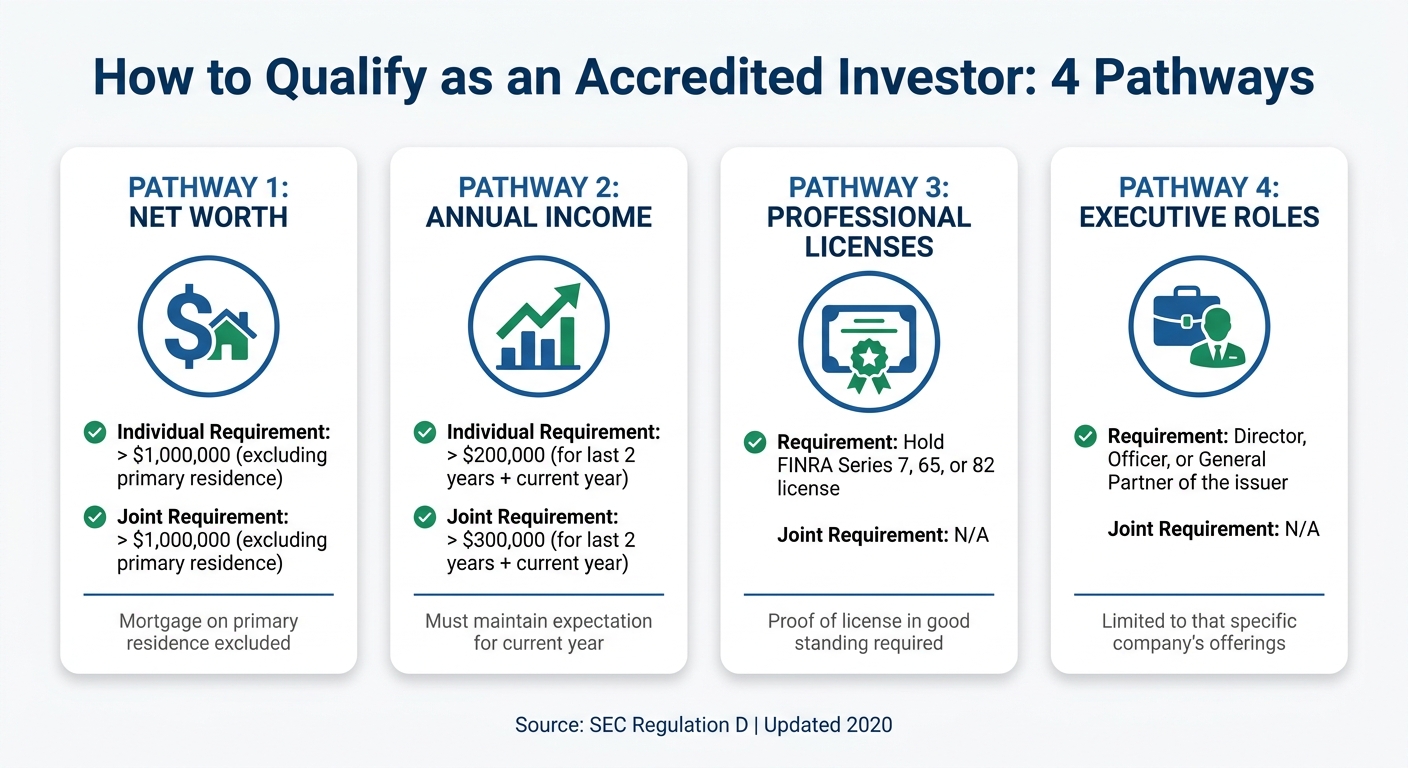

To qualify as an accredited investor and access pre-IPO investment opportunities, you need to meet specific financial or professional criteria set by the SEC. These include:

- Net Worth: Over $1,000,000 (excluding your primary residence).

- Income: $200,000+ annually ($300,000+ with a spouse) for the past two years and the current year.

- Professional Licenses: Holding FINRA Series 7, 65, or 82 licenses.

- Executive Roles: Being a director, officer, or general partner of the company issuing securities.

Verification involves providing documents like tax returns, bank statements, or proof of licenses. Rule 506(c) offerings require stricter checks compared to Rule 506(b). Once verified, you can explore pre-IPO investments through platforms, funds, or syndicates, but these carry risks like illiquidity and lack of transparency.

Key Takeaways:

- Meet financial or professional benchmarks.

- Verify status with documents or third-party services.

- Understand risks, including potential loss and long lock-up periods.

Preparation and due diligence are critical to navigating pre-IPO investments.

Accredited Investor SEC Definition: Are YOU Eligible?

sbb-itb-c5fef17

Financial Requirements for Accredited Investor Status

Accredited Investor Qualification Requirements: 4 Ways to Qualify

The SEC has established specific financial benchmarks to determine who qualifies as an accredited investor. These benchmarks can be met through net worth, income, or certain professional credentials.

Net Worth Threshold

To qualify via net worth, an individual (or a couple combining their assets) must have a net worth exceeding $1,000,000, excluding the value of their primary residence [2][5].

Net worth is calculated by adding up all assets - such as bank accounts, retirement funds, investments, and personal property - and subtracting liabilities like student loans, car loans, and credit card debt [7]. A mortgage on your primary residence generally isn’t factored in as a liability if the home has positive equity. However, if the mortgage exceeds the home’s value, the excess debt is counted as a liability [6].

One important caveat: Any debt increases, like a home equity line of credit taken out within 60 days before an investment, count as liabilities. This rule is designed to prevent artificially inflating net worth [6].

If net worth isn’t the right avenue for you, income qualifications might be another option.

Income Threshold

Income can also serve as a qualification. To meet this requirement, an individual must earn more than $200,000 annually, or a combined income of over $300,000 with a spouse or spousal equivalent (a cohabitant in a relationship similar to a spouse) [2][5]. This income level must have been achieved in each of the last two years, with a reasonable expectation of maintaining it in the current year [2].

If neither net worth nor income criteria apply, professional credentials or executive roles offer alternative pathways.

Professional Licenses and Executive Positions

In 2020, the SEC expanded the definition of accredited investors to include those who demonstrate financial expertise through professional licenses or executive roles, acknowledging that wealth alone isn’t the only measure of financial sophistication [5][8].

Holding specific FINRA licenses - such as the Series 7 (General Securities Representative), Series 65 (Investment Adviser Representative), or Series 82 (Private Securities Offerings Representative) - automatically qualifies you, even if you don’t meet net worth or income benchmarks [2][8].

“For the first time, individuals will be permitted to participate in our private capital markets not only based on their income or net worth, but also based on established, clear measures of financial sophistication.”

- Jay Clayton, Chairman, SEC [5]

Additionally, if you serve as a director, executive officer, or general partner of a company issuing securities, you qualify as an accredited investor for that specific offering [2][8]. However, this status is limited to transactions involving your own company and doesn’t extend to other investment opportunities [8][4].

| Qualification Category | Individual Requirement | Joint Requirement (with spouse or equivalent) |

|---|---|---|

| Net Worth | > $1,000,000 (excluding primary residence) | > $1,000,000 (excluding primary residence) |

| Annual Income | > $200,000 (for last 2 years + current year) | > $300,000 (for last 2 years + current year) |

| Professional Licenses | Series 7, 65, or 82 | N/A |

| Executive Roles | Director, Officer, or GP of the issuer | N/A |

How to Verify Your Accredited Investor Status

Once you’ve determined that you meet the criteria to qualify as an accredited investor, the next step is verification. This process is essential for gaining access to pre-IPO investment opportunities. The method of verification depends on whether the investment falls under Rule 506(b) or Rule 506(c).

Under Rule 506(b), the process is relatively simple. Issuers rely on the “reasonable belief” that you meet the accredited investor criteria. This typically involves completing a self-certification form or subscription agreement [11]. In most cases, checking a box to confirm your status is sufficient.

Rule 506(c), on the other hand, has stricter requirements. Since this rule allows issuers to publicly advertise their investment offerings, the SEC mandates “reasonable steps” to verify your accredited status independently [10][11]. This means you’ll need to provide supporting documents or use a verification service.

According to SEC guidance issued in March 2025, issuers may accept self-certification for Rule 506(c) offerings if you invest at least $200,000 as an individual (or $1,000,000 as an entity) and the investment is not financed by a third party [13][15]. To make the process smoother, it’s helpful to know what documents are required.

“The Rule 506(c) reasonable steps obligation is the issuer’s responsibility, and the issuer’s reliance on a third-party verification service is itself part of the issuer’s reasonable steps analysis.”

- Alex Lubyansky, M&A Attorney, Acquisition Stars [10]

Documents You’ll Need

For income-based verification, you’ll need IRS forms from the two most recent tax years, such as W-2s, 1099s, Schedule K-1s, or Form 1040. Additionally, you’ll need to submit a written statement confirming that you expect to maintain the same income level in the current year [10][11][14].

For net worth verification, gather documentation of your assets. This might include bank statements, brokerage account statements, certificates of deposit, property tax assessments, or independent appraisals. You’ll also need a consumer credit report from Equifax, Experian, or TransUnion, dated within the last 90 days, to verify your liabilities [10][11][14].

If you hold a Series 7, 65, or 82 license, you can simply provide proof of your license in good standing through FINRA BrokerCheck [10][11][14].

Another option is using the professional letter safe harbor. A licensed attorney, CPA, SEC-registered investment adviser, or registered broker-dealer can provide a written confirmation that they verified your status within the last 90 days [10][11][12]. This approach is ideal if you’d prefer not to share sensitive financial documents directly with an issuer.

If you’d like to streamline the process, you can also turn to trusted third-party verification platforms.

Using Third-Party Verification Services

Third-party services simplify the verification process by reviewing your documents and issuing a verification letter or reusable Investor Passport. These platforms employ licensed professionals - such as attorneys, CPAs, or registered investment advisers - to ensure compliance with SEC standards [16][17][18].

To use these services, you’ll typically register on the platform (often through a link provided by the issuer), select your verification method (income, net worth, or professional license), upload your documents, and wait for approval. The process usually takes 12 to 48 hours and costs between $50 and $150 per individual. However, many issuers cover the fee [16][17][18][19].

“The SEC does not certify you as an accredited investor, nor can you apply to them to get a certification.”

Third-party services not only protect your privacy but also save you from repeatedly submitting sensitive documents to multiple issuers. If you’re reinvesting with the same issuer, you may even be able to reuse a previous verification for up to five years, provided your financial situation hasn’t changed significantly [19].

Where to Find Pre-IPO Investment Opportunities

Once your accredited investor status is verified, the next step is identifying pre-IPO deals. By early 2026, late-stage private companies were valued at over $3 trillion in market capitalization [20]. Companies such as SpaceX, OpenAI, and Stripe remain private longer, offering growth opportunities that were once exclusive to public markets [20].

Access to these opportunities has expanded, no longer limited to institutional investors or the ultra-wealthy. Accredited investors now have several avenues to explore, depending on their investment size, risk appetite, and level of involvement.

Secondary Market Platforms

One popular route to pre-IPO shares is through secondary market platforms. These platforms connect sellers - like employees, founders, or early investors - with accredited buyers. They generally operate under two main models:

- Fund-based models: These pool multiple investors’ capital into a Special Purpose Vehicle (SPV), often structured as a Delaware LLC, to hold shares in a private company. For example, platforms like EquityZen offer minimum investments ranging from $10,000 to $25,000. SPV managers typically charge a carried interest of 10%–20% on profits at exit [20].

- Marketplace models: These facilitate direct share purchases. Forge Global, a publicly traded company (ticker: FRGE), is an example. It caters to institutional and high-net-worth investors, with minimum investments usually starting at $100,000 and transaction fees between 2% and 4%. While direct ownership provides shareholder control, it comes with fixed costs ranging from $5,000 to $15,000, making it better suited for larger investments [20][21].

A critical factor to keep in mind is the Right of First Refusal (ROFR). Companies can block secondary sales by either buying the shares themselves or letting existing investors acquire them. This can lead to delays, with many deals failing to close within the standard 6- to 8-week settlement period. Before committing, check if the company has a history of blocking transactions or is actively raising funds - both scenarios can increase the likelihood of ROFR issues [20][21].

“The Right of First Refusal represents the single most significant operational difference between public and private market transactions.”

- AltStreet [20]

Secondary shares often trade at 120%–150% of a company’s 409A valuation (the tax-driven floor) but at a discount compared to prices paid by venture capitalists during preferred funding rounds. In Q1 2025, secondary shares were discounted by an average of 20% relative to the last funding round [21].

Late-Stage Venture Capital Funds

For those looking for diversification, late-stage venture capital funds offer exposure to a broader portfolio of private companies - typically two or more years before their IPO [9]. Unlike SPVs, which focus on a single company, these funds spread investments across 10 to 20 or more companies, reducing the risk tied to a single entity [21]. Managed by professionals who handle due diligence and performance monitoring, they provide indirect access to pre-IPO opportunities. For instance, Sutter Rock Capital, a Nasdaq-listed firm, invested in companies like Spotify and Dropbox years before their IPOs [9].

These funds are structured in two main ways:

- 3(c)(1) funds: These are limited to 100 accredited investors (or up to 250 if the fund size is under $12 million).

- 3(c)(7) funds: These accept up to 2,000 qualified purchasers, typically individuals with at least $5 million in investments [4].

The fee structure for these funds often follows the “2 and 20” model - charging a 2% annual management fee plus 20% carried interest on profits [21]. However, investments are usually locked up for 1 to 5 years due to the illiquid nature of pre-IPO shares [3][9].

Angel Syndicates and SPVs

Angel syndicates and SPVs (Special Purpose Vehicles) are other collective investment options for pre-IPO deals. In an SPV, investors buy membership interests in a vehicle that appears as a single entity on the company’s capitalization table [9]. Syndicates, on the other hand, are typically led by experienced investors who source deals, negotiate terms, and manage the investment on behalf of participants. This model provides access to opportunities that might not be available to individual investors. Platforms like Augment and AngelList made it possible to access late-stage growth companies through both direct marketplaces and collective investment vehicles in early 2025 [4][22].

Setting up an SPV involves upfront costs - legal, compliance, and banking fees - which generally range from $10,000 to $20,000. These costs are shared among participants [20]. It’s important to consider how these fees may impact your net returns, especially over time. While syndicates often provide access to exclusive deals through the lead investor’s network, they also require a passive role, as the manager controls voting and exit decisions. Evaluating the lead’s track record and fee structure is essential before participating.

How to Evaluate Pre-IPO Investment Opportunities

Evaluating pre-IPO shares demands a deeper dive into financials, capital structure, and liquidity than analyzing publicly traded stocks. Unlike public companies, private firms don’t provide quarterly earnings reports or SEC filings, so transparency is limited. To make informed decisions, you’ll need to thoroughly assess financial data and understand how your shares fit into the broader capital structure. This groundwork is essential for navigating liquidity and legal challenges, which are covered in the next sections.

Analyzing Company Performance and Growth

Start by comparing the price venture capitalists (VCs) paid in the last funding round to the company’s 409A valuation. Typically, this gap falls between 50% and 80%. A wider gap often indicates that VCs paid a premium for preferred stock rights that common shareholders won’t receive.

Don’t let headline valuations mislead you. Instead, use a combination of the 409A valuation, Tape D marks (which reflect how mutual funds value their private holdings), and recent secondary market prices to get a clearer picture of market dynamics. For example, in early 2026, SpaceX common shares traded at around $85.00 on secondary markets - a 23% discount to the Series J preferred price of $110.00, even though the 409A valuation floor was just $45.00 [20]. This pricing disparity highlights the real supply-demand dynamics and the lack of protective rights tied to common stock.

Run exit scenarios to gauge potential returns. For moderate exits, liquidation preferences can consume more than 75% of the proceeds before common shareholders see any benefit [20]. Calculate how much your shares could be worth at various exit valuations - $500 million, $1 billion, $5 billion - to determine where the upside becomes meaningful.

Liquidity Constraints and Lock-Up Periods

Pre-IPO shares are not easily sold. You should be prepared for your investment to remain locked up for 1 to 5 years, or even longer [3]. Unlike public stocks that can be sold instantly, private shares require company approval, waivers for the Right of First Refusal (ROFR), and lengthy settlement processes. Many transactions fail to close due to ROFR exercises, board rejections, or valuation changes during the 30–60 day approval period [20].

“Many pre-IPO transactions never close. Companies exercise Right of First Refusal. Boards block transfers. Valuations move against buyers during extended approval periods.” - AltStreet [20]

Investigate the company’s track record regarding secondary sales. Some companies are “ROFR-friendly” and routinely approve transfers, while others actively block them, particularly during fundraising rounds when existing investors may want to buy those shares themselves. This information can often be found in platform deal notes or by consulting the broker directly. If the company is raising new capital, expect delays or outright denials.

Understanding these liquidity challenges is critical as you move on to review the legal framework.

Legal and Compliance Review

Beyond pricing and liquidity, the legal structure of your investment plays a major role in your potential outcomes. Before committing funds, examine the capitalization table to understand the “preference stack.” This outlines how much money must be returned to preferred shareholders (like VCs) before common shareholders receive any returns [20]. Pay close attention to the differences between share classes - common stock typically lacks the liquidation preferences, anti-dilution protections, and board representation that preferred stockholders enjoy [20].

Confirm whether you’re purchasing shares directly or through a Special Purpose Vehicle (SPV). Direct purchases provide voting rights and control but come with legal fees ranging from $10,000 to $15,000 [20]. SPVs lower the entry cost to $10,000–$25,000 but introduce additional fees and K-1 tax complexities [20]. Knowing exactly what you’re buying and how it fits into your portfolio is essential.

Look out for side letters, which are special agreements granting certain investors extra rights beyond standard documents [4]. These can significantly impact your position in the capital structure. Just as verifying your accredited status is crucial, a thorough legal review of documents like the Stock Purchase Agreement, Investor Rights Agreement, and any ROFR waivers is equally important. Consulting legal counsel ensures your pre-IPO investment is sound [20].

Accreditation for Trusts and Institutions

Trusts, pension plans, and foundations can access pre-IPO opportunities, but their qualification criteria differ from those for individual investors. Instead of meeting income or net worth benchmarks, these entities must demonstrate sufficient assets and, in some cases, advanced financial management capabilities. Knowing these requirements can help ensure your entity is eligible to participate in private investment opportunities. Here’s a breakdown of the key criteria:

Trust Accreditation Requirements

For a trust to qualify as an accredited investor, it must hold assets exceeding $5,000,000 [2]. Additionally, the trust’s investments must be managed by someone with proven financial and business expertise [2].

However, there’s a critical condition: the trust cannot be formed solely to acquire the securities being offered [5]. If a trust is created specifically for investing in a particular pre-IPO deal, it will not qualify, regardless of its asset size.

Revocable trusts have another option for accreditation. If all grantors of the trust are accredited individuals, the trust can qualify without needing to meet the $5,000,000 asset threshold [23]. On the other hand, irrevocable trusts typically must meet the $5,000,000 asset requirement [23].

To verify accreditation, you’ll need to provide documentation such as a letter from a licensed CPA, attorney, or SEC-registered investment advisor confirming the trust’s status [23]. Additional documents, like brokerage statements, bank statements, or tax records, may also be required to prove the asset threshold [1].

Institutional Entity Requirements

Institutional entities - including pension plans, employee benefit plans, 501(c)(3) foundations, corporations, partnerships, and LLCs - qualify as accredited investors if they hold assets exceeding $5,000,000 [2]. Similar to trusts, these entities cannot be established solely for the purpose of acquiring the offered securities [5].

The SEC expanded the definition of accredited entities in 2020 to include a broader category. This includes governmental bodies, Indian tribes, and family offices, provided they own over $5,000,000 in investments and were not formed specifically for the investment [5]. Family offices must manage a minimum of $5,000,000 to qualify.

Certain financial institutions, such as banks, insurance companies, registered investment companies, and business development companies, automatically qualify under long-standing SEC definitions, regardless of their asset size [2].

When it comes to verification, entities may provide audited financial statements, tax returns, or brokerage records [1]. Alternatively, a confirmation letter from a registered broker-dealer, SEC-registered investment adviser, licensed attorney, or CPA can streamline the process. This method is especially useful for Rule 506(c) offerings, which require issuers to take reasonable steps to verify investor status [1].

“Self-certification by the investor alone (by checking a box) without the company having any other knowledge of the investor’s financial circumstances or sophistication is not sufficient to meet either the ‘reasonable belief’ standard or the ‘reasonable steps to verify’ requirement.” - SEC.gov [1]

Keeping your documentation current is essential. Under Rule 506(c), a written representation from a previously verified investor can remain valid for up to five years, provided the company has no conflicting information [1]. This means that once your status is verified, future pre-IPO investments may involve less administrative effort.

Conclusion

Becoming an accredited investor opens the door to pre-IPO opportunities, but it starts with meeting specific criteria like earning over $200,000 annually, holding a net worth exceeding $1 million (excluding your primary residence), or possessing a Series 7, 65, or 82 license [2]. However, this financial qualification is just the beginning.

Verification is a critical step, serving as a regulatory safeguard for both investors and issuers. Under Rule 506(c), the SEC mandates verified documentation rather than relying on self-certification [1]. As the SEC emphasizes:

“Self-certification by the investor alone (by checking a box) without the company having any other knowledge of the investor’s financial circumstances or sophistication is not sufficient to meet either the ‘reasonable belief’ standard or the ‘reasonable steps to verify’ requirement” [1].

Once your accredited status is verified, the real challenge begins: conducting thorough due diligence. Accreditation simply grants you access; it doesn’t eliminate the risks tied to pre-IPO investments. These deals often involve capital lock-up periods ranging from one to ten years and come with significant uncertainties [3]. Without standardized disclosure requirements, it’s essential to dive deep into evaluating company performance, growth potential, and legal compliance. As highlighted earlier, this step is vital to making informed decisions.

Preparation is key. Start by organizing your documentation, understanding the risks and lock-up periods, and determining how much you’re willing to risk. If you’re new to this type of investment, it’s wise to begin with smaller commitments while getting familiar with the asset class. Accreditation may open the door, but it’s your research and decision-making that will ultimately shape your success in pre-IPO investing.

FAQs

Do I qualify if my net worth is $1,000,000 but most of it is home equity?

Under SEC guidelines, your primary residence doesn’t count toward the $1,000,000 net worth requirement to qualify as an accredited investor. This means if most of your wealth comes from home equity, you won’t meet the criteria. To qualify, your net worth - excluding the value of your primary home - must still total at least $1 million.

What’s the fastest way to verify accredited status for a Rule 506(c) deal?

The simplest and fastest way to verify accredited status for a Rule 506(c) offering is through self-certification, as outlined in recent SEC guidance. This approach lets investors confirm their status without needing to provide extensive documentation right away, making the process much more straightforward.

While traditional methods - such as submitting tax returns or bank statements - are still an option, self-certification cuts down on the time and effort required for approval.

How can I reduce risk when buying pre-IPO shares?

Investing in pre-IPO shares can be risky, so it’s crucial to do your homework. Start by conducting thorough due diligence to confirm the company’s credibility and fully understand the terms of the deal. Keep in mind that pre-IPO investments often involve unregistered securities, which adds another layer of risk.

This type of investment is typically open to accredited investors - those who meet specific income or net worth requirements. If you’re considering this path, consulting with financial or legal professionals who specialize in pre-IPO deals can be incredibly helpful. Their expertise can guide you through the process and help you navigate potential risks more effectively.

Related Blog Posts

- 7 Key Metrics for Evaluating Web3 Investment Opportunities

- Institutional Strategies for Digital Asset Portfolios

- How Liquid Staking Meets Institutional Compliance

- How to Structure Token Purchase Agreements for Web3 Deals