Capital calls are a key process in private equity investments. When you commit to a fund, you don’t pay the full amount upfront. Instead, the General Partner (GP) requests portions of your commitment over time as needed. Here’s what you need to know:

- What is a Capital Call?

It’s a formal request by the GP for a portion of your pledged capital. These requests are legally binding and governed by the Limited Partnership Agreement (LPA). You’ll typically have 10–30 days to transfer funds after receiving notice. - How It Works:

- The GP identifies a need (e.g., investment, fees, or expenses).

- Fund administrators calculate each investor’s share and issue a notice.

- You wire your share, which is then used for the specified purpose.

- Why It Matters:

Capital calls prevent "cash drag", allowing you to keep uncalled capital invested elsewhere until needed. This helps optimize returns while maintaining liquidity. - Key Participants:

- General Partners (GPs): Manage investments and issue calls.

- Limited Partners (LPs): Ensure liquidity to meet obligations.

- Fund Administrators: Handle calculations and notices.

- Risks and Protections:

Missing a call can lead to penalties like interest charges or losing your partnership interest. Maintaining a liquidity buffer (1.5x–2x anticipated calls) reduces this risk. - Special Cases:

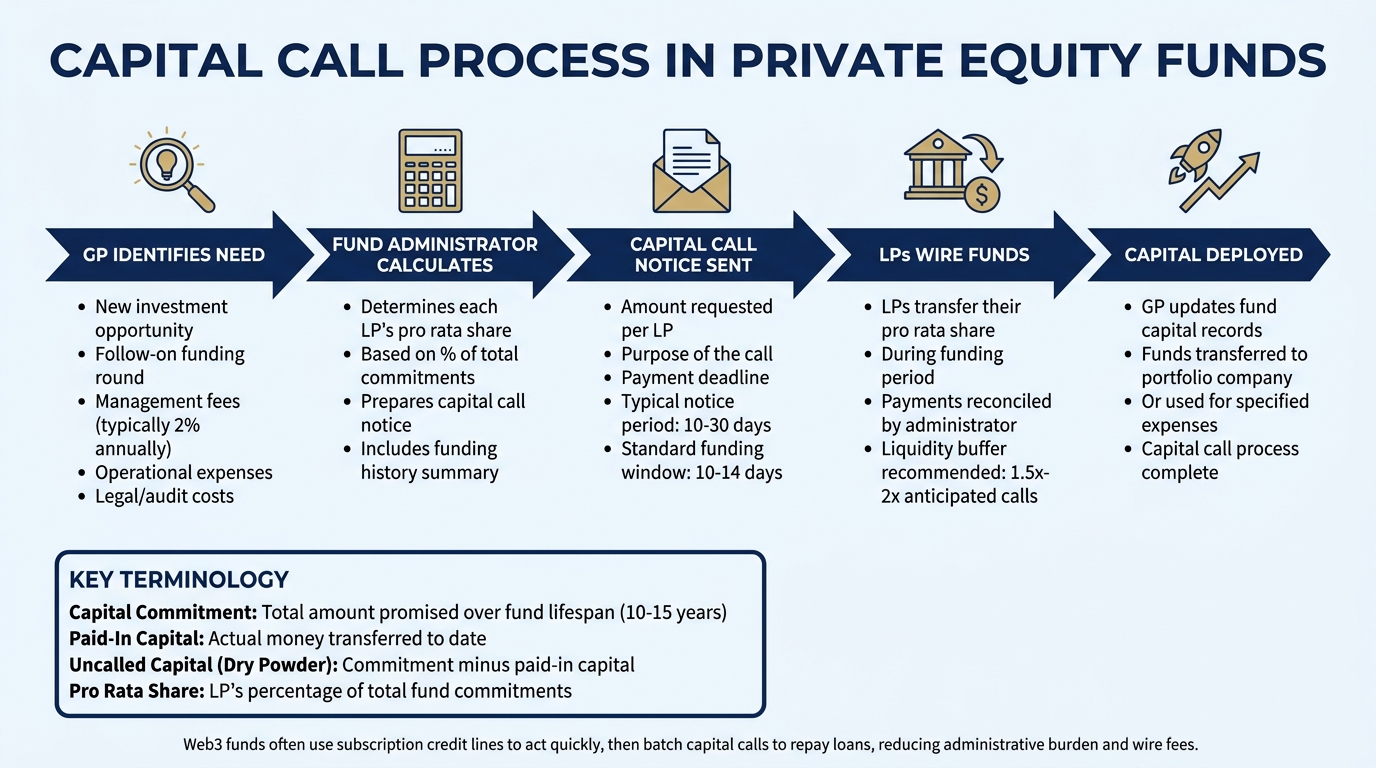

Web3-focused funds often use subscription credit lines to act quickly on investments, batching calls to repay loans.

Understanding capital calls ensures you can meet obligations, avoid penalties, and manage your investments effectively.

Private Equity Capital Calls: Mechanics, ILPA Standards, and Fiduciary Duty

sbb-itb-c5fef17

How Capital Calls Work

Capital Call Process: From GP Request to Fund Deployment

Capital Commitments vs Paid-In Capital

When you sign a Limited Partnership Agreement (LPA), you’re agreeing to a capital commitment – a promise to invest a specific amount of money over the fund’s lifespan, which typically spans 10 to 15 years. This commitment sets the upper limit of your financial responsibility, but it doesn’t mean you need to provide the full amount upfront.

Paid-in capital, on the other hand, is the actual money you transfer to the fund in response to capital calls. The difference between your total commitment and the amount you’ve paid in so far is referred to as uncalled capital or "dry powder." For example, if you’ve committed $10 million but have only contributed $6 million, your uncalled capital is $4 million.

Your contribution during each capital call is based on your pro rata share, which corresponds to your percentage of the total commitments made to the fund. Once your full commitment is paid, the General Partner (GP) typically cannot request more funds unless the LPA includes an overcall provision. Such provisions allow the GP to request additional funds – usually up to 110% or 120% of your original commitment – to cover unexpected expenses or fees [2].

Now that these terms are clear, let’s break down how the capital call process works.

Capital Call Structure and Process

The capital call process is fairly straightforward. It starts when the GP identifies a need for funds. This could be for a new investment, a follow-on round for an existing portfolio company, or to cover operational costs like management fees, audits, or legal expenses.

Once the need is determined, the fund administrator calculates each Limited Partner’s (LP) pro rata share and sends out a formal capital call notice. This notice includes the amount requested, the purpose of the call, the payment deadline, and a summary of your funding history. Typically, LPs are given 10 to 14 days to fulfill the call [3].

During the funding period, LPs wire their contributions. After reconciling the payments, the GP updates the fund’s capital records and deploys the funds. The capital is either sent to a portfolio company for investment or used to cover specified expenses.

This process serves as the foundation for both traditional Venture Capital funds and newer Web3-focused funds, though there are some notable differences in how each operates.

Capital Call Examples in Venture Capital and Web3

The way capital calls are handled can vary significantly between traditional venture capital funds and Web3-focused funds.

In venture capital, funds generally issue multiple capital calls during the early years of the fund’s lifecycle. Each call typically represents a smaller portion of an LP’s total commitment – often between 5% and 25% – as the fund gradually deploys capital across various investment rounds.

Web3 and crypto-focused funds, however, often operate at a faster pace. These funds may issue larger, less frequent capital calls to quickly seize time-sensitive opportunities. To accommodate this speed, many Web3 GPs rely on subscription lines of credit – short-term loans backed by LP commitments. This allows them to deploy capital immediately while batching LP calls at later intervals to repay the credit line. For instance, a fund might use a credit line to make several investments and then issue a single capital call to cover the loan. This approach not only reduces administrative work and wire fees but also gives LPs more predictable cash flow management.

Additionally, management fees in Web3 funds are often collected quarterly or semi-annually, sometimes combined with investment-related calls to minimize the number of wire transfers [4].

Recognizing these differences can help you navigate capital calls more effectively and align them with your broader investment strategy.

Legal and Financial Framework for Capital Calls

Limited Partnership Agreement Terms

The Limited Partnership Agreement (LPA) serves as the backbone for managing capital calls. It outlines key requirements, like providing investors with notice – usually between 10 and 30 business days – before the funding deadline.

The LPA also sets boundaries on how called capital can be used. Common purposes include funding new investments, supporting follow-on rounds, covering management fees (typically around 2% of committed capital annually), handling fund expenses, and addressing organizational costs. It distinguishes between the commitment period – usually the first three to five years – and the time after. Once the commitment period ends, capital calls are generally limited to follow-ons, fees, and existing obligations.

Additional clauses, such as overcall protections, cap the amount general partners (GPs) can request, generally at 110% to 120% of an investor’s original commitment. Many LPAs also include opt-out rights, giving investors the ability to decline specific investments due to regulatory issues (like ERISA or the Volcker Rule), tax concerns, or ESG policy restrictions.

Understanding these provisions is essential, as they influence the penalties and remedies discussed in the next section.

Default Risks and Available Remedies

Failing to meet a capital call is a major breach of LPA terms. Such defaults can disrupt fund operations, leading to broken deal fees, delayed investments, or reliance on costly credit lines.

LPAs prescribe escalating penalties for defaulting investors. Initially, penalty interest is applied – commonly the prime rate plus 5% to 10%, or a flat 10% to 15% annually. Persistent defaults may result in the forced sale of the investor’s interest at a significant discount – often 50% to 75% of its net asset value – or, in extreme cases, complete forfeiture of the partnership interest. These measures are designed to safeguard the fund’s stability and ensure the capital call process remains reliable.

"The default remedies in a fund’s limited partnership agreement (‘LPA’) significantly impact the health and stability of the subscription credit facility because they incentivize investors to fund their capital contributions."

To avoid default risks, investors are advised to maintain a liquidity buffer of 1.5x to 2x their anticipated near-term capital calls. Most LPAs also include a cure period – typically 10 to 30 days – to allow investors to address missed payments before severe penalties are enforced.

Capital Call Lines of Credit

In addition to the LPA’s formal rules, funds often rely on capital call lines of credit (also called subscription facilities or sub-lines). These short-term credit tools are backed by investors’ uncalled capital commitments, providing funds with immediate access to cash when needed.

Lenders secure these loans by pledging the GP’s right to call capital and gaining control over the accounts where investor contributions are deposited. When a fund needs to act quickly – like closing a deal – it can draw on this credit line. The fund then issues a capital call to repay the loan, typically within 30 to 90 days.

This approach not only speeds up deal closings but also boosts the fund’s internal rate of return by minimizing cash drag. These credit lines usually carry interest rates of SOFR plus 100 to 300 basis points, along with commitment fees on undrawn amounts (generally 15 to 50 basis points). However, the LPA must explicitly permit borrowing, pledging unfunded commitments, and delegating the authority to issue capital call notices. Regardless of circumstances, investors remain obligated to fulfill capital calls used to repay these loans, even if the fund encounters a default.

"A capital call (or ‘subscription line’) facility is a short-term loan bridging the time between a venture capital or private equity fund making a capital call and receiving capital contributions from its investors to finance a new investment."

Managing Capital Calls: A Guide for Institutional Investors

Tracking Uncalled Capital

Institutional investors must use a centralized system to monitor unfunded commitments across their portfolios. Tools like real-time dashboards can reconcile fund records and send automated alerts, minimizing the risk of administrative delays that could lead to default penalties [11].

A common practice is maintaining a liquidity coverage ratio of 1.5x to 2x for upcoming capital calls [2]. This buffer accounts for the typical notice periods of 10 to 30 business days [2] and safeguards against overlapping calls from multiple funds. To optimize returns while keeping funds accessible, investors should allocate uncalled capital into short-term, low-risk instruments like Treasury bills or money market funds [2][1].

Conducting regular liquidity stress tests and scenario analyses helps evaluate the ability to meet simultaneous capital calls, especially during market disruptions [11][2]. This is particularly relevant when addressing the denominator effect – a situation where declining public market values cause private equity allocations to exceed limits, potentially impacting new commitments [2].

These monitoring efforts play a crucial role in shaping strategic cash flow planning, as discussed in the next section.

Aligning Capital Calls with Portfolio Objectives

Effective capital call management begins with cash flow modeling to predict the timing and size of calls and distributions. This approach helps align liquidity needs with portfolio goals, minimizing unexpected demands [12][6]. Diversified portfolios, as highlighted in a Pantheon study covering 1993–2013, can deploy up to 75% of unfunded commitments in public markets without increasing default risk [12].

"Holding excessive cash to meet capital calls can significantly reduce overall portfolio performance. It is critical to balance liquidity and return to create the best long-term outcomes." – John Jennings, President and Chief Strategist, ArchBridge Family Office [12]

Building a program across varied vintage years, geographies, and fund types helps smooth cash flows, as fluctuations in individual fund calls tend to offset one another [12]. Over time, mature private investment programs often become self-funding, with distributions from older funds covering capital calls for newer ones [12]. To avoid cash drag, investors should maintain only one to two quarters’ worth of expected capital calls in cash, placing the rest in a diversified liquid portfolio. Using margin loans can also help meet short-term deadlines without resorting to forced asset sales [12].

Capital Call Management in Web3 VC Funds

Managing capital calls in Web3 venture capital funds requires additional flexibility due to their unique dynamics. These funds often issue smaller but more frequent capital calls – typically 2% to 5% of total commitments – making higher liquidity buffers essential given the unpredictability of startup funding cycles [2]. The fast-paced nature of blockchain and crypto sectors also demands strategies distinct from traditional private equity.

In this environment, subscription facilities are key. They bridge timing gaps, allowing immediate deal execution while enabling LPs to handle capital calls in more predictable quarterly batches [4][7]. These facilities can also boost IRR by 50 to 200 basis points [2].

Proactive communication with General Partners is essential for anticipating the timing and size of upcoming calls [11][2]. Web3 fund structures often involve multiple closes and equalization payments. To manage this complexity, investors should use platforms that automate pro rata calculations, ensuring accuracy and transparency [8][4]. This kind of automation is particularly important in sectors with compressed deal cycles, where traditional approaches may fall short of the agility required.

Conclusion

Grasping how capital calls work is crucial for institutional investors involved in private equity and venture capital funds. Effectively managing liquidity – by maintaining a buffer of 1.5× to 2× the anticipated near-term calls – helps investors meet their obligations without risking hefty default penalties [2].

Efficient capital call management also boosts operational performance. By aligning calls with deal closings instead of keeping excess cash idle, funds minimize cash drag and improve key metrics like Internal Rate of Return (IRR) and Total Value to Paid-In Capital (TVPI) [1][3]. This becomes especially important in Web3 and early-stage venture strategies, where smaller, more frequent calls (typically 2–5% of total commitments) require robust tracking systems and larger liquidity reserves [2][3]. These operational practices align closely with the legal frameworks that govern these processes.

Speaking of legal frameworks, they play a key role in safeguarding investor interests. The Limited Partnership Agreement (LPA) establishes binding rules for investors, including standard notice periods of 10–30 business days, which offer limited flexibility [2][5]. Investors who understand these contractual provisions are better equipped to protect their interests while maintaining strong ties with General Partners.

As the funding environment continues to shift, so do the strategies and tools supporting capital calls. Subscription facilities are now common for funds exceeding $20 million, reflecting this evolution [4]. Automating call processes, enforcing consistent call schedules, and adopting multi-layered liquidity strategies allow investors to capitalize on opportunities without resorting to forced sales. Mastering these elements distinguishes the most efficient institutional investors from the rest.

FAQs

What happens if I can’t meet a capital call on time?

Failing to meet a capital call on time can result in various penalties. These might include interest charges or even the loss of your partnership interest, depending on the terms laid out in the fund agreement. It’s essential to carefully review your fund’s agreement to understand the potential consequences. If you think you might face delays, consider reaching out to the fund manager proactively to discuss your situation. Open communication can sometimes help mitigate the impact.

How do I estimate upcoming capital calls and needed liquidity?

To get a handle on upcoming capital calls and the liquidity you’ll need, start by examining the fund’s investment pipeline and the terms outlined in the limited partnership agreement (LPA). Take a close look at the fund’s investment schedule and past patterns of capital calls. These calls often occur over a span of 3-5 years, with each one typically accounting for 10-25% of your total commitment. It’s wise to keep a cash reserve that matches these projections, as call notices are generally sent out 10-30 days before the payment is due.

Do subscription credit lines change my capital call obligations?

Subscription credit lines can influence your capital call obligations by offering fund managers access to uncalled capital commitments. This can postpone the need for an immediate capital call, giving investors more flexibility in managing their cash flow. However, it’s important to note that this delay doesn’t remove your responsibility. When the actual capital call is made, you’re still obligated to meet your commitment in full.