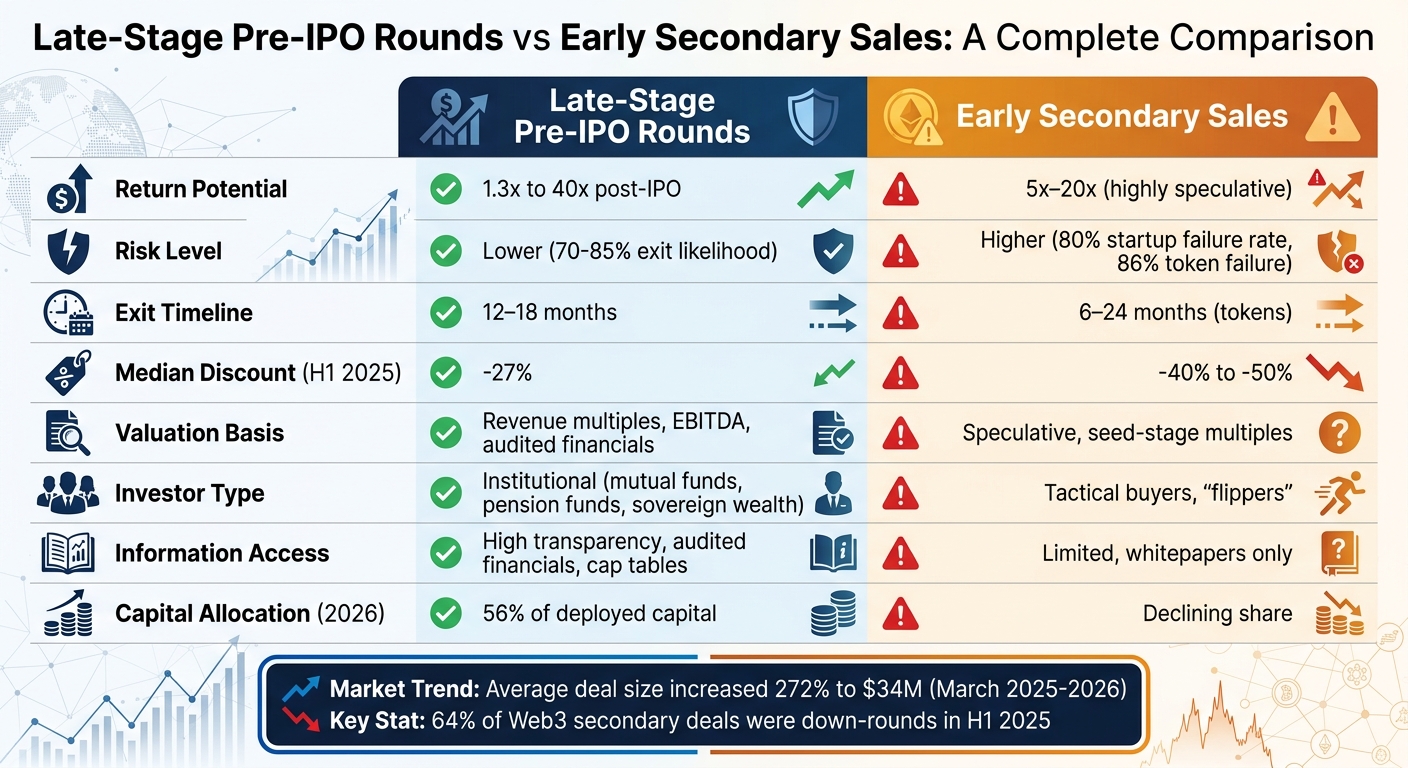

Late-stage pre-IPO investments often deliver better returns with lower risk compared to early secondary sales. These rounds focus on mature companies nearing IPOs, offering shorter exit timelines (12–18 months) and more reliable financial data, like revenue multiples and EBITDA. In contrast, early secondary sales, dominated by seed-stage deals, are highly speculative, with 80% of blockchain startups failing in their first year. Late-stage rounds attract institutional investors due to their transparency, audited financials, and proximity to liquidity events.

Key Takeaways:

- Higher Returns: Late-stage investments can yield up to 40x returns post-IPO, while early sales are riskier with up to 86% token failure rates.

- Lower Risk: Late-stage rounds have a 70–85% exit likelihood versus 20% for early-stage ventures.

- Institutional Preference: Late-stage deals draw mutual funds and pension funds due to their structured governance and data-driven valuations.

- Market Trends: By 2026, 56% of venture capital in Web3 flows into late-stage deals, reflecting a preference for stable, revenue-generating companies.

Quick Comparison:

| Factor | Late-Stage Pre-IPO Rounds | Early Secondary Sales |

|---|---|---|

| Return Potential | 1.3x to 40x post-IPO | 5x–20x but highly speculative |

| Risk Level | Lower | Higher (80% startup failure) |

| Exit Timeline | 12–18 months | 6–24 months (tokens) |

| Valuation Basis | Revenue multiples, EBITDA | Speculative, seed-stage multiples |

| Investor Type | Institutional (mutual funds, etc.) | Tactical buyers, "flippers" |

Late-stage pre-IPO rounds are ideal for those seeking stable, predictable growth, while early secondary sales are better suited for risk-tolerant investors chasing higher potential returns.

Late-Stage Pre-IPO vs Early Secondary Sales Comparison

Pre-IPO Investing: Risks, Rewards, and Strategy

sbb-itb-c5fef17

Financial Returns and Historical Performance

Investing in late-stage pre-IPO rounds offers higher returns with reduced risk compared to early secondary sales in the Web3 space. The median discount to the last primary round for venture secondaries improved to -27% in the first half of 2025, up from -39% during the same period in 2024 [8]. This narrowing reflects growing confidence in companies nearing public offerings. A closer look at recent IPOs highlights this trend.

Take Circle‘s NASDAQ IPO in June 2025, for example. Before going public, secondary market shares traded at a valuation between $5.0 billion and $5.25 billion. When the IPO launched, it was priced at $6.8 billion ($31 per share). However, day-one trading opened at $69 per share, eventually surging past $200 per share [6]. Investors who bought late-stage secondary shares reaped enormous returns, while those who exited earlier missed out on these gains.

| Metric | Early Secondary (Seed/SAFT) | Late-Stage Pre-IPO (Equity) |

|---|---|---|

| Median Discount (H1 2025) | -40% to -50% | -27% |

| Time-to-Exit | 6–24 Months | 12–18 Months |

| Exit Likelihood | 20% survival rate | 70%–85% |

| Return Multiple Potential | 5x–20x (but 86% of tokens fail) | 1.3x (at IPO) to 40x (post-IPO peak) |

The data makes it clear: late-stage pre-IPO rounds tend to yield better outcomes. For instance, Kraken’s confidential IPO filing in June 2025 led to a significant valuation jump. Its secondary market valuation rose from $6.82 billion to over $7.7 billion, with $750 million in trade volume recorded over just 90 days [6]. AI-focused Web3 companies also posted a 17% median valuation increase in the first half of 2025, while companies founded in 2020 or later saw a median growth of 70% [8]. These numbers highlight how late-stage investments benefit from companies entering public markets with validated business models and audited financials.

Early-stage investments, on the other hand, tell a very different story. In the first half of 2025, 64% of Web3 secondary market deals were priced as down-rounds relative to prior valuations [6]. Seed and pre-seed rounds dominated, making up 82% of crypto private market offers. Yet, 80% of new blockchain startups fail within their first year [6][11]. The shift in capital allocation is clear – 56% of all deployed capital now goes to later-stage deals, as investors pivot away from speculative tokens toward revenue-generating infrastructure companies [11].

Risk-Reward Profiles

Early secondary sales and late-stage pre-IPO rounds present very different risk-reward dynamics. Early secondary sales are characterized by extreme volatility, often influenced by what’s known as "token-supply overhang." This refers to an excess of tokens in circulation, which can lead to price drops. Buyers in these rounds typically demand steep discounts – ranging from 40–50% – compared to spot market prices [6]. On the other hand, late-stage pre-IPO rounds experience more moderate volatility, as their valuations are tied to public market comparisons, such as those for companies like Coinbase or Circle [6]. This connection to established benchmarks provides more stability, unlike the speculative swings seen in early rounds. These differences in volatility significantly influence performance outcomes in subsequent investment stages.

The risks in early-stage blockchain ventures are stark: 80% of new blockchain startups fail within their first year [11]. In 2025 alone, 11.6 million tokens became defunct, accounting for 86.3% of all token failures over the prior five years [11]. In contrast, late-stage companies nearing an IPO – typically within a 12–18 month window – offer much higher probabilities of successful exits [6]. Consider Uber’s private funding journey: while seed investors saw theoretical returns of 2,050,000%, late-stage Series D investors achieved a more modest but still impressive 382% return by the time of its IPO [12].

Dilution is another key factor that varies between these two investment stages. Late-stage pre-IPO rounds often involve issuing new shares, which dilutes existing investors’ ownership stakes. In contrast, early secondary sales involve trading existing shares, so ownership percentages remain unchanged [13][12]. However, early secondary buyers face challenges like limited transparency and pricing inefficiencies [4][10]. Late-stage investors, in comparison, benefit from detailed financial audits and greater scrutiny of management teams, making these investments more informed [4][10].

Here’s a breakdown of the contrasting risk metrics:

| Risk Metric | Early Secondary Sales (Seed/SAFT) | Late-Stage Pre-IPO Rounds |

|---|---|---|

| Volatility Level | High (supply overhang & tactical flips) | Moderate (anchored to public comps) |

| Exit Probability | Low (80% first-year failure rate) [11] | High (12–18 months to IPO) [6] |

| Dilution Impact | None (existing shares traded) | High (new shares issued) [13][12] |

| Pricing Basis | Narrative & seed-stage multiples | Public market EV/Revenue multiples [6] |

| Typical Discount | 40–50% median [6] | Tighter spreads; closer to par [6] |

The Web3 venture market has increasingly shifted its focus toward late-stage mega-rounds, favoring investments with more predictable outcomes. Between March 2025 and March 2026, the average check size for crypto venture capital rounds surged by 272%, reaching $34 million [11]. This trend reflects a "flight to quality", as early-stage ventures continue to face high attrition rates [11]. As SecondLane and Delphi Digital aptly describe:

"Companies and startups now face a verdict of being ‘guilty until proven innocent.’ Those who can show real traction… are rewarded, at the expense of out-of-favor sectors" [6].

Institutional Participation and Capital Efficiency

Late-stage pre-IPO rounds have become the go-to entry point for institutional investors like mutual funds, sovereign wealth funds, and pension managers – groups that traditionally waited for companies to go public. Why? Because companies are staying private much longer. Back in 2000, the typical company went public at 5–6 years old. By 2025, that number will exceed 12 years [12]. With so much value now being created in private markets, these investors are stepping in earlier to capture growth.

The numbers tell the story: between March 2025 and March 2026, the average crypto venture deal size jumped to $34 million [9]. Late-stage deals soaked up 56% of the total funding, reflecting a "barbell economy" where capital pours into massive late-stage deals while mid-stage rounds dwindle [11]. In Q1 2026 alone, more than $5 billion flowed into crypto startups, prioritizing companies with proven revenue streams [9].

Institutional investors are drawn to late-stage rounds for a key reason: they offer a level of transparency and governance that early secondary sales simply can’t match. Late-stage buyers gain access to audited financials, detailed cap tables, and direct communication with company leadership. Crossover funds like Fidelity and T. Rowe Price also bring public market valuation expertise to these private investments [10][12]. In contrast, early secondary token buyers rely on public whitepapers and sparse disclosures, which creates a significant gap in available information [10]. This transparency not only strengthens governance but also enables more efficient use of capital.

Speaking of efficiency, late-stage investments stand out here as well. These investors avoid the hefty 2% management fees and 20% carried interest that come with traditional venture funds. They also skip the decade-long lock-up periods. Instead, they aim for shorter 12–18 month windows before liquidity events, capturing value at critical moments of growth [6][15].

Here’s how early secondary sales stack up against late-stage pre-IPO rounds across key metrics:

| Feature | Early Secondary Sales | Late-Stage Pre-IPO Rounds |

|---|---|---|

| Institutional Involvement | Mostly tactical buyers and "flippers" chasing steep discounts [6] | Led by crossover funds, sovereign wealth funds, and pension funds [12] |

| Capital Efficiency | Discounts range from 15–50% due to high risk and illiquidity [6][14] | Pricing based on public market comparisons with tighter bid-ask spreads [6] |

| Liquidity/Exit | Exit typically takes 6–24 months, often relying on token unlocks [6] | Clear path to IPO within 12–18 months; structured for liquidity [6][12] |

| Information Access | Limited, often based on whitepapers and tokenomics [10] | Full transparency with audited financials, cap tables, and board access [10][12] |

| Deal Maturity | Pre-Seed deals average 6.1 months; Seed/Round A take 3+ months [14] | Rounds B, C, and D close in just over a month due to institutional readiness [6][14] |

This shift toward institutionalization is picking up speed. Private markets now raise about four times more capital annually than public equity markets, with global private market assets under management reaching $26 trillion [12]. Institutional investors typically allocate 25–35% of their portfolios to alternative investments as a standard practice [12]. Alexandre Covello of Venture Secondaries captures this trend perfectly:

"Instead of committing to 10-year venture funds, large family offices now buy direct positions in late-stage companies… targeting markups at the next financing round 12–18 months later" [15].

Pros and Cons

When comparing late-stage pre-IPO rounds with early secondary sales, the differences boil down to key factors like return potential, risk, and exit timelines. Here’s a side-by-side look at how these two strategies stack up:

| Factor | Late-Stage Pre-IPO Rounds | Early Secondary Sales |

|---|---|---|

| Return Potential | Moderate and more predictable, as much of the growth has already occurred [2]. | Extremely high potential (up to 2,000% or more), though highly speculative [12]. |

| Risk Level | Lower, thanks to mature business execution [2]. | Much higher, with nearly 80% of blockchain startups failing in their first year [11]. |

| Time to Exit | Shorter, typically 12–18 months to IPO [6]. | Longer, ranging from 7–10 years for equity or 6–24 months for token unlocks [6]. |

| Valuation Basis | Grounded in data, using revenue multiples, EBITDA, and public market comparisons [2]. | Speculative, driven by team vision and potential market impact [2]. |

| Information Access | High transparency with access to detailed data [10]. | Limited, often relying on public information or whitepapers [10]. |

| Operational Maturity | Backed by an established business model and a defined customer base [1]. | Frequently in early stages, still testing product-market fit [1]. |

Bill Clark, CEO of MicroVentures, offers this perspective:

"While the investment risk is still high in all startups, late-stage opportunities may seem to have a clearer path to an IPO, acquisition, or other exit" [7].

For those seeking more predictable growth tied to measurable metrics, late-stage pre-IPO rounds could be the better fit. On the other hand, if you’re comfortable with higher risks and drawn to the potential for massive returns, early secondary sales might align better with your Web3 investment strategy. Keep in mind, though, that 60% of companies at the pre-Series A stage never progress to Series A [16]. This comparison highlights the trade-offs, helping investors tailor their approach to their risk tolerance and market outlook.

Conclusion

The analysis above highlights some key takeaways for investors. Late-stage pre-IPO rounds stand out for their combination of predictable returns and reduced risk. These opportunities often come with shorter exit timelines (12–18 months compared to 6–24 months for early-stage token unlocks), established revenue streams, and professional-grade infrastructure that early secondary sales typically lack [6]. A case in point: during Circle’s NASDAQ IPO in June 2025, secondary shares initially valued at $5.0–$5.25 billion experienced a notable uptick post-IPO, delivering strong returns for investors who timed their late-stage entry well [6].

The current market environment also leans heavily in favor of late-stage investments. In Q1 2026, deal sizes increased sharply by 272%, reaching an average of $34 million, with mega-rounds accounting for a dominant 86% of venture funding [9][17]. Jan Strandberg, Co-Founder & CEO of Acquire.Fi, aptly summarizes the trend:

"The secondary print is often more honest than the primary mark, even when it’s uncomfortable" [5].

With more than 70% of venture exits now occurring through secondary markets rather than traditional IPOs or M&A, the appeal of late-stage pre-IPO rounds continues to grow [3].

For investors, the smart move is to focus on Tier A companies that feature audited financials and clean cap tables [3]. Keeping an eye on confidential IPO filings from companies like Kraken and Gemini could help identify potential catalysts. Additionally, prioritizing investments in revenue-generating protocols – particularly in areas like infrastructure, stablecoin payments, and custody – while benchmarking valuations against public comparables such as Coinbase’s EV/Rev multiples, can help gauge whether secondary shares are priced attractively [6]. This disciplined, data-driven approach builds on earlier insights about institutional participation and rewards careful capital allocation.

The Web3 investment space has evolved significantly, moving beyond flashy presentations and speculative token stories. In 2026, success will hinge on targeting businesses with tangible revenue, institutional support, and a clear trajectory toward public markets – qualities that late-stage pre-IPO rounds are uniquely positioned to deliver.

FAQs

How can I tell if a Web3 company is truly “IPO-ready”?

To figure out if a Web3 company is ready to go public, you’ll need to take a close look at its financial stability, how well its operations are running, and whether it’s hitting major milestones like achieving product-market fit and steady revenue growth. Companies that show clear market traction, have institutional investors on board, and follow disciplined growth strategies are generally in a stronger position to enter public markets. It’s also important to factor in IPO trends specific to the Web3 sector and the liquidity of secondary markets when evaluating the company’s readiness for this big step.

What documents should I review before buying late-stage pre-IPO shares?

Before purchasing late-stage pre-IPO shares, it’s essential to carefully examine key documents. These include details on preferred share terms, liquidation preferences, rights of first refusal (ROFRs), and any relevant investment agreements or offering materials. These documents outline crucial information about your rights as an investor and the potential risks involved.

What can delay or block the expected 12–18 month exit?

Delays or roadblocks to the planned 12–18 month exit can stem from several factors, including a narrow IPO window, market skepticism, shifts in sector valuations, or challenges tied to regulations and liquidity. These hurdles might push companies to lean more heavily on secondary markets or alternative liquidity options, which could, in turn, affect the expected timeline.