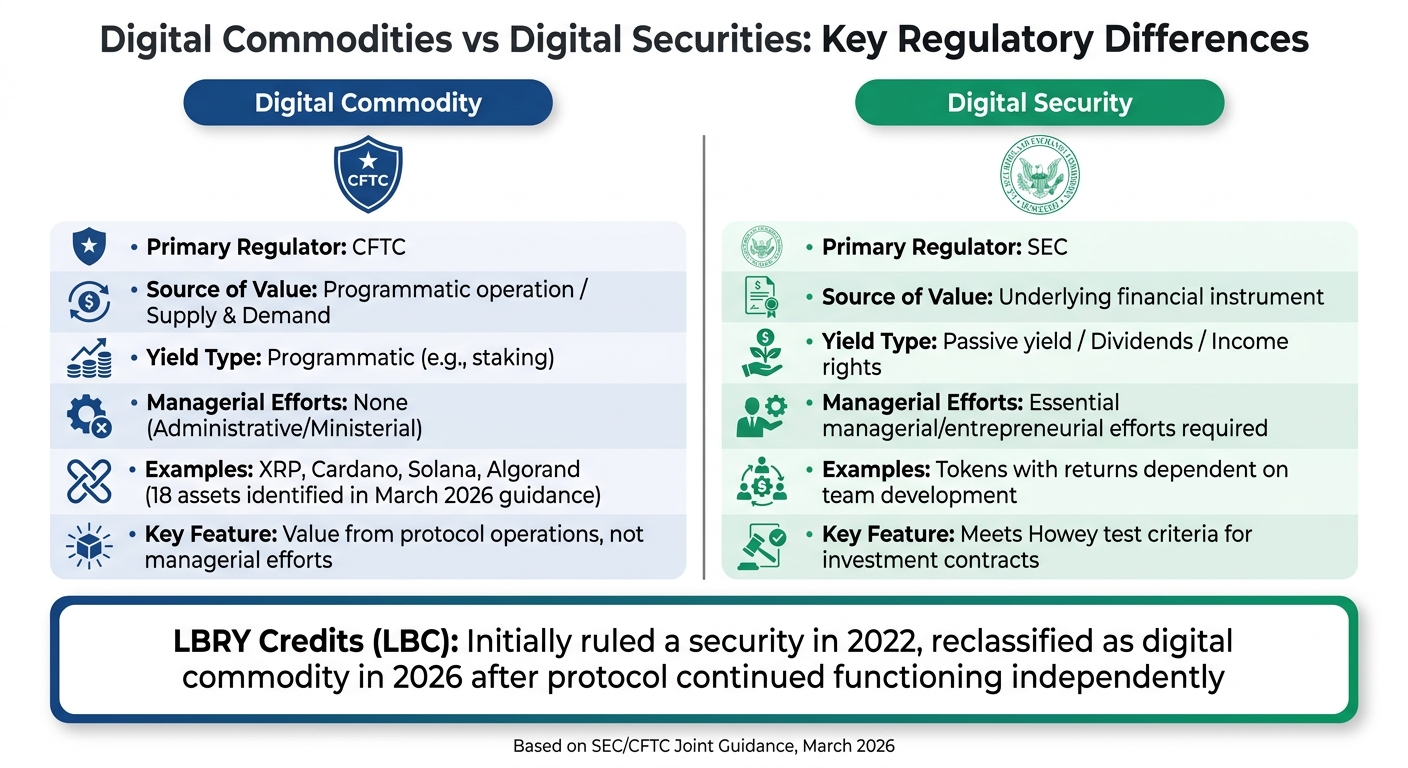

Digital Commodities vs Digital Securities: Regulatory Classification Framework

Strong regulatory frameworks are just as important as secure custody solutions for institutions stepping into the world of DeFi. For institutions, understanding and navigating these regulations isn’t optional – it’s essential. In March 2026, the SEC and CFTC issued joint guidance that reshaped how digital assets are classified, focusing on their economic characteristics and the roles of their issuers [12][13]. This guidance identified 18 specific crypto assets, including XRP, Cardano, Solana, and Algorand, as digital commodities. Notably, 16 of these already have futures contracts traded in CFTC-regulated markets [13]. The key difference? Digital commodities gain value from programmatic operations and market dynamics, while assets tied to passive income, financial rights, or ongoing managerial work fall under SEC jurisdiction as securities.

"The interpretation is the Commission’s first step toward developing a clearer regulatory framework for the treatment of crypto assets under the Federal securities laws." – SEC/CFTC Joint Release [11]

Institutions must ensure that DeFi yield products generate returns through protocol-driven mechanisms, not through managerial or entrepreneurial efforts. These distinctions directly inform the compliance measures that institutional investors must follow.

SEC and CFTC Regulations

The Howey test plays a central role in determining whether a DeFi product qualifies as an investment contract. It evaluates whether money is invested in a common enterprise with an expectation of profit derived solely from others’ efforts [11][12]. The March 2026 guidance clarified that activities like protocol mining and staking (including liquid staking) are generally administrative or operational, and thus do not count as securities offerings [13]. For example, staking ETH through a protocol’s consensus mechanism is typically considered compliant. However, tokens whose returns depend on a team’s ongoing development or business decisions are likely to be classified as securities, requiring registration or exemptions.

The GENIUS Act, passed in early 2026, introduced the first federal framework for digital assets. It defined "Digital Assets" and excluded compliant payment stablecoins from being categorized as securities [11][13]. This provides institutions with clearer guidelines for incorporating stablecoins into DeFi strategies without triggering securities registration requirements.

Tax reporting adds another layer of complexity. Starting January 1, 2027, digital asset intermediaries – including DeFi front-end platforms – must collect user information and report transactions to the IRS using Form 1099-DA [14].

The regulatory division between commodities and securities creates distinct compliance paths, as shown below:

| Asset Type | Primary Regulator | Source of Value | Yield Type | Managerial Efforts |

|---|---|---|---|---|

| Digital Commodity | CFTC [13] | Programmatic operation/Supply & Demand [12] | Programmatic (e.g., staking) [13] | None (Administrative/Ministerial) [13] |

| Digital Security | SEC [13] | Underlying financial instrument [12] | Passive yield/Dividends/Income rights [13] | Essential managerial/entrepreneurial efforts [12] |

A case in point is LBRY Credits (LBC). Initially ruled a security in 2022 (SEC v. LBRY, Inc.), it was later reclassified as a digital commodity in the 2026 guidance because the protocol continued functioning independently after the company ceased operations [12][13].

AML and KYC Requirements

Beyond asset classification, institutions must also comply with rigorous anti-money laundering (AML) and know-your-customer (KYC) requirements. These are essential under the Bank Secrecy Act. FinCEN has clarified that developers and participants in DeFi protocols may be considered money transmitters and subject to these rules [17].

"Developers and participants in decentralized finance protocols can be considered money transmitters and may be subject to Bank Secrecy Act (BSA) requirements." – FinCEN [17]

Additionally, the Financial Action Task Force’s "Travel Rule" requires institutions to share sender and recipient data for transactions exceeding certain thresholds. This poses challenges to DeFi’s pseudonymous nature, but the industry is adapting by moving from wallet-based trust to identity-based trust [15].

"The market is moving from wallet‑based trust to identity‑based trust." – Chainlink [15]

For institutions with fiduciary duties, transacting with anonymous parties is not an option. This has led to the rise of permissioned liquidity pools – restricted environments where all participants are verified. These pools allow institutions to engage in DeFi without the risks posed by unverified actors. Emerging technologies, like Zero-Knowledge Proofs, help institutions verify key identity attributes (e.g., ensuring someone isn’t on a sanctions list) without exposing sensitive data. Meanwhile, Soulbound Tokens offer non-transferable proof of KYC compliance across protocols [15].

The stakes for compliance are high. In December 2022, Danske Bank A/S paid $2.06 billion to settle AML-related failures at its Estonian branch, where poor AML disclosures for non-resident customers occurred between 2009 and 2016 [16][18]. Similarly, the New York Department of Financial Services fined Deutsche Bank AG $425 million in 2017 for a mirror-trading scheme that moved $10 billion out of Russia due to weak KYC controls [18]. Institutions must implement thorough due diligence measures, including Customer Identification Programs (CIP), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD) for higher-risk cases. Blockchain analytics are also critical for monitoring sanctions violations and tracking fund origins [16][18].

VASP Licensing and Registration

Virtual Asset Service Provider (VASP) licensing introduces a mix of federal and state requirements. Institutions must register federally as a Money Services Business with FinCEN and comply with the Bank Secrecy Act [20][23]. At the state level, frameworks like New York’s BitLicense, California’s Digital Financial Assets Law (DFAL), and Illinois’ Digital Assets and Consumer Protection Act (DACPA) are setting new standards. For instance, California’s DFAL mandates that companies managing over $150,000 in customer digital assets either use a qualified custodian or secure an insurance bond [5]. Illinois’ DACPA, effective January 1, 2027, imposes custody protections and will require full licensing compliance by July 1, 2027. Non-compliance can lead to penalties of up to $25,000 per violation [22].

The GENIUS Act further adds federal requirements for payment stablecoin custodians, effective January 18, 2027, creating overlapping federal and state compliance obligations [5].

"A VASP license is the legal prerequisite for operating a crypto exchange, custody service, or any other business that handles virtual assets on behalf of third parties." – LegalBison [19]

To obtain a VASP license, companies must demonstrate robust AML/CTF measures, including effective KYC protocols and transaction monitoring. Regulators also evaluate the backgrounds, criminal records, and financial stability of directors and beneficial owners [19][20][23]. Institutions must maintain minimum capital reserves and liquidity ratios to ensure solvency [19][21]. Given the time-intensive nature of the application process, engaging with regulators early and establishing transparent governance – with defined roles for key officers like the Chief Financial Officer and Compliance Officer – can help streamline the process.

Risk Management for Institutional DeFi

For institutions diving into DeFi yield strategies, risk management isn’t just important – it’s a necessity. The decentralized nature of DeFi introduces risks like technical flaws, unreliable counterparties, and volatile markets that traditional finance rarely encounters. The numbers speak for themselves: DeFi protocols faced $1.4 billion in exploits in 2025, though permissioned institutional protocols accounted for only $67 million of those losses. This demonstrates that structured risk strategies can significantly limit exposure [4].

DeFi’s 24/7 operations, autonomous smart contracts, and rapid liquidity shifts mean institutions can’t rely on legacy risk frameworks designed for equities or bonds. Instead, they need continuous oversight, in-depth technical evaluations, and controlled access to safeguard their capital and uphold fiduciary responsibilities.

Smart Contract Risk Assessment

Smart contracts are the backbone of DeFi, but they also pose one of its biggest risks. A single coding flaw or an insufficient audit can lead to catastrophic losses. Tools like the K Framework provide mathematical validation for smart contracts, while economic audits simulate extreme market conditions to test a protocol’s resilience [4].

For example, in May 2022, Gauntlet‘s risk modeling platform simulated 10,000 market scenarios daily, identifying vulnerabilities in the Terra/Luna ecosystem. By advising institutions to reduce positions 72 hours before the depeg event, it helped prevent $890 million in potential losses [4]. This kind of proactive modeling can avert systemic collapses.

Real-time threat detection systems are equally critical. In March 2023, Forta‘s network detected the Euler Finance hack 25 minutes before it concluded, allowing three institutions to withdraw $47 million before the protocol was drained [4]. Early detection tools, paired with automated responses like circuit breakers, can mitigate losses by acting swiftly during emerging threats.

When engaging with protocols, institutions should prioritize those with at least six months of mainnet operation and multiple successful audits [4]. Diversification is also key – investments should typically be limited to 5-10% of a protocol’s TVL to avoid overexposure. Additionally, transaction simulation tools can help identify potential issues, such as malicious logic, before funds are committed [1].

| Risk Mitigation Tools | Function | Key Providers |

|---|---|---|

| Formal Verification | Validates smart contract code | Runtime Verification, K Framework |

| Threat Detection | Monitors for real-time exploits | Forta, Hypernative |

| Risk Modeling | Simulates economic stress scenarios | Gauntlet, Chaos Labs |

| Incident Response | Automates liquidity removal | OpenZeppelin Defender |

| Bug Bounties | Rewards for finding vulnerabilities | Immunefi |

| Insurance | Covers financial losses | Nexus Mutual, Sherlock |

Bug bounty programs have proven effective in addressing vulnerabilities. In 2025, Immunefi facilitated $82 million in payouts, with some bounties reaching $10 million [4]. Protocols that actively engage with security researchers through these programs are better equipped to address risks before they escalate.

Permissioned Liquidity Pools

Managing counterparty risk is another cornerstone of institutional DeFi strategies. Interacting with anonymous participants exposes institutions to compliance and sanctions risks. Permissioned liquidity pools address this by limiting access to verified participants who have completed KYC checks. These pools offer a controlled environment where institutions can safely operate without legal or operational concerns.

Policy engines further enhance security by whitelisting approved protocols and addresses. Institutions can tier protocols based on their security and operational history. For instance, Tier 1 might include well-established players like Aave, while Tier 2 could encompass newer, audited protocols with stricter exposure caps [2].

"Institutional-grade custody and compliance translates to infrastructure that maintains continuous asset control, enforces structured authorization logic, and integrates policy-level safeguards while maintaining the composability of smart contract environments." – Paul, Author, Cantina Blog [2]

Multi-level authorization workflows prevent single points of failure by requiring multiple approvals – such as from an analyst, portfolio manager, and risk officer – before executing transactions [1]. Emergency override procedures and quorum requirements for large transfers add another layer of protection.

Real-time risk scoring tools block interactions with flagged addresses, ensuring compliance with AML and sanctions regulations. These tools integrate seamlessly with custody platforms, providing instant alerts for suspicious transactions [2].

Real-Time Monitoring and Analytics

DeFi’s round-the-clock nature means risks can emerge anytime, making real-time monitoring essential. These systems provide immediate insights into protocol exposure, portfolio valuation, and operational anomalies, helping institutions manage liquidity risks in volatile markets.

Operational alert systems notify risk teams of unusual activities, such as unauthorized transactions or sudden governance changes. For example, in April 2026, Coinbase Cloud managed 2.1 million staked ETH ($7.4 billion) for 847 institutional clients. Automated slashing insurance and performance monitoring helped mitigate validator-related risks, showcasing the importance of continuous oversight [4].

Granular exposure tracking allows institutions to break down positions by protocol, asset type, and risk category. This visibility helps identify overconcentration and rebalance portfolios before issues arise. Compliance integration ensures every transaction is traceable, with detailed audit trails for regulatory reporting.

MEV (Miner Extractable Value) protection tools like Flashbots Protect also play a critical role. In 2025, these tools saved institutions an estimated $890 million by preventing front-running attacks [4]. By ensuring fair transaction execution, they shield institutions from sophisticated exploitation.

Institutions should regularly evaluate their security measures, conducting quarterly assessments and annual penetration testing for both internal systems and third-party providers. While the cost of comprehensive monitoring ranges from $150,000 to $400,000 annually, it’s a necessary investment to protect against potentially massive losses [4].

Implementation Best Practices

Turning ideas into action requires making clear decisions about custody, fund structures, and advisory partnerships. These choices will shape whether your DeFi approach runs smoothly or encounters compliance and operational challenges. With 86% of institutional investors already holding digital assets or planning to invest within two years, nailing these fundamentals is more important than ever [29]. Below are best practices that build on the earlier discussion of custody and compliance frameworks.

Selecting Custody Providers

Picking the right custody provider is one of the most critical steps for institutions entering the DeFi space. The provider you choose impacts your ability to execute strategies, respond to market shifts, and meet regulatory requirements. In 2024 alone, cryptocurrency losses reported to the FBI surpassed $6.5 billion, highlighting the need for strong custody solutions [26].

Start by assessing the provider’s security measures. Multi-Party Computation (MPC) is widely regarded as the gold standard for institutions. By distributing key shares across multiple parties, MPC eliminates single points of failure.

Regulatory compliance is another key consideration. Registered Investment Advisors (RIAs) must use qualified custodians to comply with SEC Rule 206(4)-2. Providers like Fireblocks Trust Company (regulated under New York Banking Law), Anchorage Digital (OCC National Bank Charter), and BitGo (regulated qualified custodian) meet these standards [6]. A cautionary example is Galois Capital, which settled with the SEC for $225,000 in 2025 after failing to follow the Custody Rule for crypto asset management [3].

"RIAs now have regulatory clarity to work with custodians like Fireblocks Trust Company… without the ambiguity that previously made compliance officers uncomfortable." – Fireblocks [6]

Evaluate the provider’s DeFi connectivity. Some offer native integrations with platforms like Aave and Uniswap, while others rely on APIs or WalletConnect sessions. The level of integration can significantly impact how quickly you can act and the complexity of operations. Providers with advanced policy engines allow institutions to set granular controls, such as whitelisting contract addresses, imposing spending limits, and requiring multi-level transaction approvals [1].

Insurance coverage is another major factor. For instance, BitGo offers coverage up to $250 million for loss, theft, or misuse when it holds all keys, while Fireblocks Trust Company provides coverage starting at $30 million+ [26]. However, standard custody insurance typically excludes protocol-level failures, so institutions should consider separate smart contract insurance [3].

Costs for institutional custody typically range from 10 to 50 basis points annually on assets under management, along with transaction fees. Minimum asset requirements generally fall between $250,000 and $10 million [1]. Before committing, conduct a thorough RFP process. Focus on security, ease of use, asset compatibility, and customer support. Request demos showing how providers handled past outages or security breaches, and run "fire drills" to test emergency protocols [26].

These decisions around custody lay the groundwork for building compliant and efficient fund structures.

Using Regulated Fund Structures

Once custody is in place, regulated fund structures help streamline operations and compliance. By adopting recognized legal frameworks – like BVI-domiciled funds or Cayman exempted limited partnerships – institutions can avoid the risks tied to unregistered yield programs [28].

These structures allow managers to seamlessly integrate with qualified custodians while maintaining full control over strategy, allocation, and rebalancing. U.S. Regulation D supports offerings for accredited investors, while Regulation S applies to offshore investors. Section 3(c)(7) of the Investment Company Act helps funds avoid registration as investment companies [28].

Aave Arc showcases how regulated structures can align with permissioned DeFi. Launched in January 2022 as a KYC-verified lending pool through Fireblocks, it attracted $8.7 billion in deposits from 31 whitelisted institutions by March 2026. Its conservative loan-to-value ratio of 42% ensured zero liquidations during the March 2023 banking crisis [4].

Another example is BlackRock’s BUIDL fund, which uses a dual-layer custody model. BNY Mellon safeguards Treasury assets, while investors’ chosen providers manage ERC-20 tokens on Ethereum. This setup ensures that even if the tokenization platform experiences issues, the underlying assets remain secure with a trusted custodian bank [27].

Establishing a DeFi framework typically involves upfront costs of $200,000 to $500,000 in legal and consulting fees over four months. One European asset manager spent $3.2 million building their DeFi infrastructure and recouped the cost within seven months through yield optimization and reduced operational expenses compared to traditional fixed-income operations [4].

Partnering with Specialized Advisors

After securing custody and fund structures, working with specialized advisors ensures smooth implementation of compliance and risk controls. These advisors bridge the gap between traditional custody rules and decentralized processes [24].

Bestla VC is one such firm, offering expertise in DeFi yield strategies, legal frameworks, and compliance systems. Advisors validate operational and governance structures through code reviews, operational checks, and administrative oversight [2]. For instance, they help institutions implement onchain permission systems like Zodiac Roles Modifier, which controls access at the contract and function levels, including setting limits on swaps [29].

Compliance automation is another benefit. Advisors integrate real-time monitoring and risk scoring to block transactions involving high-risk or sanctioned addresses, ensuring adherence to AML and "Travel Rule" requirements [2]. Many institutional custody failures stem from weak internal controls rather than blockchain vulnerabilities, making these safeguards critical [25].

"Institutions interested in DeFi must reconcile traditional custody rules with a decentralized framework that operates outside the conventional financial system." – Talos [24]

Advisors can also provide pre-built permission frameworks for popular protocols, speeding up deployment and reducing operational risks. For example, Karpatkey’s DeFi-Kit offers ready-made permission sets that institutions can use immediately, avoiding the need to build from scratch [29]. These frameworks include detailed audit logs and reporting to satisfy internal and external compliance requirements in regions like Hong Kong and Singapore [2].

Conclusion: Institutional DeFi Access with Bestla VC

Tapping into DeFi yield opportunities requires a solid grasp of custody, compliance, and risk management. By Q1 2026, institutional assets in DeFi protocols hit an impressive $47 billion[4], showing that institutions can engage securely. Still, moving from traditional finance to decentralized systems is no small task, especially when trying to align DeFi’s decentralized structure with SEC Rule 206(4)-2 custody requirements.

Bestla VC plays a key role in bridging this gap. By leveraging proven custody and compliance frameworks, they help institutions adopt MPC solutions, choose qualified custodians, and implement hybrid models that balance security with operational flexibility.

The firm also tackles regulatory hurdles, including the MiCA requirements effective since June 2024. These rules demand that entities overseeing DeFi protocols register as service providers[4]. Bestla VC supports institutions in meeting these regulations while setting up permissioned access frameworks that enforce strict KYC/AML protocols.

One of the biggest challenges Bestla VC addresses is meeting fiduciary standards. Retail-grade security simply isn’t sufficient for managing substantial assets. With 32% of financial advisors already investing in crypto for client accounts by 2025, and over 40% of RIAs expected to do the same[6], institutions need strategies designed for larger-scale, professional operations.

For institutions looking to integrate DeFi yield into a compliant and secure framework, Bestla VC offers the expertise required to transform speculative opportunities into well-regulated investments.

FAQs

Do RIAs need to use a qualified custodian for DeFi yield?

While RIAs (Registered Investment Advisors) aren’t strictly obligated to use a qualified custodian for managing DeFi yield, doing so offers several advantages. It can help ensure compliance with regulatory standards while providing a secure way to hold digital assets. This added layer of protection can reduce risks tied to handling institutional investments in the DeFi space.

How do permissioned pools help with AML/KYC and sanctions risk?

Permissioned pools tackle AML/KYC and sanctions challenges by implementing rigorous identity checks and compliance protocols. These measures ensure that only verified and approved participants can take part, minimizing the risk of illegal activities or regulatory violations.

What’s the safest way to limit smart contract exploit losses?

To reduce the risk of losses from smart contract exploits in institutional DeFi, it’s crucial to implement multi-layered custody solutions. Tools like multi-party computation (MPC) wallets can help by eliminating single points of failure.

Equally important are regular audits, formal verification, and continuous monitoring of smart contracts to identify and address weaknesses. Strengthening security further involves incorporating compliance measures such as multi-signature approvals, automated risk controls, and real-time anomaly detection. These safeguards work together to help prevent and respond to vulnerabilities effectively.