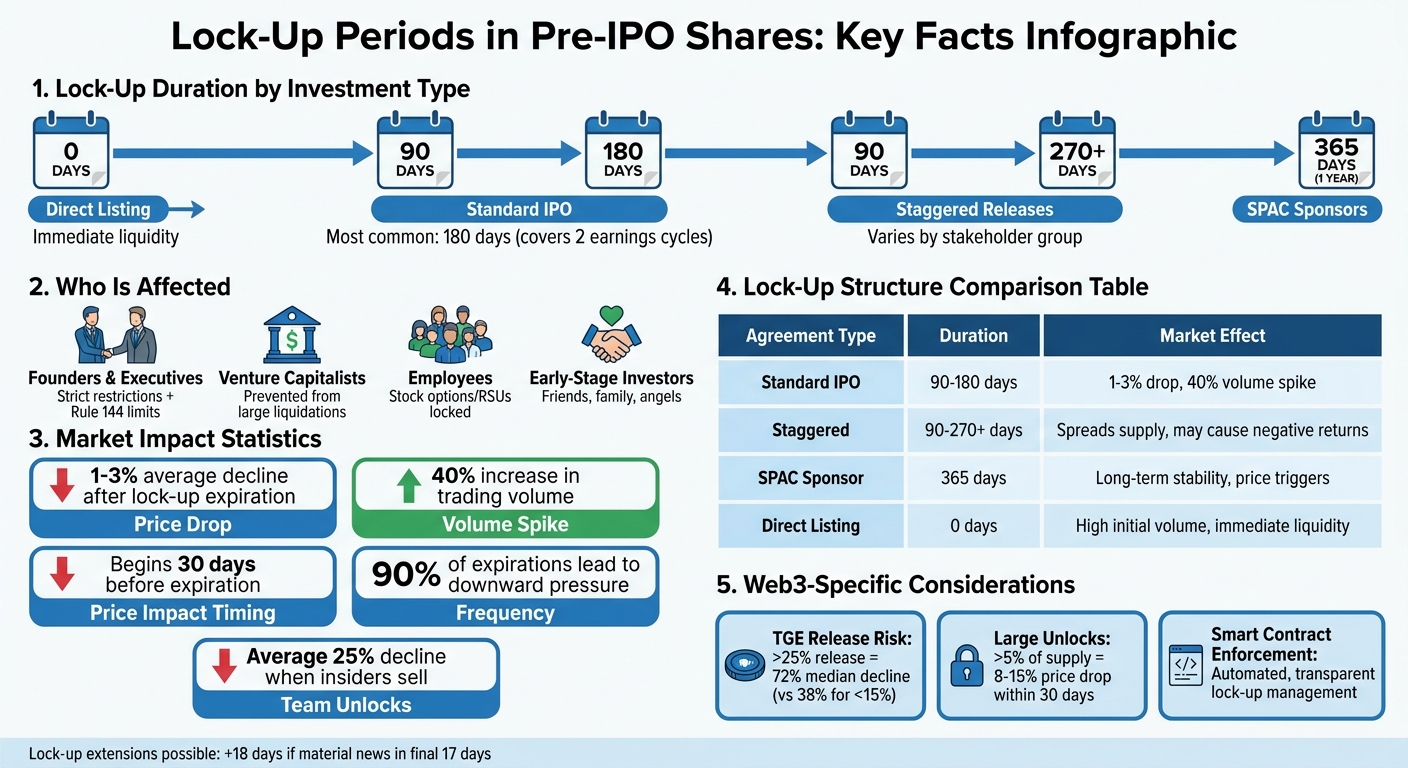

Lock-up periods are agreements that restrict insiders from selling their pre-IPO shares for a set time - usually 90 to 180 days after a company goes public. These restrictions aim to prevent a flood of shares hitting the market, which could lower stock prices. For SPACs, these periods can extend to 12 months.

Key points:

- Who is affected? Founders, executives, venture capitalists, employees, and early investors.

- Typical duration: 90–180 days for IPOs; 365 days for SPACs.

- Market impact: Share prices often drop 1–3% after lock-up expirations, with trading volume spiking by 40%.

- Structures: Standard lock-ups release all shares at once, while staggered agreements spread out selling dates.

In Web3 investments, smart contracts enforce lock-ups, and token liquidity is often tied to vesting schedules. Investors should monitor unlock dates, assess token release percentages, and diversify to manage risks effectively.

Understanding lock-up terms in SEC filings and planning around expiration dates can help you protect your investments and time your trades wisely.

Lock-Up Period Duration and Market Impact by Investment Type

Wall Street’s Plan to Stop an IPO Crash

sbb-itb-c5fef17

What Are Lock-Up Periods and Why Do They Matter?

A lock-up period is a predetermined timeframe - usually lasting between 90 and 180 days after a company goes public - during which insiders and early investors are prohibited from selling their pre-IPO shares [4]. This restriction covers all equity acquired before the IPO and often includes limitations on hedging strategies like short-selling. While these agreements aren’t required by federal law or the SEC, they are negotiated between the company and its underwriters. The terms of such agreements are detailed in the company’s S-1 registration statement and prospectus, available on the SEC’s EDGAR database.

The primary purpose of lock-up periods is to maintain market stability and demonstrate confidence in the company’s future.

The Reason Lock-Up Periods Exist

Lock-up periods are designed to prevent excessive selling immediately after an IPO, which could destabilize the stock price. Without these restrictions, insiders might flood the market with shares, creating an imbalance between supply and demand and driving down the stock’s value.

“The restriction exists to prevent a flood of selling that would tank a freshly listed stock.” - LegalClarity Team [4]

Typically lasting 180 days, lock-up periods span two earnings cycles, giving the market time to stabilize before insiders are allowed to sell. Underwriters enforce these agreements to maintain investor trust and protect their reputations. Additionally, lock-up periods signal to the market that insiders are committed to the company’s long-term success, which can help build confidence among new investors.

Who Is Affected by Lock-Up Periods

Lock-up periods apply to several groups holding pre-IPO equity, including:

- Founders and Executives: Often holding large stakes, these individuals face strict restrictions.

- Venture Capitalists: Early-stage investors are prevented from dumping shares, which could destabilize the market.

- Employees: Those who received stock options or RSUs as part of their compensation must wait until the lock-up period expires to sell.

- Early-Stage Investors: Friends, family, and angel investors who participated in early funding rounds are also subject to these restrictions.

| Stakeholder Group | Typical Restriction Details |

|---|---|

| Founders & Executives | Restricted from selling shares until the lock-up ends; also subject to Rule 144 volume limits. |

| Venture Capitalists | Barred from liquidating large positions to avoid market disruption. |

| Employees | Cannot sell stock options or RSUs until the lock-up period concludes. |

| SPAC Sponsors | Often face extended lock-ups - up to 12 months or tied to specific price-based triggers. |

Even after the lock-up period ends, insiders are still bound by Rule 144, which limits sales to no more than 1% of the company’s outstanding shares or the average weekly trading volume over a three-month period [4].

In the next section, we’ll examine how the duration and structure of lock-up periods influence market behavior.

How Long Do Lock-Up Periods Last?

Now that we know who faces these restrictions, let’s dive into how long lock-up periods typically last and how they’re structured.

For pre-IPO lock-ups, the industry standard is usually 90–180 days, though specific offerings can tweak this timeline. The most common duration - 180 days - covers two earnings cycles, giving investors enough time to assess the company’s performance without being influenced by insider actions.

“The 180-day standard has become industry convention because it roughly spans two earnings cycles, giving investors enough financial data to form independent views on the company’s value.” – LegalClarity Team [4]

However, not all lock-up periods are created equal. Traditional IPOs stick to the 180-day guideline, while SPAC sponsors face a longer restriction of 365 days. On the other hand, direct listings allow insiders to sell their shares immediately [4].

There’s also a clause that can extend the lock-up period. If material news comes out during the final 17 days of the lock-up, an automatic extension of 18 days might kick in. That means a 180-day lock-up could stretch to 198 days in some cases [4].

Standard vs. Staggered Lock-Up Agreements

The type of lock-up agreement - whether standard or staggered - plays a big role in how the market reacts when restrictions lift.

Standard agreements have one expiration date for everyone, including founders, employees, and venture capitalists. When the lock-up ends, all insiders can sell at once, often leading to a surge in trading volume and potential price drops. This concentrated selling event can create significant volatility.

Staggered agreements, by comparison, space out the release dates for different groups. For example, employees might get to sell after 90 days, venture capitalists after 180 days, and founders after 270 days [4]. While this approach aims to ease the selling pressure, research shows that staggered releases can still lead to negative abnormal returns, sometimes even worse than single-expiration agreements [2].

Here’s a quick breakdown of how different agreements and durations impact the market:

| Agreement Type | Typical Duration | Affected Shareholders | Market Effect |

|---|---|---|---|

| Standard IPO | 90–180 days | Founders, VCs, Employees | Potential 1–3% price drop; 40% volume spike [4] |

| Staggered | 90, 180, to 270+ days | Different classes of insiders | Spreads out supply; may still cause negative returns [2] |

| SPAC Sponsor | 365 days (1 year) | SPAC Sponsors/Founders | Long-term stability; often includes price triggers [4] |

| Direct Listing | 0 days (None) | All existing shareholders | High initial volume; immediate liquidity [4] |

Some companies also build in performance-based triggers, allowing insiders to sell early if the stock price remains above a certain level for a set period [4].

Next, we’ll look at how these lock-up structures and durations impact share prices and overall liquidity.

How Lock-Up Expiration Affects Share Prices and Liquidity

When lock-up periods end, share prices often take a hit. On average, prices drop between 1–3% as the market is flooded with newly tradable shares [6]. Research indicates that 90% of these expirations lead to downward price pressure, regardless of the size of the unlock or who is doing the selling [8].

Interestingly, the price impact doesn’t wait until the actual expiration date. It can start as early as 30 days before the lock-up ends [8]. Sophisticated investors often begin hedging their positions two to four weeks in advance, using tools like market makers to prepare for the increased supply. Meanwhile, retail investors tend to sell their shares closer to the expiration date, usually within the final week, fearing dilution. This dynamic contributes to the early price decline [8].

Once the lock-up ends, the identity of those selling shares becomes a key factor in market reactions. For example, team unlocks - when company insiders sell their shares - can be particularly disruptive, often causing average declines of 25% [8]. This is because team members often sell for personal financial reasons, and their sales usually lack a coordinated strategy. On the other hand, institutional investors tend to manage their sales more strategically, using derivatives, options, or over-the-counter (OTC) desks to minimize market disruption. Traders also play a role, increasing short positions as the expiration date nears. In some cases, this can trigger a short squeeze if selling intensifies [6][8].

Price Changes After Lock-Up Periods End

The effects of lock-up expirations vary widely, as seen in recent examples:

- Figure (FIGR), a blockchain-focused fintech company, saw its stock price soar 61.40% after its lock-up expired. The IPO price of $25.00 jumped to $40.35, fueled by strong financials, including a rise in net income from $27.3 million to $89.6 million, and a growing loan portfolio [7].

- Gemini (GEMI), however, experienced a sharp decline. Its stock plummeted 57.79%, falling from its $28.00 IPO price to $11.82. Although the company reported 53% revenue growth year-over-year, it remained unprofitable, which raised concerns among investors after the lock-up ended [7].

“The post-IPO period acts as a critical filter. It separates short-term interest from long-term investment rationale and highlights which companies are ready for the public markets.” – Regolith IPO Digest [7]

Some companies faced even more dramatic outcomes. For instance, American Bitcoin (ABTC), a Bitcoin mining firm, suffered a massive single-day crash in late 2025. Following the unlock of private placement shares from its merger with Gryphon Digital Mining, the stock dropped 38.83% in one trading session. During the first hour alone, shares plunged nearly 50%, falling from $3.58 to a low of $1.80 [9].

Here’s a quick snapshot of how various companies performed through their lock-up expirations:

| Company | Ticker | IPO Price | Price at Lock-Up Expiry | % Change | Sector |

|---|---|---|---|---|---|

| Figure | FIGR | $25.00 | $40.35 | +61.40% | Blockchain/Fintech |

| Legence | LGN | $28.00 | $42.04 | +50.14% | Infrastructure/Tech |

| Netskope | NTSK | $19.00 | $19.30 | +1.58% | Cloud Security |

| Klarna | KLAR | $40.00 | $31.70 | -20.75% | Fintech/Payments |

| American Bitcoin | ABTC | $3.58 | $2.19 | -38.83% | Bitcoin Mining |

| Gemini | GEMI | $28.00 | $11.82 | -57.79% | Crypto Exchange |

For investors, timing is everything. The data suggests it’s wise to sell shares about 30 days before a lock-up expiration to avoid pre-hedging pressure. Conversely, re-entering the market 14 days after the expiration can allow time for volatility to settle [8].

How to Navigate Lock-Up Periods in Web3 Investments

In the world of Web3, lock-up periods require a tailored approach. Thanks to blockchain transparency and smart contracts, managing these restrictions becomes more structured. These strategies build on earlier discussions about how lock-ups impact markets.

Managing Liquidity Restrictions

Lock-up periods limit liquidity, so understanding these constraints while maintaining portfolio flexibility is crucial. Typically, equity vests over four years pre-IPO, while lock-up periods post-IPO or post-token-launch generally last 90–180 days, preventing immediate sales [5]. In Web3, smart contracts often enforce these restrictions, releasing tokens only when specific conditions - like timeframes or project milestones - are met [10].

“Token lockup promotes a commitment to the project’s future rather than short-term gains, aligning holders’ interests with the project’s ambitions.” – Bitzo [10]

To navigate limited liquidity during lock-ups, diversification is key. Spread investments across projects with different unlock schedules to avoid overlapping dates [14]. Another option is engaging with DeFi protocols. While your primary holdings remain locked, you can use decentralized finance platforms to earn utility tokens by providing liquidity or lending [11]. Additionally, OTC trading services like those from Bestla VC offer liquidity access without waiting for lock-up expirations, all while minimizing counterparty risks.

Before investing, always verify lock-up terms. Tools like Etherscan can confirm that tokens are locked until the specified date [12]. Platforms such as CoinMarketCap and CoinGecko also help monitor token allocation, distribution transparency, and upcoming unlock schedules [11].

Timing Your Investments and Assessing Risk

Proper timing is essential to reducing risk and managing liquidity restrictions. One critical factor is the percentage of tokens released during the Token Generation Event (TGE). Projects releasing over 25% of tokens at TGE often experience a median first-year decline of 72%, compared to 38% for projects with unlocks below 15% [13]. Avoid projects where a single month adds more than 2–3% to the circulating supply [13].

Track all major unlock events during the first two years of any Web3 project. Large unlocks - those exceeding 5% of circulating supply - are typically linked to an 8–15% price drop within 30 days of the event [13]. Use platforms like TokenUnlocks, CryptoRank, or DefiLlama to monitor real-time supply changes and adjust your positions accordingly [14].

Pay close attention to the project’s vesting curve. Linear curves are predictable and carry lower risk. S-curves reward long-term holders, while logarithmic curves, which front-load token releases, often suggest short-term thinking and come with higher risk [13]. Poor vesting structures have been linked to 40–60% greater first-year price volatility [13].

For institutional investors and insiders, Rule 10b5-1 trading plans can simplify navigating trading windows and blackout periods [5]. These pre-arranged plans allow for scheduled stock sales during lock-up periods, offering a legal safeguard against insider trading accusations while enabling gradual liquidity [3][4]. However, even after lock-ups end, SEC Rule 144 limits sales to the greater of 1% of outstanding shares or the average weekly trading volume [4].

Lastly, keep an eye out for voluntary lock-up extensions from project teams or major VCs. These extensions often signal long-term commitment and can ease negative price sentiment [14]. On the flip side, if a project lacks verifiable on-chain proof of locks, consider it a warning sign [12].

“Locking seed round and investor tokens on-chain closes that gap [the trust gap] permanently.” – StakePoint Team [12]

Web3 and Blockchain Pre-IPO Lock-Up Examples

These examples shed light on how adjustments to lock-up terms can directly impact token liquidity and market perception. By examining specific Web3 projects, we can see how lock-up periods influence token pricing and investor behavior.

In July 2024, Worldcoin extended the unlock schedule for 80% of WLD tokens held by investors and team members from three years to five. This adjustment decreased the daily unlock rate by roughly 40%, dropping from 3.3 million to 2 million WLD tokens per day. The result? Within just 24 hours, the WLD token price jumped 45%, reaching $3.13 [17].

“Tokens remained locked to allow protocol maturation before unlocking.” – Tools for Humanity [17]

When market conditions took a downturn, Story Protocol opted for a different strategy. In February 2026, after the $IP token’s value plummeted 32% over 30 days, the project postponed its first major unlock by six months. This delay, enforced via an automated smart contract [19], allowed liquidity to enter the market more gradually, mitigating the effects of a weak market environment.

Monad, on the other hand, launched its public mainnet on November 24, 2025, with a carefully planned lock-up strategy. From the outset, 50.6% of its 100 billion MON tokens were locked. Investors and team members faced a one-year cliff, followed by monthly unlocks over the next four years. The project, which raised $225 million before launch, sold 7.5% of its total supply during a public sale on Coinbase at $0.025 per MON [16][18]. To ensure fair distribution, Monad prohibited locked tokens from being staked, ensuring staking rewards benefited the broader token ecosystem rather than being concentrated among insiders [18].

Another compelling example comes from Zorp. In December 2025, Zorp revised its lock-up terms for the $NOCK token. Seed round investors agreed to a one-year lock-up post-network launch, followed by an 18-month linear unlock. Team members faced a one-year cliff, with their tokens unlocking incrementally over 24 months. This structure, which involved 211 million $NOCK tokens for purchasers and 117 million for the team [15], helped reduce short-term supply pressures while aligning stakeholders with the project’s long-term goals.

Conclusion: What Investors Need to Remember

Lock-up periods are contractual arrangements designed to prevent large-scale share sell-offs immediately after an IPO - not federal requirements. In the Web3 space, these restrictions are often governed by smart contracts, which provide a transparent and secure way to enforce these agreements [3][2][4][20]. For investors, understanding how these mechanisms work is key to managing liquidity and planning exit strategies effectively.

As mentioned earlier, the end of a lock-up period often brings price swings and increased trading activity. To stay ahead, investors should carefully review SEC filings, particularly the “Shares Eligible for Future Sale” section in S-1 registration statements. These documents outline the exact expiration dates and the number of shares entering the market [4][1].

Tax planning and market timing are equally crucial. If you hold shares for over a year from the date you acquire them (not the IPO date), you may qualify for long-term capital gains tax rates, which are generally lower than ordinary income tax rates [4]. For insiders, setting up 10b5-1 trading plans during the lock-up period can help establish pre-arranged selling schedules, reducing risks of insider trading allegations [3][4]. These steps highlight the importance of blending regulatory, tax, and market strategies in your investment approach.

Navigating these complexities requires a deep understanding of regulatory frameworks, tax implications, and market dynamics. Bestla VC, with its focus on Web3 investments and secondary market solutions, provides expert guidance on OTC trades, early-stage investments, and legal matters. Collaborating with professionals can help you optimize release schedules, verify smart contract terms, and manage risks to enhance your returns.

FAQs

Where do I find a company’s lock-up expiration date?

You can find a company’s lock-up expiration date in its registration documents or prospectus. These documents detail the terms of the lock-up agreement, including how long it will last - usually between 90 and 180 days after the IPO. Reviewing these sources will help you determine when the restrictions on selling shares will end.

Can lock-up periods be extended or end early?

Lock-up periods can sometimes be adjusted, either extended or shortened, depending on the terms outlined in the underwriting agreement or lock-up contract. That said, these periods are generally set for a specific timeframe - most commonly between 90 and 180 days. Any modifications to the duration are subject to the conditions specified in the original agreement.

How should I plan buys or sells around an unlock?

When preparing for trades around a lock-up expiration, it’s essential to track the expiration date, which typically falls 90 to 180 days after an IPO. This period is crucial because stock prices often dip as insiders sell their shares, increasing the supply in the market.

Your approach will depend on your risk tolerance. If you’re comfortable with potential volatility, you might consider buying after a possible price drop. On the other hand, selling beforehand could help you avoid potential declines.

Don’t forget to factor in broader market trends and any recent news about the company, as these can also influence price movements. Always ensure your decisions align with your overall investment strategy.