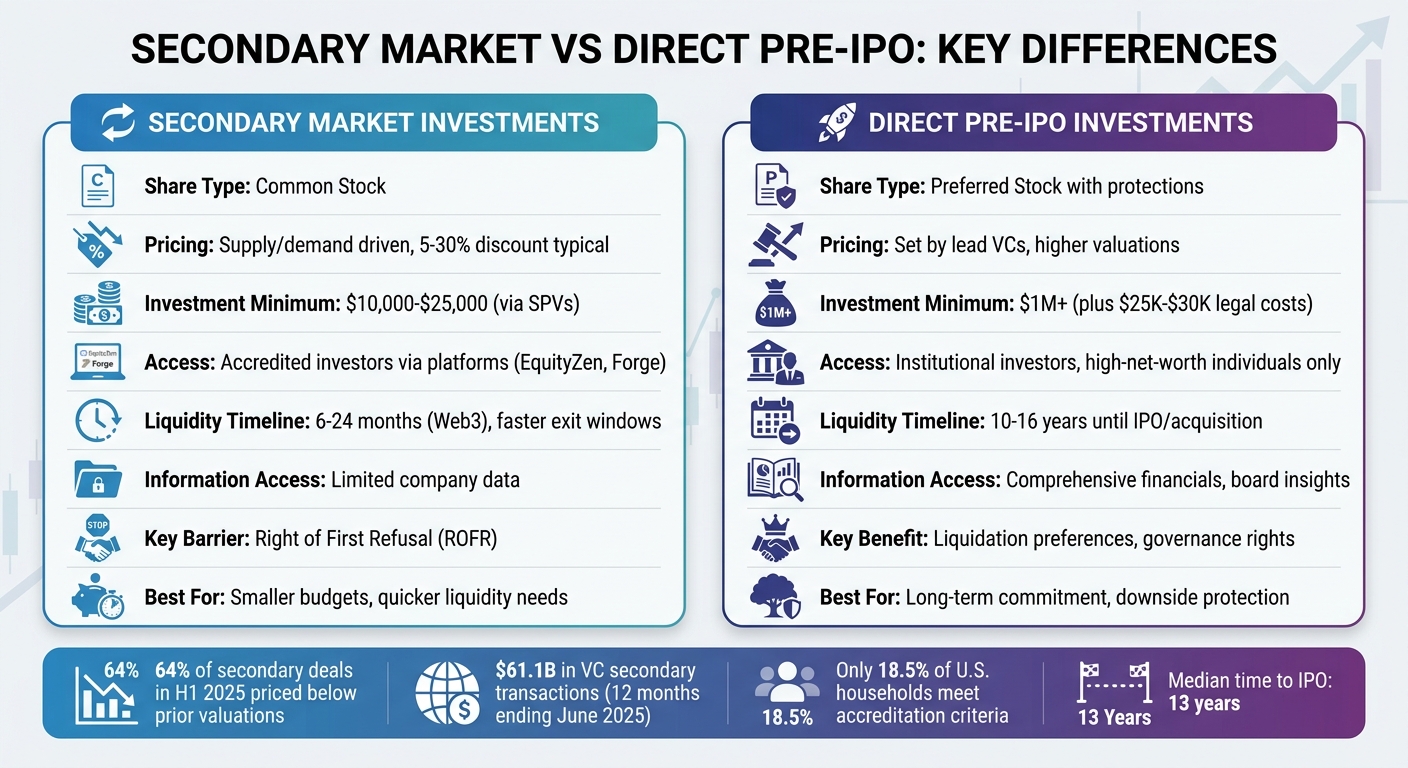

When investing in private companies, you have two main options: secondary market investments and direct Pre-IPO investments. Each has distinct pricing, access, and liquidity features.

- Secondary Market Investments:

- You buy shares from existing shareholders (e.g., employees or early investors).

- Shares are typically common stock, often sold at a discount (5%–30%) compared to the latest funding round.

- Easier access for accredited investors via platforms like EquityZen, with lower minimums ($10,000–$25,000).

- Faster liquidity, but limited information and potential deal barriers like Right of First Refusal (ROFR).

- Direct Pre-IPO Investments:

- You purchase newly issued shares directly from the company during a funding round.

- Shares are usually preferred stock, offering added protections like liquidation preferences.

- Reserved for institutional investors or high-net-worth individuals, with higher minimums (often $1M+).

- Long-term commitment, as funds are tied up until an IPO or acquisition.

Quick Comparison:

| Feature | Secondary Market Investment | Direct Pre-IPO Investment |

|---|---|---|

| Pricing | Driven by supply/demand; discounts common | Set by lead investors; higher prices |

| Access | Available to accredited individuals | Limited to institutions and high-net-worth investors |

| Liquidity | Moderate; faster via platforms | Low; tied to IPO or acquisition |

| Share Type | Common stock | Preferred stock with protections |

| Investment Minimum | $10,000–$25,000 (via SPVs) | $1M+ |

| Information | Limited access to company data | Comprehensive access to financials |

Each option caters to different goals. Secondary markets are better for smaller budgets and quicker liquidity. Direct Pre-IPO investments suit those seeking governance rights and downside protection but require patience and higher capital. Choose based on your financial goals and risk tolerance.

Secondary Market vs Direct Pre-IPO Investment Comparison Chart

1. Secondary Market Investments

Pricing Dynamics

In secondary markets, prices are shaped by supply and demand, unlike primary rounds where prices are set by lead investors. This dynamic often leads to a wide range of discounts, influenced by various market conditions.

A key factor here is the difference between preferred shares – commonly held by venture capitalists – and common shares traded in secondary markets. This gap, often called the "409A Delta", can range from 50% to 80%. The discount reflects the additional perks of preferred shares, like liquidation preferences and protective provisions[2].

Web3 pricing is particularly sensitive to broader market trends. For example, Coinbase‘s EV/Revenue compression in early 2025 caused private valuations to drop. Additionally, large unlock events from earlier seed SAFTs have increased the available supply, pushing buyers to demand steeper discounts. In the first half of 2025, 64% of secondary deals were priced below their prior primary valuations – a 10% jump from the previous year[4].

Different sectors also see varying impacts. Capital has increasingly flowed toward infrastructure and modular solutions like Layer 1s and AI-compute, while consumer-facing sectors such as GameFi have faced sharper discounts. For instance, GameFi deals have traded at a median discount of about 55%, whereas top-tier companies with clear IPO trajectories have, in some cases, traded at premiums of 200% or more compared to earlier funding rounds[4][6].

While pricing reflects these market forces, investors must also navigate significant barriers to entry.

Access and Barriers

Secondary market participation comes with its own set of challenges. The first hurdle is accreditation. According to SEC Regulation D, individuals must earn $200,000 annually (or $300,000 jointly) or have a net worth exceeding $1 million, excluding their primary residence. As of early 2026, only about 18.5% of U.S. households meet these criteria[2].

Even accredited investors face obstacles like the Right of First Refusal (ROFR). This clause allows companies or existing investors to buy back shares under negotiation – usually within 30 to 60 days – causing many deals to fall apart during this window[2]. Companies actively raising funds are more likely to exercise ROFR, while those with established secondary programs may waive it.

Investment minimums also limit access. Secondary deals often require $100,000 or more, though Special Purpose Vehicles (SPVs) can lower the barrier to $10,000–$25,000. However, SPVs come with added costs, including a 3–5% transaction fee, setup fees ranging from $10,000 to $20,000 (shared among investors), and carried interest of 10–20%[2].

Another challenge is information asymmetry. Secondary buyers generally have access to less detailed financial data compared to primary investors or the company itself. This lack of transparency can make valuations uncertain, especially in Web3, where factors like complex vesting schedules and multi-jurisdictional regulations add layers of complexity[9].

"In the secondary market, the buyer often knows more than the seller. Institutional buyers often have access to ‘side letters’ or updated financial disclosures that you… might not." – Calcix Research Team[10]

Liquidity Options

One advantage of secondary markets is faster liquidity compared to direct Pre-IPO investments, which often tie up capital until a significant exit event. In Web3, exit windows typically range from 6 to 24 months, driven by early token unlocks and the prevalence of SAFTs[4].

In 2025, 56% of Web3 secondary deals were finalized in under one month. The private equity secondary market saw $100 billion in transaction volume during the first half of 2025 – a 42% increase from the same period in 2024[1].

However, this liquidity comes with trade-offs. Secondary buyers often acquire common shares at a discount, whereas direct Pre-IPO investors secure preferred shares with liquidation preferences. In moderate exit scenarios, these preferences can claim 75% or more of the proceeds, leaving common shareholders with much smaller returns. To better assess potential outcomes, investors should request a detailed "waterfall" analysis that outlines returns under different scenarios[2].

Web3-Specific Use Cases

The dynamics of the secondary market are clearly illustrated in Web3 scenarios, where they play a key role in shaping exit strategies.

Take Circle‘s June 2025 NASDAQ IPO, for example. Before going public, Circle‘s shares traded on secondary platforms at valuations between $5.0 and $5.25 billion, with cumulative volumes reaching $110 million. The IPO itself was priced at $31 per share (around a $6.8 billion valuation), and shares later surged to over $200 each[4].

Kraken offers another example. Following its confidential IPO filing in early 2025, secondary market activity spiked. By June 30, 2025, Kraken‘s secondary shares were valued at roughly $6.82 billion, with $750 million in bids and trades over a 90-day span[4].

Additional data from the Web3 secondary market highlights broader trends. By May 2024, the total order book was valued at $668 million, with an average deal size of $3.9 million. Unlike traditional markets, where secondary demand focuses on companies nearing an IPO, 82% of offers in crypto private markets came from seed and pre-seed rounds[6][4].

The composition of assets is also shifting. In early 2025, SAFTs accounted for 54% to 59% of the market, while pure equity deals made up 32% to 34%. This balance began to shift after Circle’s IPO, reflecting a growing preference for equity as Web3 infrastructure and centralized finance projects prepare for public exits – a trend sometimes referred to as the "Circle Catalyst"[3][4].

sbb-itb-c5fef17

I Tried Buying Pre-IPO Shares on Hiive – Here’s What I Learned | Where to Buy Pre-IPO Stocks

2. Direct Pre-IPO Investments

Direct Pre-IPO investments operate differently from secondary markets, relying on institutional processes rather than market-driven pricing. These investments are shaped by detailed negotiations and structured financing rounds led by venture capital firms.

Pricing Dynamics

The pricing model for direct Pre-IPO investments is driven by institutional venture capital firms, not the push and pull of supply and demand. These firms conduct thorough due diligence and negotiate valuations during financing rounds. As part of these transactions, investors typically receive newly issued preferred shares. These shares come with added protections, such as liquidation preferences, anti-dilution clauses, and sometimes board representation. Investors may also secure information rights, granting access to financial reports, growth data, and strategic plans [1].

Unlike secondary market transactions, where money simply exchanges hands between investors, funds raised in direct Pre-IPO rounds go straight to the company to fuel its growth. This results in preferred shares often being priced higher than common shares. With companies remaining private for as long as 13 years, the importance of these Pre-IPO rounds has grown significantly [1].

Access and Barriers

Participation in direct Pre-IPO rounds is typically limited to institutional investors or strategic partners. These late-stage financing rounds, such as Series D or later, often require substantial minimum commitments – usually starting at $1 million or more. Additionally, these investments demand patience, with timelines stretching up to 10 years before liquidity is possible, usually through an IPO or acquisition.

For comparison, secondary markets offer shorter investment horizons. In fact, during the 12 months ending in June 2025, the total value of venture capital secondary transactions reached $61.1 billion, surpassing the $58.8 billion raised through VC-backed IPOs [11]. This contrast highlights the liquidity challenges inherent in direct Pre-IPO investments.

Liquidity Options

Liquidity in direct Pre-IPO investments is typically tied to major exit events, but structured solutions like company-sponsored tender offers have emerged as alternatives. These tender offers allow employees and early investors to sell shares back to the company at a predetermined price. This not only provides liquidity but also establishes valuation benchmarks without the unpredictability of open secondary markets [5].

For instance, SpaceX conducted a tender offer in late 2024 and early 2025, buying back $1.25 billion worth of shares from employees. This approach gave stakeholders liquidity while maintaining control over the company’s equity. Such methods, often referred to as part of the "Liquidity Stack", prioritize secondary sales and tender offers, with IPOs reserved for favorable market conditions [5].

"The market will fund quality, but it will not subsidize ambiguity." – Foley & Lardner [5]

Web3-Specific Use Cases

Web3 companies face unique hurdles when it comes to Pre-IPO valuations. Their revenue multiples – typically between 1.5x and 3x – are lower than those seen in sectors like AI or SaaS, which range from 3x to 5x. This discrepancy stems from factors like regulatory uncertainty, risks associated with smart contracts, and revenue volatility tied to token prices [12].

Investors need to carefully evaluate revenue sources, distinguishing between stable, recurring income (like SaaS subscriptions or API fees paid in stablecoins) and revenue from token incentives, which may be heavily discounted – sometimes by as much as 50% to 70% [12]. Additionally, securing a top-tier smart contract audit from firms like OpenZeppelin or Trail of Bits can boost a Web3 company’s valuation by up to 30%, as it reduces technical risks [12].

After Circle’s June 2025 IPO, the Web3 investment landscape began shifting. Equity structures started to dominate as infrastructure projects moved closer to public exits. This shift marked a departure from earlier token-centric models, reflecting a more mature approach to Pre-IPO valuations [3][4].

"A protocol with $50M TVL but $100K annual revenue is valued on the $100K, not the TVL." – Victor Raphael, CEO, ReFi Ventures [12]

Pros and Cons

In the dynamic world of Web3, understanding the trade-offs between secondary markets and direct Pre-IPO investments is essential for making informed decisions about investor strategies. Each option comes with its own set of advantages and limitations, shaping its suitability for different types of investors.

Secondary markets offer more accessible entry points, particularly through SPVs (special purpose vehicles), which allow accredited investors to gain exposure to late-stage companies with lower capital requirements [2]. This broader access has helped open doors for a wider range of participants. However, one of the key challenges is pricing. Shares in secondary markets are often traded through fragmented negotiations rather than centralized exchanges, leading to a lack of pricing clarity [1]. Additionally, buyers frequently face information gaps, as they typically don’t have access to up-to-date financial or operational details about the companies they’re investing in [1].

On the other hand, direct Pre-IPO investments provide greater transparency and governance. Institutional investors in this space often receive preferred shares, which come with liquidation preferences and enhanced information rights, offering a clearer view of a company’s financial health and strategic direction [1]. But this heightened level of access comes with a steep price – both literally and figuratively. Capital is locked in until the company reaches an exit event, such as an IPO or acquisition. Considering the median time to IPO is around 13 years after a company’s founding, this long-term commitment is typically out of reach for all but institutional investors, venture capital firms, and ultra-high-net-worth individuals who can afford the substantial capital requirements [1].

The liquidity difference between these two options is particularly striking. Secondary markets serve as occasional "release valves" for investors, with U.S. venture secondary trading volume projected to hit $106.3 billion by 2025 [7]. In contrast, direct investments offer little to no liquidity until a major event, unless the company itself organizes a tender offer. Another important distinction lies in the type of shares being purchased. Secondary market transactions generally involve common stock, which sits at the bottom of the liquidation hierarchy. Meanwhile, direct investments often involve preferred shares, which include protections against downside risk. This difference in share class explains why common stock typically trades at a discount of 20%–80% compared to preferred shares [2].

Here’s a quick comparison of the two approaches:

| Feature | Secondary Market Investment | Direct Pre-IPO Investment |

|---|---|---|

| Pricing Transparency | Low; fragmented platforms, supply-demand driven [1] | High; determined by the company and lead VCs [1] |

| Investor Access | Accessible to accredited individuals via platforms (e.g., EquityZen, Forge) [2] | Limited to institutional investors, VCs, and ultra-high-net-worth individuals [2] |

| Liquidity | Moderate; periodic opportunities via platforms/tenders [5] | Low; funds locked until IPO or acquisition [9] |

| Information Rights | Limited; often outdated or incomplete [1] | Comprehensive; includes board insights and audits [1] |

| Suitability | Ideal for accredited retail investors with smaller capital [2] | Best for institutional investors seeking governance and large share blocks [2] |

"The secondary market has matured significantly, moving away from the ‘Wild West’ era of 2021." – Calcix Research Team [10]

Ultimately, the choice between these two investment paths depends on individual goals, risk tolerance, and the desired level of involvement in governance and liquidity. Each approach caters to distinct strategies, offering different trade-offs for investors.

Conclusion

Deciding between secondary market opportunities and direct Pre-IPO investments comes down to your financial resources, risk appetite, and investment timeline. Secondary markets have made it easier for accredited investors to gain exposure to late-stage private companies, often with minimum investments starting at $10,000–$25,000. On the other hand, direct Pre-IPO investments typically demand a higher commitment – $100,000 or more – along with legal costs ranging from $25,000 to $30,000 per transaction [2].

For accredited retail investors with smaller budgets, secondary markets offer a more accessible way to invest in high-growth Web3 companies. However, these opportunities come with challenges, such as limited access to company information and potential Right of First Refusal (ROFR) clauses that could block transactions. Before investing, it’s crucial to research a company’s ROFR history and analyze its liquidation preference waterfalls to get a clear picture of what common shareholders might expect in different exit scenarios [2].

Meanwhile, institutional and ultra-high-net-worth investors willing to meet the higher capital requirements of direct Pre-IPO rounds often benefit from preferred shares, which provide downside protection, greater access to information, and opportunities for governance involvement. But these perks come with a trade-off: illiquidity. Funds are generally tied up until an exit event, and the median time to IPO can range from 10 to 16 years [8][11].

These considerations become even more critical in the ever-evolving Web3 space. With 64% of secondary deals in H1 2025 priced below earlier funding rounds, conducting a rigorous analysis of company fundamentals is essential [4]. The volatility and potential of the Web3 sector demand careful evaluation of valuations and pricing dynamics, reinforcing the importance of understanding both the risks and the rewards of each investment path.

"The market will fund quality, but it will not subsidize ambiguity." – AdValorem Research [5]

Whether you prioritize the accessibility and liquidity of secondary markets or the control and transparency of direct Pre-IPO investments, your strategy should align with your financial goals and risk tolerance. Both options require thorough due diligence, realistic expectations about liquidity, and a clear understanding of the inherent risks in private market investments.

FAQs

How can I tell if a secondary discount is a good deal?

When considering whether a secondary discount is worth pursuing, it’s essential to compare it against recent valuation rounds. This helps determine if the discount represents genuine value or underlying risk. Discounts around 45% or higher could signal a potential opportunity, but significantly steeper reductions might raise red flags about the company or the broader market.

To make an informed decision, take a closer look at several factors:

- Sector and Stage: Consider the industry and the company’s current growth phase to understand the context of the discount.

- Terms: Pay attention to specific conditions, like lock-up periods, which can affect liquidity and timing.

- Bid-Ask Spread: A wide spread could indicate uncertainty or low demand, which may warrant caution.

Ultimately, ensure the discount reflects strong fundamentals rather than signs of distress.

What should I ask for to reduce info gaps in a secondary purchase?

To bridge information gaps, request detailed valuation metrics and contextual data. This includes the company’s most recent funding round valuation, any discounts or premiums applied, and liquidity factors. It’s also helpful to inquire about the valuation methodology, recent comparable transactions, and any lock-up or transfer restrictions that might apply. Typical discounts, such as 25%-45% off the last funding valuations, can provide a clearer picture of fairness and guide more informed decision-making.

How do liquidation preferences change my payout vs common stock?

Liquidation preferences determine how proceeds are divided during events like acquisitions or IPOs. Essentially, they ensure that preferred stockholders get paid first – usually their initial investment or a multiple of it – before common stockholders see any returns. This setup offers a layer of protection for preferred investors, but it can limit what common stockholders receive if the company’s valuation doesn’t surpass the preference thresholds. On the flip side, if the valuation exceeds those thresholds, preferred shareholders can also participate in the extra proceeds.